What Happened?

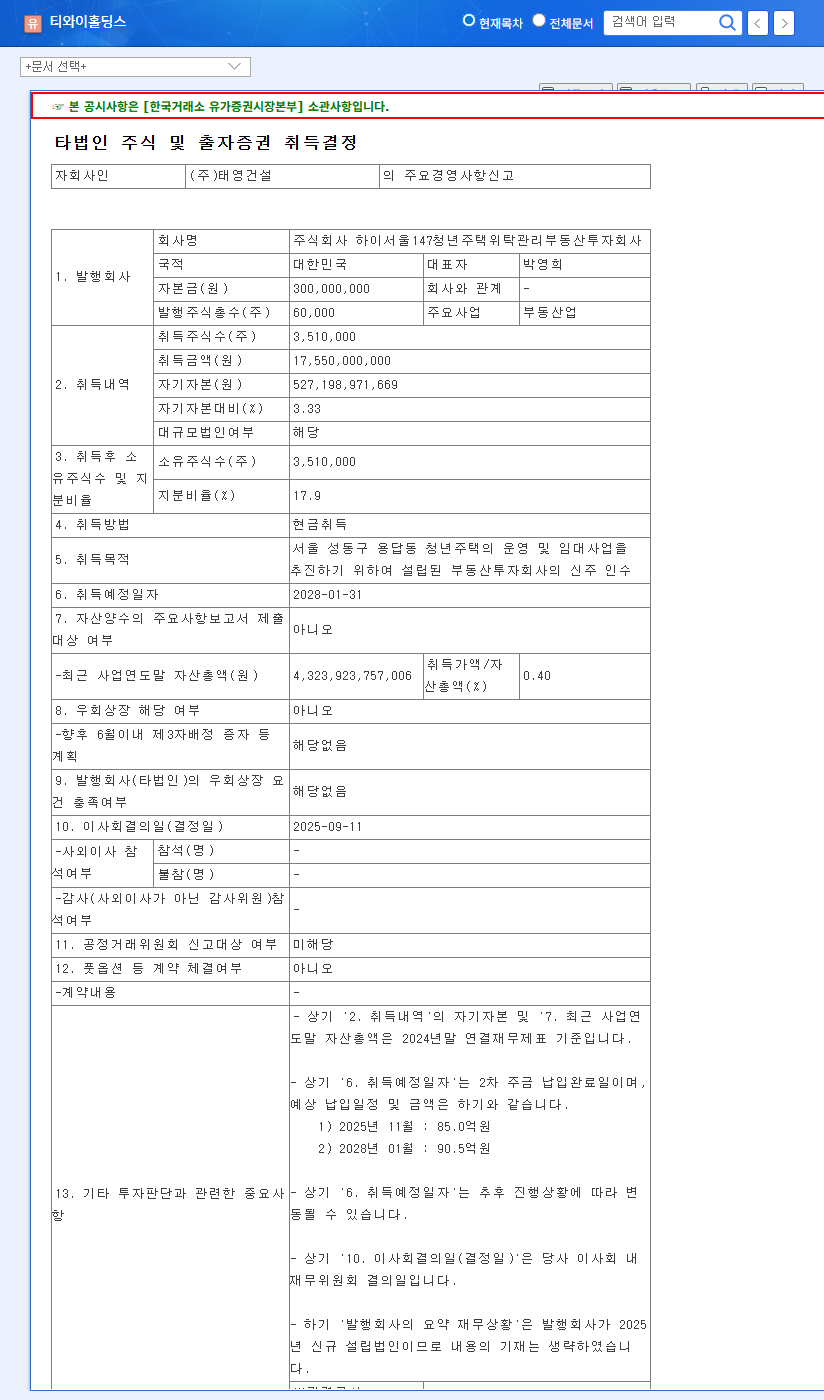

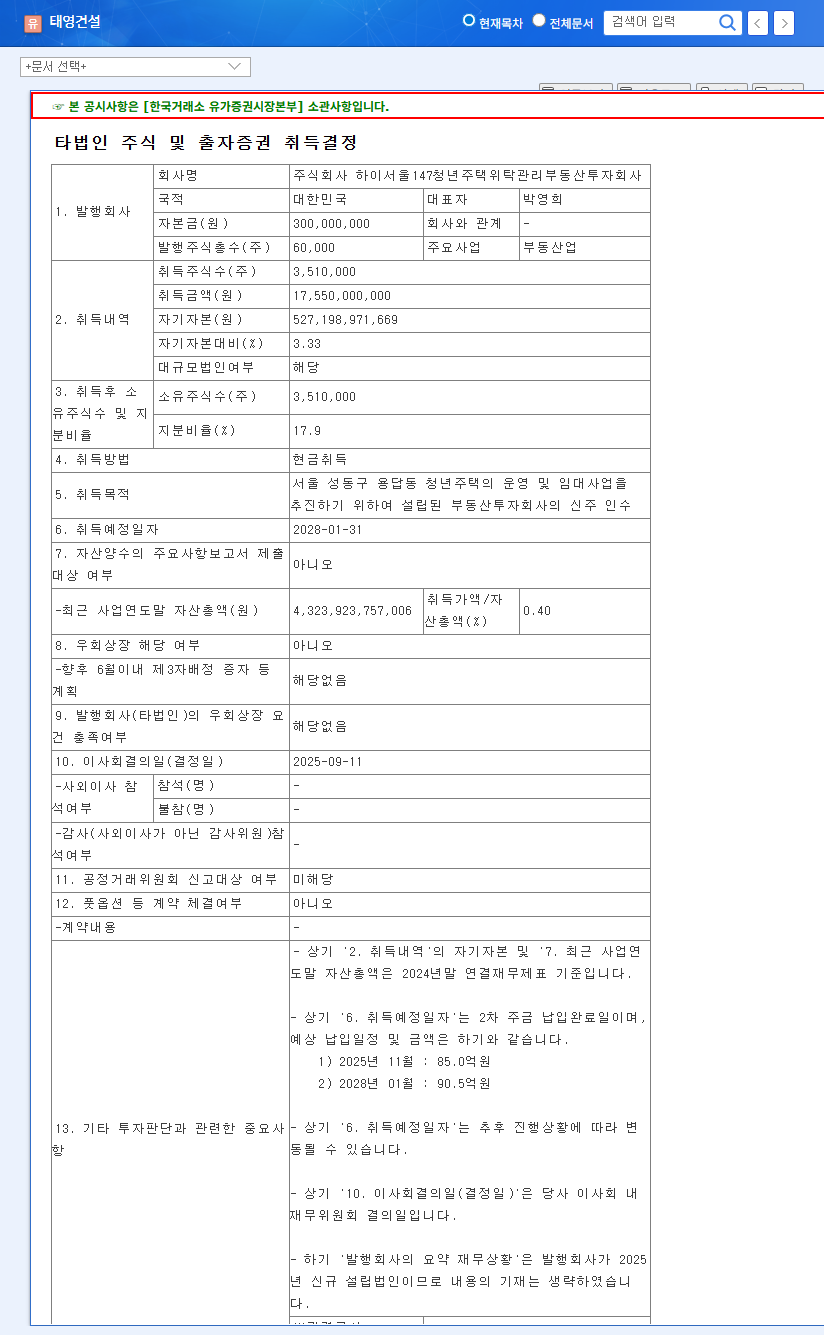

TY Holdings’ subsidiary, Taeyoung Construction, acquired a 17.9% stake in Hi Seoul 147 Youth Housing Management REIT for 17.6 billion won, marking its entry into the youth housing operation and rental business in Yongdap-dong, Seongdong-gu, Seoul.

Why Does It Matter?

TY Holdings is currently facing challenges due to Taeyoung Construction’s workout status and sluggish performance in its broadcasting, leisure, and logistics businesses. This investment presents a potential opportunity for new revenue streams and diversification. However, it also carries the risk of increased financial burden.

What’s the Potential Impact?

- • New business venture and portfolio diversification

- • Potential for long-term profitability improvement

- • Expansion of investments in related companies

- • Potential increase in financial burden

- • Uncertainty related to Taeyoung Construction’s workout

- • Uncertainties in operating and leasing the youth housing

- • Lack of market expectations

What Should Investors Do?

Investors should carefully consider the following factors before making investment decisions:

- • Progress and outlook of Taeyoung Construction’s workout proceedings

- • Actual performance and profitability of the youth housing project

- • TY Holdings’ financing capabilities and changes in its financial structure

- • Changes in the macroeconomic environment, such as interest rate fluctuations and real estate market trends

The youth housing venture represents both an opportunity and a risk for TY Holdings. Investors should carefully analyze both positive and negative factors, consider the company’s long-term strategy and market conditions, and make informed investment decisions.

FAQ

What are TY Holdings’ main businesses?

TY Holdings primarily manages and invests in its subsidiaries. Its main subsidiaries include SBS, Blue One, and DMC Media.

What is the current status of Taeyoung Construction?

Taeyoung Construction is currently undergoing workout proceedings.

How will this investment affect TY Holdings?

While it offers an opportunity for diversification and new revenue streams, it also carries the risk of increasing the company’s financial burden. Given Taeyoung Construction’s ongoing workout, a cautious approach is warranted.