The latest developments surrounding Hyundai Steel (004020) have investors asking critical questions. A significant stake reduction by the National Pension Service (NPS) has sent ripples through the market, casting a shadow over the company’s immediate prospects. This detailed Hyundai Steel stock forecast will dissect the implications of the NPS’s move, perform a comprehensive analysis of the company’s fundamentals from H1 2025, and explore the long-term strategic initiatives that could redefine its future. We’ll provide a clear-eyed view on whether this is a temporary setback or a sign of deeper issues, offering a data-driven investment strategy for 2025 and beyond.

The Catalyst: National Pension Service Reduces Its Stake

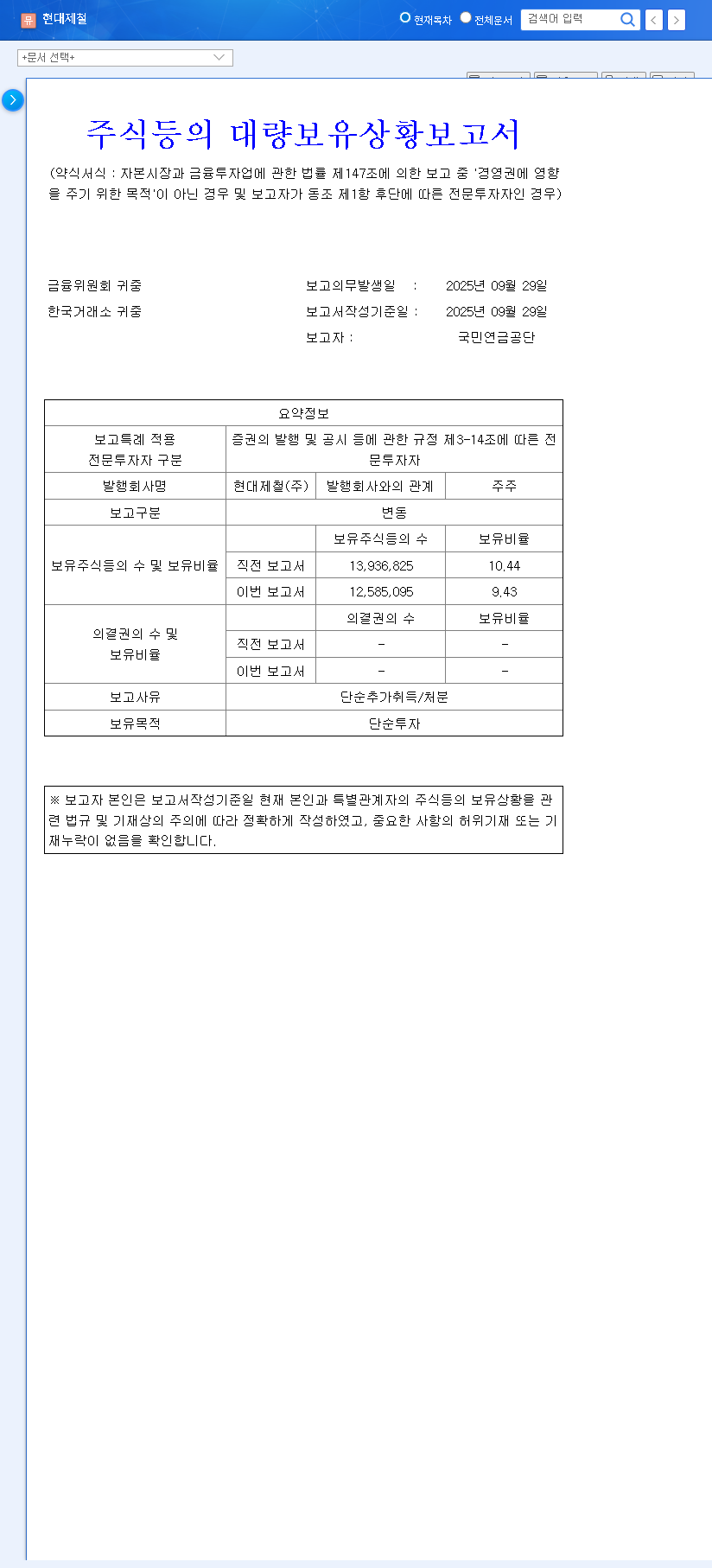

The primary trigger for recent market volatility was the disclosure that the National Pension Service (NPS), South Korea’s largest institutional investor, has trimmed its holdings in Hyundai Steel. The ownership stake was reduced from 10.44% to 9.43%, a decrease of just over one percentage point. According to the Official Disclosure (DART), the stated reason was for simple investment purposes, which is often interpreted as portfolio rebalancing or partial profit-taking.

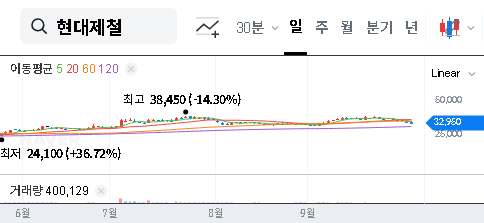

While labeled a routine adjustment, any sell-off by a major institutional holder like the NPS can create short-term downward pressure on a stock. It often prompts other market participants to re-evaluate their own positions, potentially leading to increased trading volume and heightened price volatility.

Financial Deep Dive: Analyzing H1 2025 Performance

To understand the context behind the NPS Hyundai Steel stake reduction, we must scrutinize the company’s recent financial health. The first half of 2025 painted a challenging picture, marked by declining profitability amid a sluggish global steel market.

Profitability Under Pressure

- •Revenue Dip: Consolidated revenue for H1 2025 fell to KRW 11.509 trillion, a slight year-over-year decrease.

- •Operating Profit Slump: More concerningly, operating profit plummeted to KRW 82.7 billion.

- •Net Loss: The company swung to a net loss of KRW 16.9 billion for the period.

These figures were primarily driven by lower sales prices for core flat and long steel products, coupled with weakened demand from key downstream industries. However, despite these headwinds, Hyundai Steel maintains a solid financial foundation with a debt-to-asset ratio of approximately 42.3%, indicating a stable balance sheet capable of weathering market cycles.

Future Growth Engine: The U.S. EAF Investment

The most significant positive catalyst for any long-term Hyundai Steel investment thesis is its ambitious expansion into the North American market. The company has announced a landmark USD 5.8 billion investment to build a state-of-the-art electric arc furnace (EAF) steel mill in Louisiana, USA. This facility will specialize in high-quality automotive steel sheets.

Why This Move is a Game-Changer

- •Tapping into the EV Market: The plant is strategically positioned to supply the burgeoning electric vehicle (EV) manufacturing hub in the U.S. Southeast.

- •Eco-Friendly Production: EAF technology has a significantly lower carbon footprint than traditional blast furnaces, aligning with global ESG trends and attracting environmentally conscious partners.

- •Long-Term Profitability: By producing high-value-added products in a high-demand market, this investment is designed to secure a new, powerful revenue stream for decades to come.

Investment Thesis & Strategic Outlook

Considering all factors, our current Hyundai Steel stock forecast points to a ‘Neutral’ rating. The short-term sentiment is dampened by weak H1 earnings and the NPS sell-off. However, the long-term potential anchored by the U.S. EAF project is undeniable. Investors must weigh the current headwinds against future growth opportunities. For more on the global market, reports from the World Steel Association provide excellent context.

Key Risks to Monitor

- •Continued stake sales from NPS or other institutions.

- •A prolonged global economic slowdown further depressing steel demand.

- •Volatility in raw material prices and currency exchange rates.

- •Potential delays or cost overruns in the new U.S. investment project.

Key Opportunity Factors

- •Successful execution of the U.S. EAF mill, securing a major foothold in the North American auto market.

- •Recovery in downstream industries (construction, shipbuilding) leading to increased demand.

- •Expansion of high-margin, eco-friendly steel products.

Investors should monitor corporate guidance for H2 2025 and track the progress of the North American project. For a broader perspective, see our comprehensive guide to investing in the industrial sector.

Disclaimer: This analysis is for informational purposes only. Investment decisions carry risk and should be made based on individual research and financial advice.