The recent news that South Korea’s National Pension Service (NPS) has significantly reduced its holding in HanaTour stock (039130) has sent ripples of concern through the investment community. As the nation’s largest institutional investor, any major move by the NPS is scrutinized for deeper meaning. Does this divestment signal a fundamental problem with HanaTour, or is it merely a strategic portfolio adjustment? For current and prospective investors, this event demands a thorough HanaTour stock analysis to separate short-term market noise from long-term value indicators.

This comprehensive guide will dissect the NPS’s decision, evaluate HanaTour’s current financial health, analyze the market impacts, and provide actionable strategies for investors navigating this period of uncertainty. Our goal is to equip you with the insights needed to make an informed HanaTour investment decision.

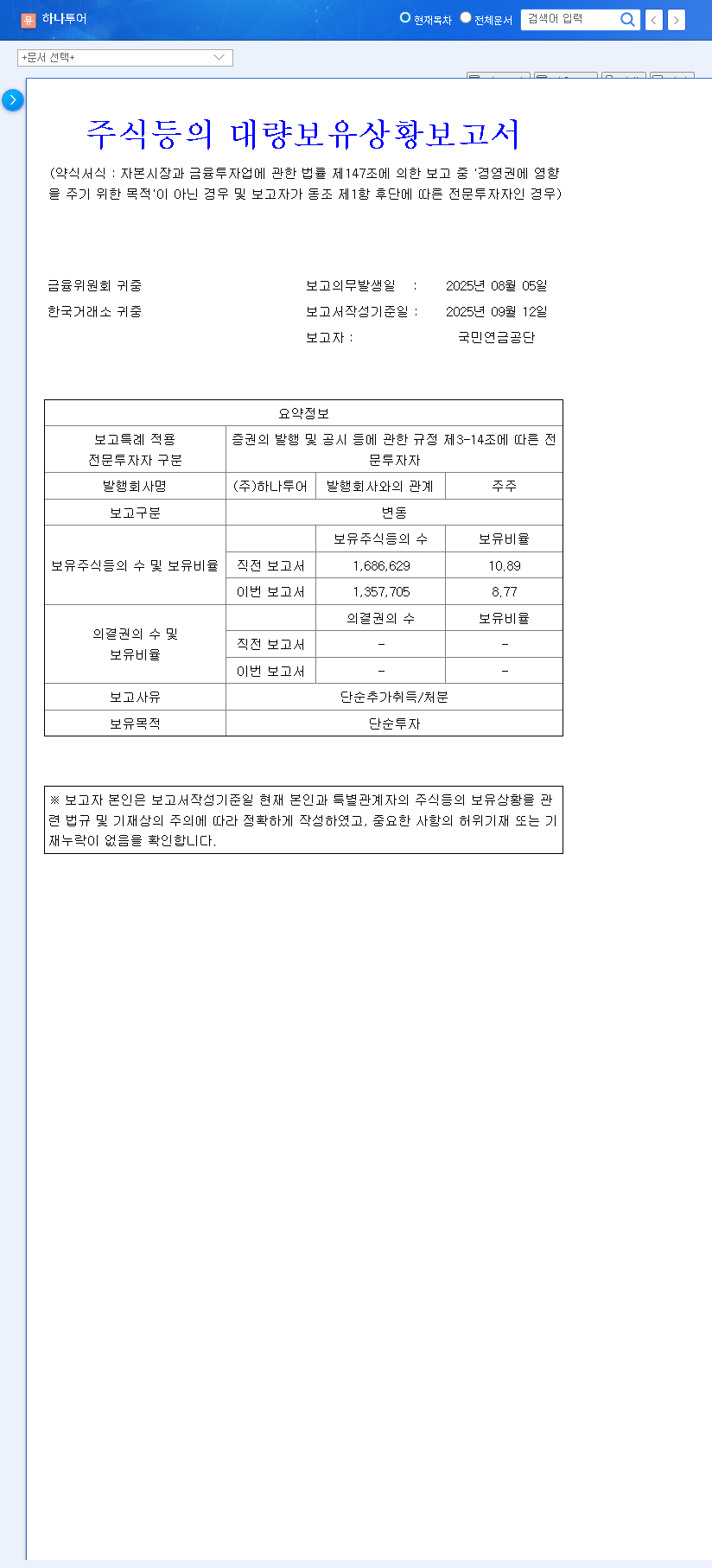

The Catalyst: Deconstructing the NPS Stake Reduction

On October 1, 2025, a regulatory filing revealed that the National Pension Service had decreased its stake in HanaTour from 10.89% to 8.77%, a notable reduction of 2.12 percentage points. The transaction details were made public via an Official Disclosure on the DART system, confirming the shift in ownership.

What Does ‘Simple Investment’ Purpose Mean?

Crucially, the NPS cited the purpose of the sale as ‘simple investment.’ This classification is important. It suggests the decision was not driven by a negative assessment of HanaTour’s management or long-term prospects. Instead, it likely stems from standard institutional portfolio management practices, which can include:

- •Profit-Taking: Selling a portion of a position after a period of price appreciation to lock in gains.

- •Portfolio Rebalancing: Reducing exposure to the travel sector to reallocate capital to other industries with perceived higher growth potential, such as technology or renewable energy.

- •Risk Management: Trimming positions in response to macroeconomic uncertainties that could impact the travel industry, like fluctuating exchange rates or rising fuel costs.

Such strategies are common among large funds and, as explained by financial experts at sources like Reuters, do not necessarily reflect a bearish outlook on the specific company.

HanaTour’s Financial Health: A Fundamental Checkup

While the NPS HanaTour sale may be neutral, HanaTour’s underlying fundamentals present a mixed picture. The H1 2025 results highlight existing challenges:

H1 2025 Performance Snapshot:

Revenue: 288.388B KRW (▼5.27% YoY)

Operating Profit: 21.932B KRW (▼13.27% YoY)

Net Income: 25.511B KRW (▼31.22% YoY)

Debt-to-Equity Ratio: 269.69%

Profitability Pressures and Debt Concerns

The year-over-year declines in revenue and profit suggest that the post-pandemic travel boom may be normalizing or facing new headwinds. More concerning is the high debt-to-equity ratio of nearly 270%. This level of leverage makes the company highly sensitive to interest rate fluctuations and can limit its financial flexibility for future investments and acquisitions. For the HanaTour stock price to appreciate sustainably, the company must demonstrate a clear path to improving profitability and strengthening its balance sheet.

Navigating the Future of HanaTour Stock

The market’s reaction will likely be bifurcated. In the short term, technical factors and sentiment will dominate, while long-term value will be dictated entirely by fundamental performance and strategic execution.

Short-Term Impact: Supply Overhang and Sentiment Shift

A large institutional sale creates a ‘supply overhang,’ which can exert downward pressure on the stock price as the market absorbs the new shares. This can trigger algorithmic selling and weaken retail investor sentiment, leading to increased volatility. Traders should be prepared for price fluctuations and heightened trading volumes in the weeks following the disclosure.

Long-Term Outlook: The Pivot to Digital is Key

In the long run, the success of a HanaTour investment hinges on the company’s ability to innovate beyond its traditional travel package model. The company’s push toward diversification through location-based services and e-commerce platforms is critical. Success here could unlock new, higher-margin revenue streams and prove to the market that HanaTour is evolving into a modern travel-tech company. The progress of these new ventures, not the NPS’s current holdings, will be the true driver of future shareholder value. For broader context, investors may want to read a deep dive into the travel industry’s post-pandemic recovery.

Actionable Investment Strategy

Investors should tailor their approach based on their time horizon.

- •Short-Term Traders: Monitor technical indicators, trading volume, and news flow closely. The increased volatility may present short-term trading opportunities, but risk management through stop-loss orders is essential.

- •Long-Term Investors: Look past the immediate noise. Focus on quarterly earnings reports for signs of a turnaround in core business performance. Scrutinize management commentary on debt reduction plans and the monetization progress of new digital ventures.

In conclusion, the NPS stake reduction is a significant data point but not a definitive verdict on HanaTour’s future. It serves as a catalyst for investors to re-evaluate their thesis. The real story for HanaTour stock will be written in its ability to improve its financial health and successfully execute its digital transformation strategy in a challenging macroeconomic environment.