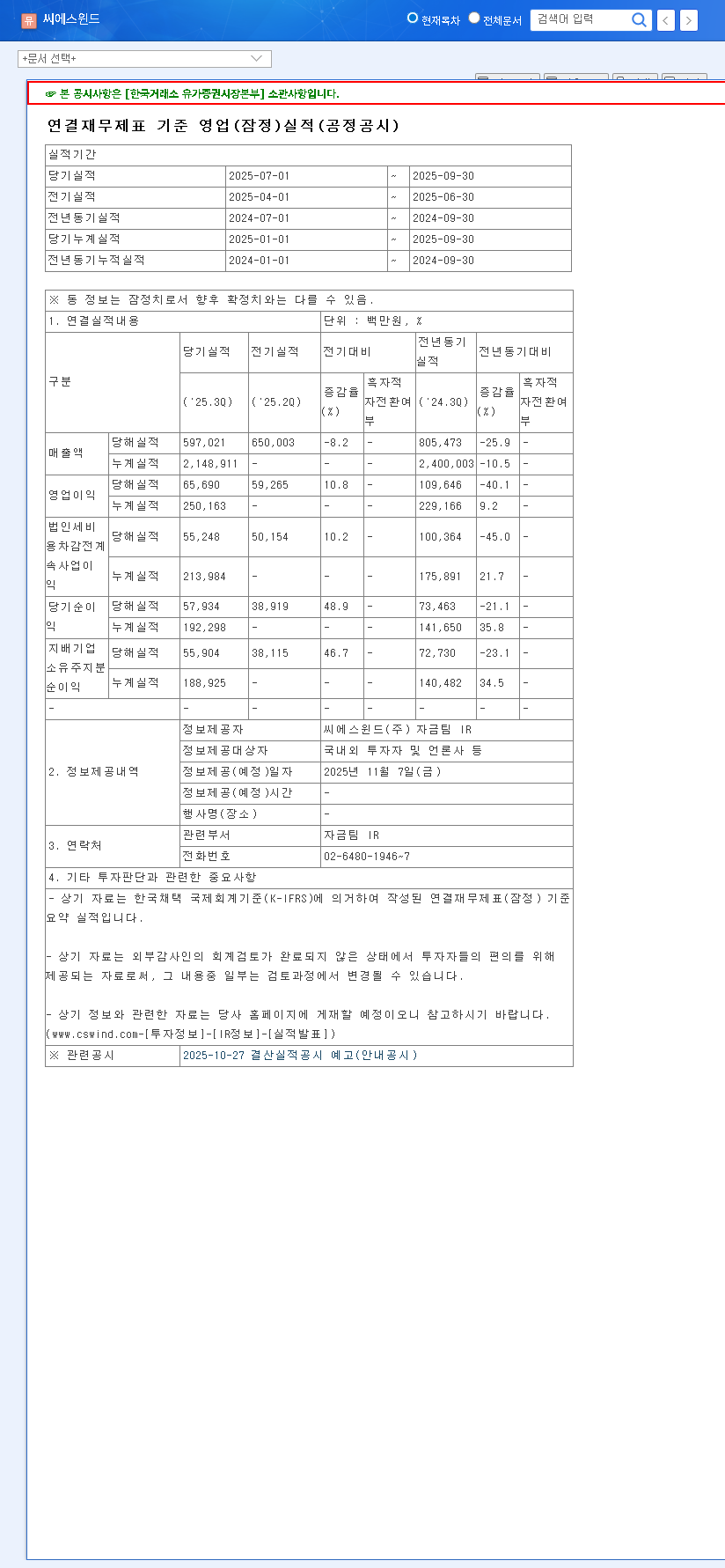

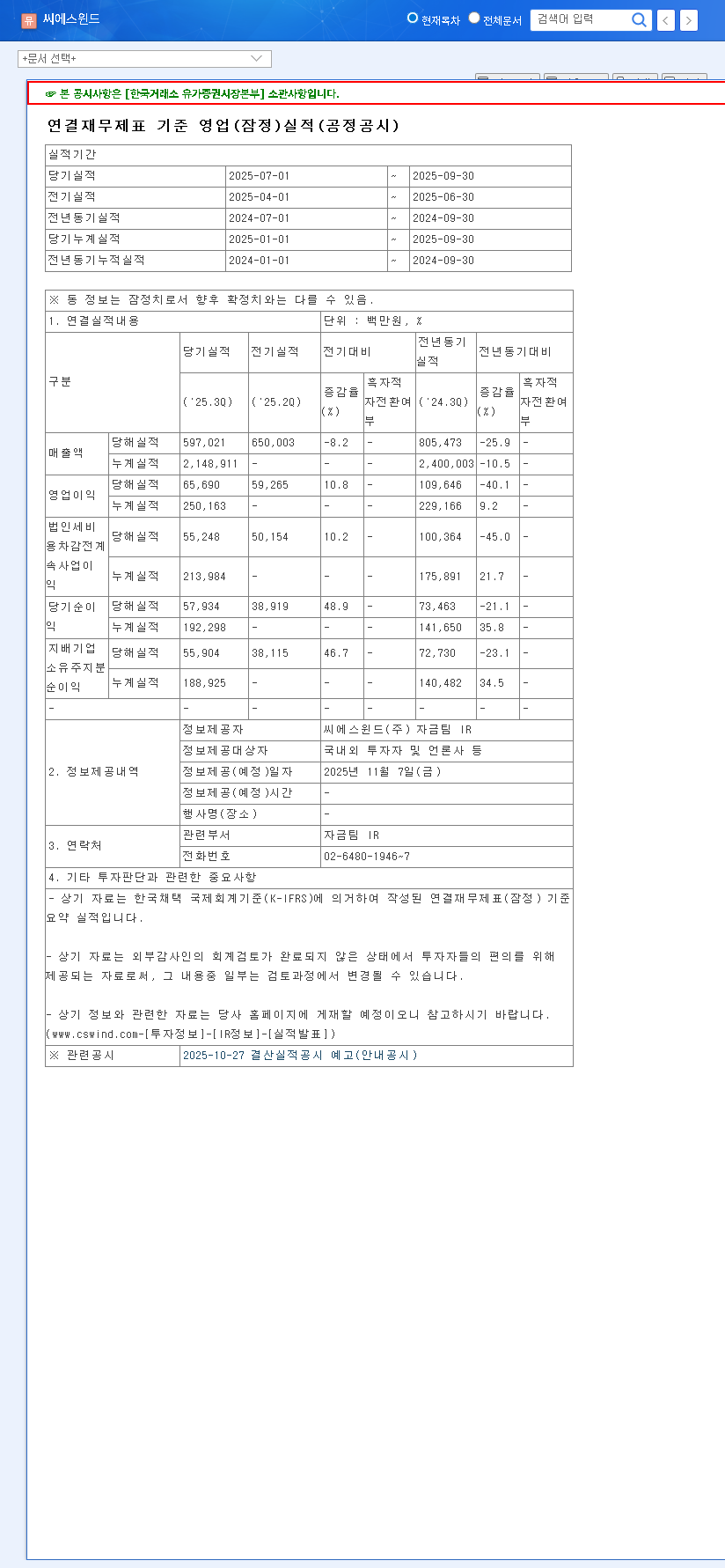

In a significant development for the global renewable energy sector, industry leader CS Wind Corporation has announced a major wind tower supply contract with Siemens Gamesa Renewable Energy. This 67.2 billion KRW deal is more than a simple transaction; it’s a strategic move that reinforces CS Wind’s market position and offers a clear signal to investors about its mid-to-long-term growth trajectory. For anyone following CS Wind stock or the broader green energy market, understanding the nuances of this agreement is crucial.

This article provides an in-depth investment analysis of the contract, exploring its financial impact, strategic importance, and the macroeconomic factors that investors must consider. We will break down what this means for the company’s fundamentals and its future in the competitive renewable energy landscape.

Contract Details: A Closer Look at the Landmark Agreement

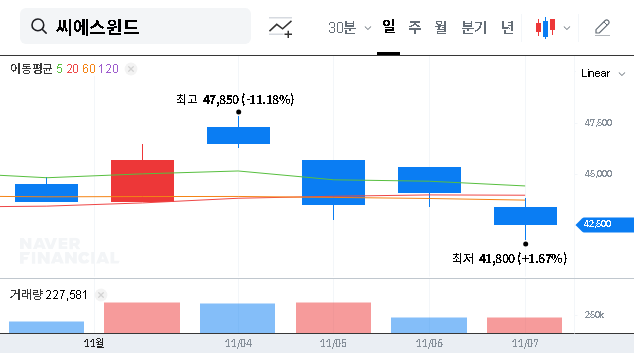

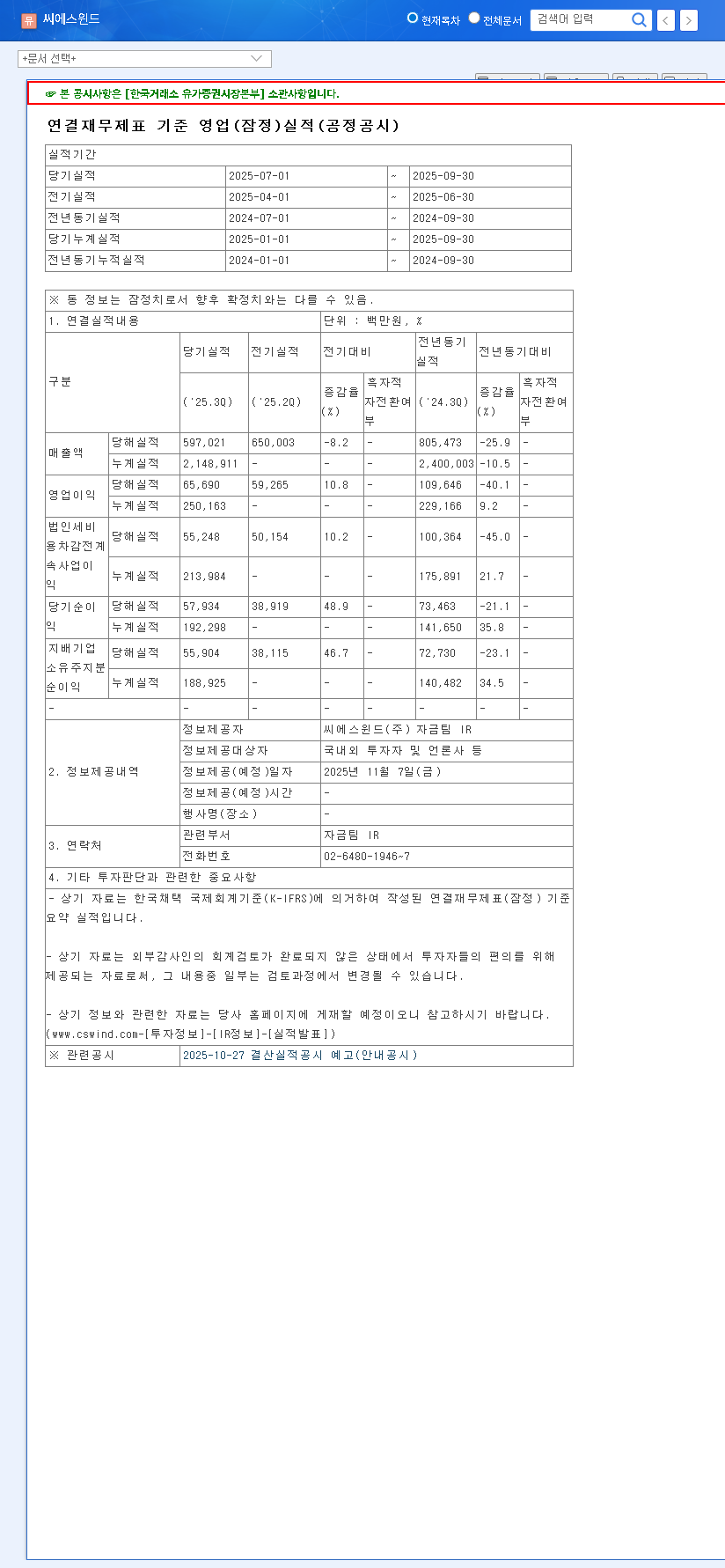

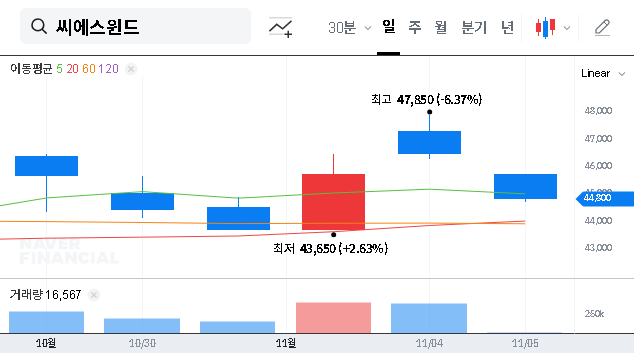

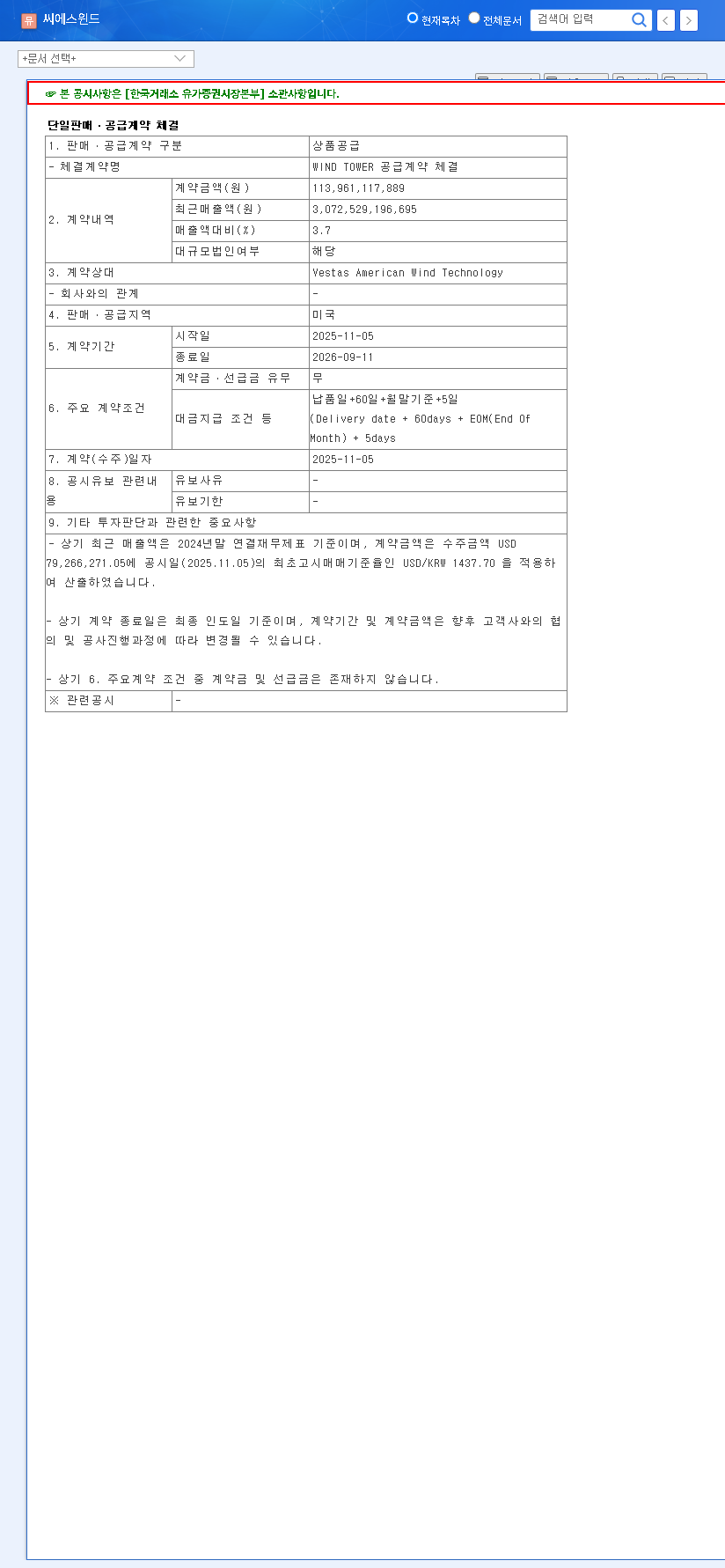

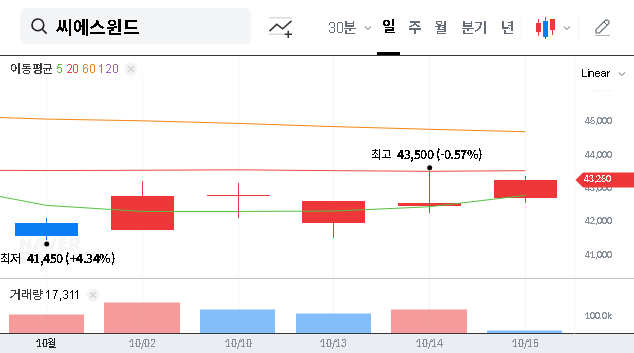

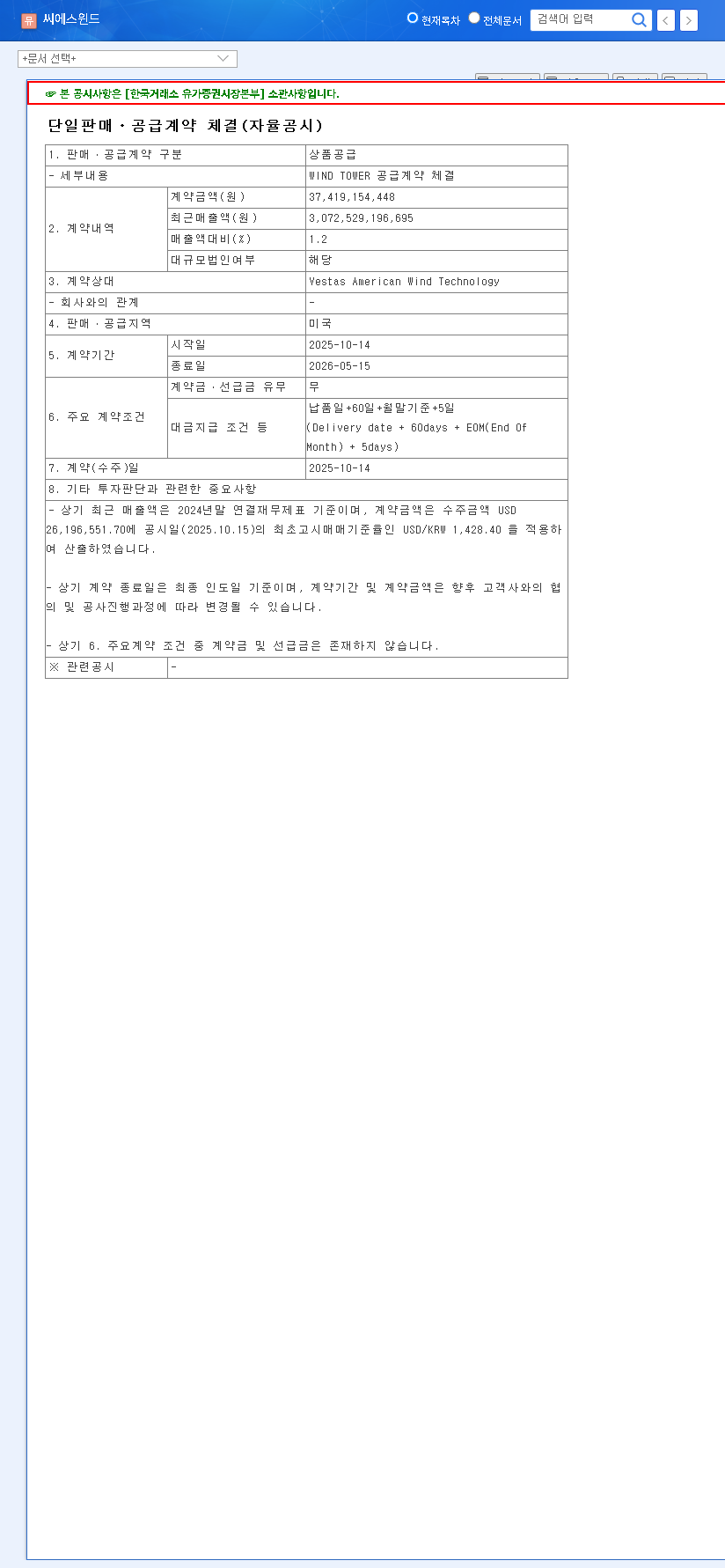

On November 14, 2024, CS Wind publicly disclosed the contract, formalizing its partnership with Siemens Gamesa, a global titan in wind turbine manufacturing. The deal centers on the supply of its core wind tower products to Poland, a key European market. For complete details, you can view the Official Disclosure on DART.

Key Financial and Logistical Terms:

- •Contract Value: 67.2 billion KRW (approximately €40.7 million), representing a significant 2.2% of CS Wind’s estimated 2024 revenue.

- •Counterparty: Siemens Gamesa Renewable Energy, one of the world’s largest and most respected wind turbine manufacturers.

- •Product: High-quality WIND TOWER structures, a core competency of CS Wind.

- •Supply Region: Poland, enhancing CS Wind’s footprint in the rapidly expanding Eastern European renewable energy market.

- •Contract Period: A 16-month term from November 13, 2025, to March 26, 2027, ensuring a stable revenue stream for future fiscal years.

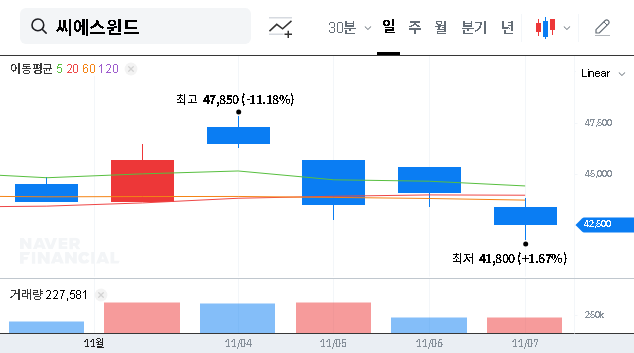

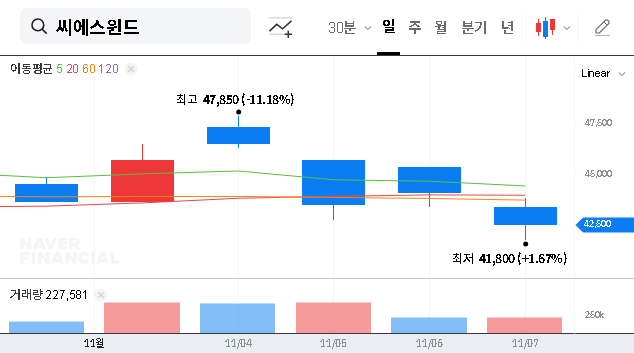

Strategic Impact: Why This Deal Matters for CS Wind Stock

This agreement is far more than just a number on a balance sheet. It strategically positions CS Wind for sustained success and validates its long-term growth narrative.

1. Securing Future Revenue & De-Risking Growth

For investors, predictability is paramount. By securing a long-term contract that begins in late 2025, CS Wind enhances its revenue visibility for the coming years. This locked-in income stream provides a stable foundation, de-risking future growth plans and demonstrating a consistent ability to fill its order book.

This deal reaffirms the strength of CS Wind’s core wind tower business, providing a solid financial base that supports its ambitious expansion into new verticals like the offshore wind substructure business.

2. Validating the Broader Business Strategy

CS Wind has been actively diversifying its portfolio, notably through its acquisition of Bladt Industries to enter the offshore wind substructure business. This contract proves that while expanding, the company has not lost focus on its foundational wind tower segment. The synergy is clear: a thriving core business generates the capital and credibility needed to successfully scale new ventures, creating a more resilient and diversified global enterprise.

Investor Watchlist: Macroeconomic Risks & Considerations

While the outlook is positive, prudent investors should remain aware of external variables that could impact profitability and market sentiment.

- •Currency Exchange Volatility (KRW/EUR): As a contract priced in a foreign currency, fluctuations in the KRW/EUR exchange rate can directly affect the final revenue and profit margins. Investors should monitor the company’s hedging strategies to mitigate this risk.

- •Global Interest Rate Environment: The cost of capital is critical for large-scale energy projects. High interest rates could slow the financing of new wind farms, potentially impacting the pipeline of future orders for suppliers like CS Wind.

- •Global Economic Conditions: Broader concerns of an economic slowdown could temper investment. However, government mandates for renewable energy, like those tracked by the International Energy Agency (IEA), often provide a powerful counter-cyclical buffer.

Investment Outlook: A Positive Thesis for CS Wind

Considering the contract’s positive implications, the validation of the company’s growth strategy, and its strengthened market position, the investment outlook for CS Wind Corporation remains strong. This deal serves as a powerful catalyst, reconfirming the company’s ability to execute and deliver value. The long-term demand for renewable energy infrastructure provides a durable tailwind for the entire sector.

Based on the available information, this development reinforces a BUY rating for CS Wind stock. Investors should focus on the company’s continued ability to secure large-scale orders, the successful integration of its offshore wind division, and its adept management of macroeconomic risks.

Disclaimer: This analysis is based on publicly available information. Investment decisions should be made at the investor’s own discretion and after conducting their own thorough research.