When MECARO.CO.,LTD. announced the disposal of treasury shares, it may have caused a ripple of curiosity among investors. However, this comprehensive MECARO stock analysis delves beyond the headlines to uncover the true value proposition of the company. We will dissect the minor stock option news, explore the company’s robust financial health, dominant market position, and chart a course for a sound MECARO investment strategy based on its powerful fundamentals and the surrounding macroeconomic environment.

Deconstructing the Treasury Stock News: A Non-Event

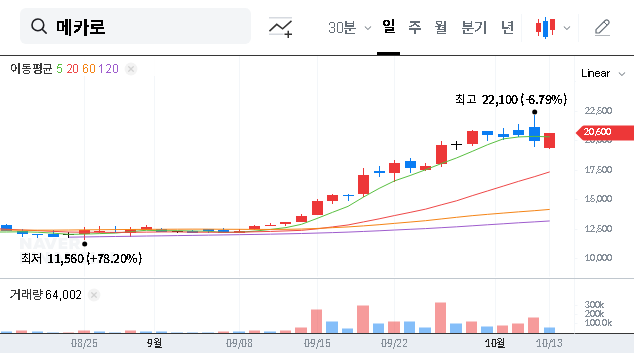

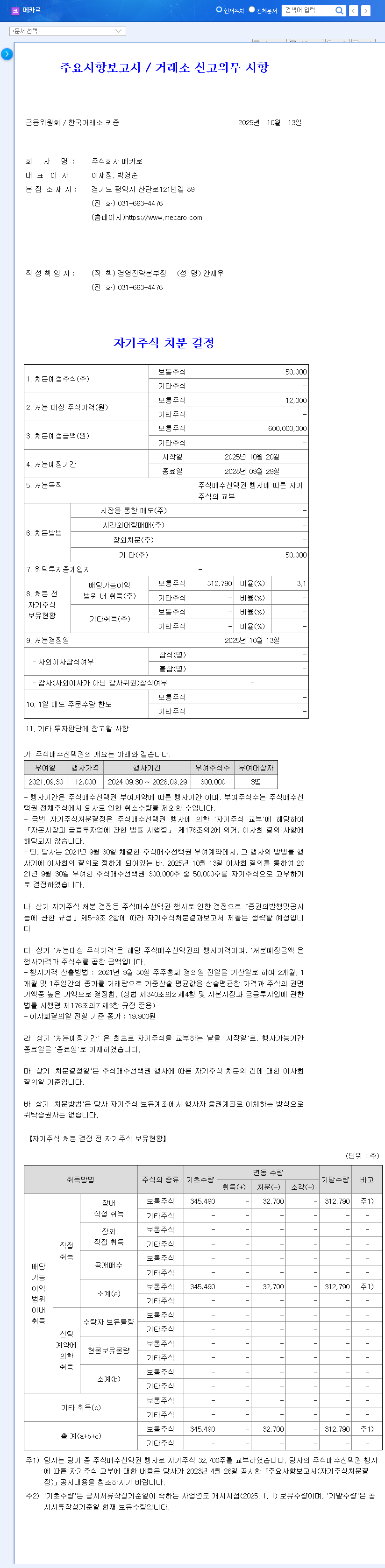

On November 13, 2025, MECARO.CO.,LTD. announced its decision to dispose of 3,000 treasury shares resulting from the exercise of stock options. While such announcements can sometimes signal significant shifts, in this case, the volume is negligible, representing a mere 0.03% of total outstanding shares. This action is best understood as a routine administrative process for employee compensation—a standard tool to incentivize and retain talent. The details of this stock option exercise were confirmed in an Official Disclosure on DART. For discerning investors, this news has minimal bearing on the company’s intrinsic value and should not trigger any short-term trading decisions.

In-Depth MECARO Stock Analysis: The Core Strengths

To truly evaluate a potential MECARO investment, one must look past minor events and focus on the company’s powerful underlying fundamentals, which paint a very compelling picture.

Stellar H1 2025 Performance & Profitability

The first half of 2025 was a landmark period for MECARO. The company not only returned to profitability but did so with explosive growth. Consolidated revenue hit KRW 44.4 billion, with an operating profit of KRW 6.7 billion. More impressively, net profit soared to KRW 7.2 billion—a staggering 15-fold increase year-over-year. This remarkable turnaround was fueled by the resurgence in the semiconductor market, strategic expansion of overseas sales, and beneficial foreign exchange rates.

A 15-fold increase in net profit is not just a number; it’s a testament to MECARO’s operational excellence and its ability to capitalize on favorable market conditions, solidifying its strong financial footing.

Dominant Core Business & Future Growth Engines

MECARO’s stability is anchored by its Heater Block business, which constitutes over 98% of its total sales. The company’s dominance is undeniable, holding an estimated 90% share of the domestic market. This creates a high barrier to entry and a reliable revenue stream. However, MECARO is not resting on its laurels. The company is actively investing in future growth by:

- •Developing advanced Aluminum Nitride (AlN) ceramic components, which are critical for next-generation semiconductor manufacturing processes.

- •Expanding into the renewable energy sector with its solar cell business through MECARO Energy.

- •Strategically discontinuing non-core operations, like its valve business, to sharpen its focus and optimize resource allocation.

Impeccable Financial Stability

A cornerstone of the positive MECARO fundamentals is its exceptionally strong balance sheet. With a debt-to-equity ratio of just 7.03%, the company operates with virtually no financial leverage, making it highly resilient to economic downturns and rising interest rates. This financial prudence provides a solid foundation for sustainable growth and future investment.

Macroeconomic Outlook: Tailwinds and Headwinds

MECARO’s performance is also influenced by broader economic trends. A favorable USD/KRW exchange rate has been a significant tailwind, boosting the value of its substantial overseas sales. Furthermore, recent cuts in benchmark interest rates in both the U.S. and Korea could lower financing costs and spur investment across the broader technology sector. However, investors must remain vigilant about potential headwinds, such as volatility in international oil prices and rising logistics costs, which could exert pressure on profit margins. Understanding these dynamics is crucial for anyone looking to invest in semiconductor industry stocks.

A Sound Investment Strategy for MECARO

Given the comprehensive MECARO stock analysis, the treasury share disposal is a non-factor. The investment thesis rests squarely on the company’s robust fundamentals and future growth trajectory.

- •Short-Term Perspective: Investors should monitor macroeconomic data, particularly exchange rates, and look for signs of continued strength in the semiconductor industry. The stock is unlikely to experience major volatility from company-specific news alone.

- •Mid-to-Long-Term Perspective: The key catalysts for long-term growth will be the successful commercialization of its new ventures in AlN ceramics and solar energy. An investor’s focus should be on quarterly reports to confirm that the impressive H1 2025 performance is sustainable and that these new growth engines are beginning to contribute meaningfully to the top line.

In conclusion, MECARO presents a compelling case for investors who prioritize strong fundamentals, market leadership, and prudent financial management. While external risks exist, the company’s core strengths position it well for continued success.

Disclaimer: This report is based on publicly available information and is intended for informational purposes only. It does not constitute investment advice. All investment decisions should be made at your own discretion after careful consideration.