Investors are closely examining the latest financial reports from WHANIN PHARM CO.,LTD, following a provisional Q3 2025 earnings announcement that fell short of market expectations. This development has introduced short-term uncertainty and requires a detailed WHANIN PHARM stock analysis to understand the full picture. While the initial numbers may seem concerning, a deeper dive reveals a company with robust fundamentals grappling with temporary cost pressures. This report will unpack the Q3 results, analyze the underlying corporate health, and provide a strategic outlook for investors navigating the current landscape of pharmaceutical stock performance.

WHANIN PHARM Q3 Earnings: The Numbers and The Miss

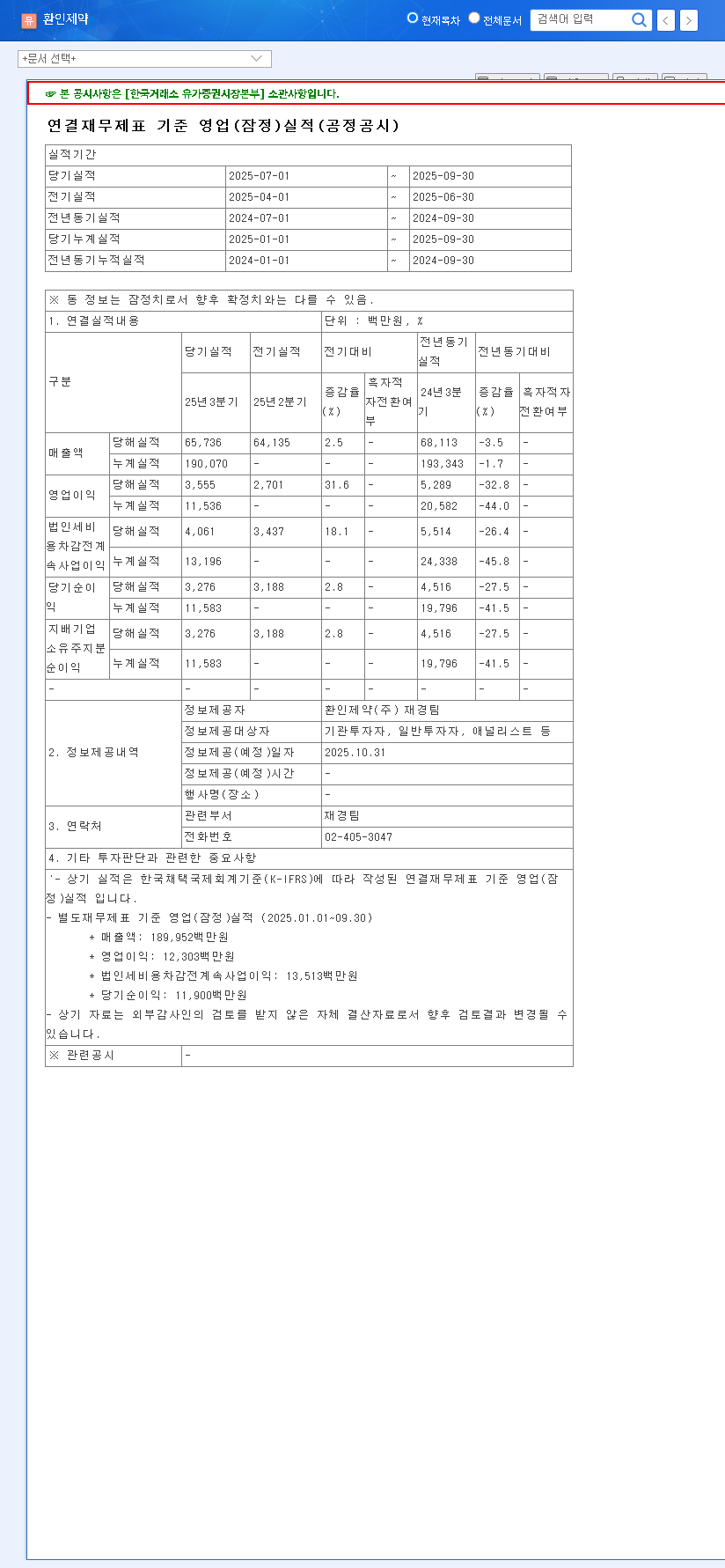

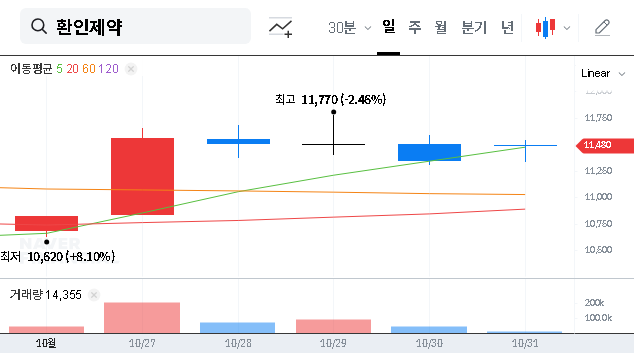

On October 31, 2025, WHANIN PHARM disclosed its provisional Q3 results, which immediately caught the market’s attention. The key figures revealed a gap between the company’s performance and prevailing analyst consensus:

- •Revenue: Reached KRW 65.7 billion, which was 5% below the market’s expectation of KRW 69.2 billion.

- •Operating Profit: Came in at KRW 3.6 billion, a significant 23% below the anticipated KRW 4.7 billion.

- •Net Profit: Reported at KRW 3.3 billion, for which no specific market expectation was available for direct comparison.

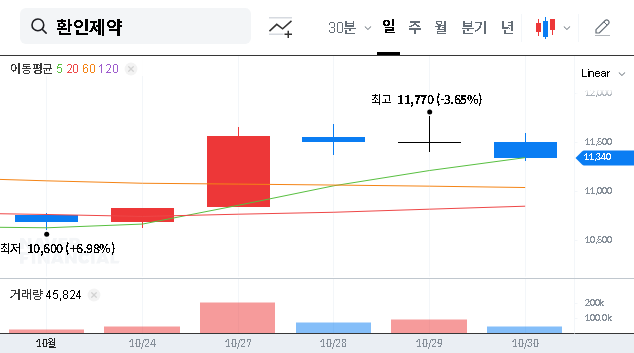

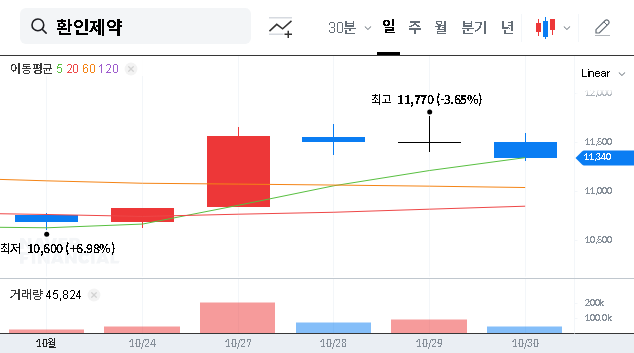

This earnings miss, particularly the substantial deviation in operating profit, is the primary catalyst for potential short-term stock volatility. When a company’s earnings fall short, it can signal to investors that its growth or profitability trajectory is not meeting prior assumptions, often leading to a recalibration of its valuation. For a comprehensive look at the official numbers, you can view the Official DART Disclosure.

Behind the Numbers: Analyzing Whanin Pharm Fundamentals

Cost Pressures vs. A Fortress Balance Sheet

The decline in profitability isn’t arbitrary. It can be traced to specific internal factors, primarily rising costs associated with growth. The company has seen an increase in inventory valuation allowances and higher production costs stemming from strategic investments in new factories in Anseong and Hyangnam. While these investments weigh on near-term profits, they are crucial for long-term capacity expansion and efficiency.

Despite these cost pressures, the core Whanin Pharm fundamentals remain exceptionally strong. The company boasts an impressively low debt-to-equity ratio of just 12.95%. This indicates a very stable financial structure that is not heavily reliant on borrowed capital, providing significant resilience against macroeconomic headwinds like rising interest rates. This financial health is a cornerstone of any long-term WHANIN PHARM stock analysis.

The central tension for investors is weighing temporary, investment-related cost increases against a backdrop of enduring financial stability and core business strength in neuropsychiatric drugs.

Growth Drivers and Strategic Partnerships

WHANIN PHARM continues to generate consistent revenue from its leadership position in neuropsychiatric treatments. Furthermore, its strategic partnership with global giant GSK to introduce new products represents a significant growth lever. The success of these new launches will be a critical factor in offsetting current cost pressures and driving future revenue growth. To better understand sector dynamics, it’s helpful to review our guide to investing in pharmaceutical stocks.

Outlook: Macro Factors and Investor Action Plan

Navigating the Macroeconomic Environment

Several external factors could influence pharmaceutical stock performance. For WHANIN PHARM, currency volatility (USD/KRW) is a key variable, as it can inflate the cost of imported raw materials. While stabilized logistics costs are a positive, the company’s low debt means it is relatively insulated from direct impacts of interest rate hikes—a significant advantage over more leveraged competitors. Continuous monitoring of these variables is essential, as highlighted by financial news outlets like Reuters.

Key Considerations for Investors

While the short-term outlook may be negative due to the earnings miss, a medium-to-long-term perspective requires careful monitoring of the following:

- •Profitability Management: Watch for signs that the company is successfully managing the costs from new investments and improving its operating margins in subsequent quarters.

- •New Product Pipeline: Track the revenue contribution from the GSK partnership and other new products. Are they gaining market traction?

- •Animal Pharmaceutical Business: Evaluate progress in this growth segment. Look for concrete investment plans, R&D updates, and market penetration.

- •Corporate Transparency: The company’s recent efforts to enhance disclosure are a positive sign. Continued transparency will help build long-term investor trust.

In conclusion, this WHANIN PHARM stock analysis suggests that while short-term caution is warranted, the company’s strong financial foundation and strategic growth initiatives provide a potential pathway for long-term value creation, contingent on successful execution and cost management.