In the volatile world of construction and real estate, a single contract can signal a monumental shift in a company’s trajectory. For investors closely watching GS E&C stock (006360), the recent news of a massive project win is exactly that kind of signal. After a challenging period marked by financial setbacks, GS Engineering & Construction has secured a landmark deal that could redefine its future. This comprehensive GS E&C investment analysis will dissect this pivotal development, examining its potential to catalyze a turnaround and what it means for shareholders moving forward.

Project Breakdown: The ₩590.8B Ssangmun Station Contract

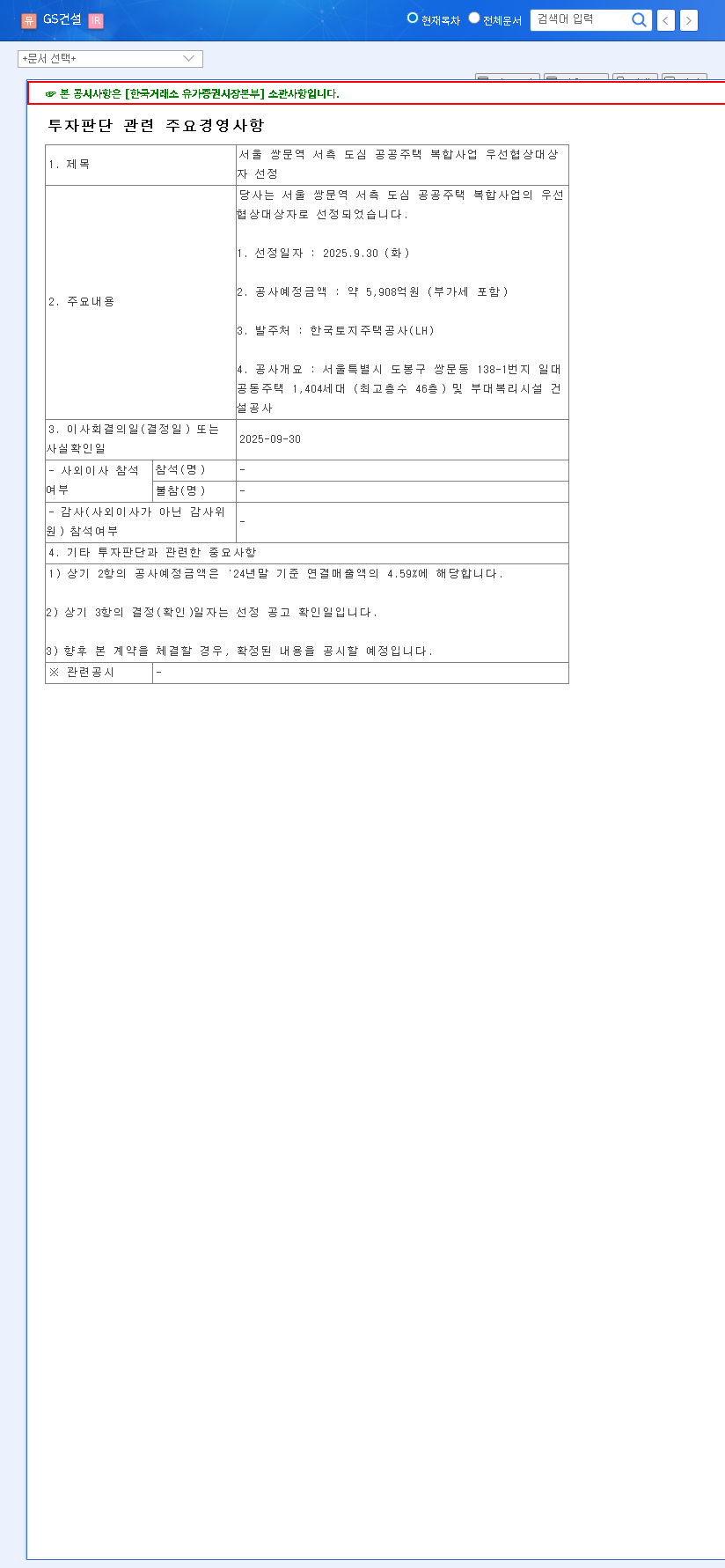

On October 1, 2025, GS E&C announced its selection as the preferred bidder for the ‘Seoul Ssangmun Station West Urban Public Housing Complex Project.’ Commissioned by the state-run Korea Land and Housing Corporation (LH), this is no ordinary contract. The project involves the construction of 1,404 apartment units, soaring up to 46 floors, along with ancillary welfare facilities in Seoul’s Dobong-gu district. The estimated construction cost stands at a staggering ₩590.8 billion (approx. $420 million USD), including VAT. This information was made public via an Official Disclosure, confirming the scale and legitimacy of the win.

The focus on urban public housing is strategic, aligning with government initiatives to increase housing supply in densely populated urban centers. For GS E&C, a leader in this domain, successfully executing the Ssangmun Station project will not only bolster its revenue but also reaffirm its technical expertise and market leadership in a core business segment.

The Critical Context: A Turnaround Story for GS E&C Stock?

This contract win couldn’t have come at a more crucial time. The company’s financial performance in 2023 was severely impacted by provisions for reconstruction costs related to the ‘Incheon Geomdan accident,’ an event that eroded investor confidence and profitability. While 2022 was a solid year, 2023 saw revenue dip to ₩82.3 billion and the operating profit margin plummet to a mere 1.78%. This new ₩590.8 billion contract is, remarkably, over seven times the company’s entire 2023 revenue. This sheer scale provides a clear and powerful pathway to financial recovery.

The Ssangmun Station project is more than just another entry in the order book; it’s a potential turning point that could restore profitability, rebuild market trust, and provide significant positive momentum for the GS E&C stock price.

Macroeconomic Tailwinds and Headwinds

While the contract itself is domestic, no construction project exists in a vacuum. Broader economic trends will play a vital role. The global interest rate environment, with central banks contemplating rate freezes or cuts, is favorable. A stable or declining interest rate could significantly reduce financing costs for a project of this magnitude, directly benefiting the bottom line. Furthermore, recent trends show a stabilization in key input costs. As noted in global economic reports from Reuters, declining crude oil prices and shipping indexes suggest that logistics and raw material price pressures may be easing, which is a significant positive for construction cost management.

Comprehensive GS E&C Investment Analysis (006360)

Investors evaluating 006360 stock must weigh the tremendous potential of this new contract against the company’s recent history and inherent industry risks. Here’s a balanced breakdown.

The Bull Case: Key Opportunities

- •Massive Revenue Injection: This project fundamentally strengthens the order backlog, providing clear revenue visibility and a path to significant growth over the next few years.

- •Profitability Restoration: If executed efficiently within budget, the project promises to dramatically improve operating margins that were decimated in 2023.

- •Market Confidence Boost: Successfully delivering a high-profile public housing project will help resolve lingering doubts from past issues and restore faith in the company’s execution capabilities. For more context, you can read our guide on evaluating construction company financials.

The Bear Case: Significant Risks to Monitor

- •Execution Risk: The gap between winning a bid and profitable completion is large. Any delays, cost overruns, or permitting issues could erode the project’s profitability.

- •Lingering Reputational Damage: The shadow of the ‘Incheon Geomdan accident’ remains. This project will be under intense scrutiny, and any missteps in quality control could have an outsized negative impact.

- •Macroeconomic Volatility: While currently favorable, a sudden spike in inflation, interest rates, or raw material prices could compress margins unexpectedly.

Final Verdict: Is GS E&C Stock a Buy?

The selection for the Seoul Ssangmun Station West project is undeniably a powerful positive catalyst for GS E&C stock. It offers a tangible and substantial opportunity for the company to overcome recent hardships and secure a robust growth engine for the future. Our investment opinion is Cautiously Positive.

While the news provides a strong short-term tailwind, prudent investors should closely monitor the company’s execution. Key metrics to watch include the final contract signing, quarterly progress reports, and margin performance. If GS E&C can demonstrate rigorous quality control and efficient project management, this win could indeed mark the beginning of a sustained and profitable turnaround.