Hotel Shilla 2025 Q3 Earnings: A Comprehensive Breakdown

The latest Hotel Shilla earnings report for Q3 2025 has sent ripples through the investment community, revealing a performance that fell significantly short of market consensus. This detailed Hotel Shilla analysis unpacks the preliminary results, examining the persistent headwinds in the crucial Travel Retail (TR) division against the encouraging resilience of the Hotel & Leisure segment. For investors holding or watching Hotel Shilla stock, understanding these dynamics is paramount.

With operating profit missing estimates by 37%, the report highlights a challenging quarter. This analysis dissects what happened, why, and the critical factors that will shape the company’s future trajectory and stock valuation.

The Numbers: 2025 Q3 Performance vs. Expectations

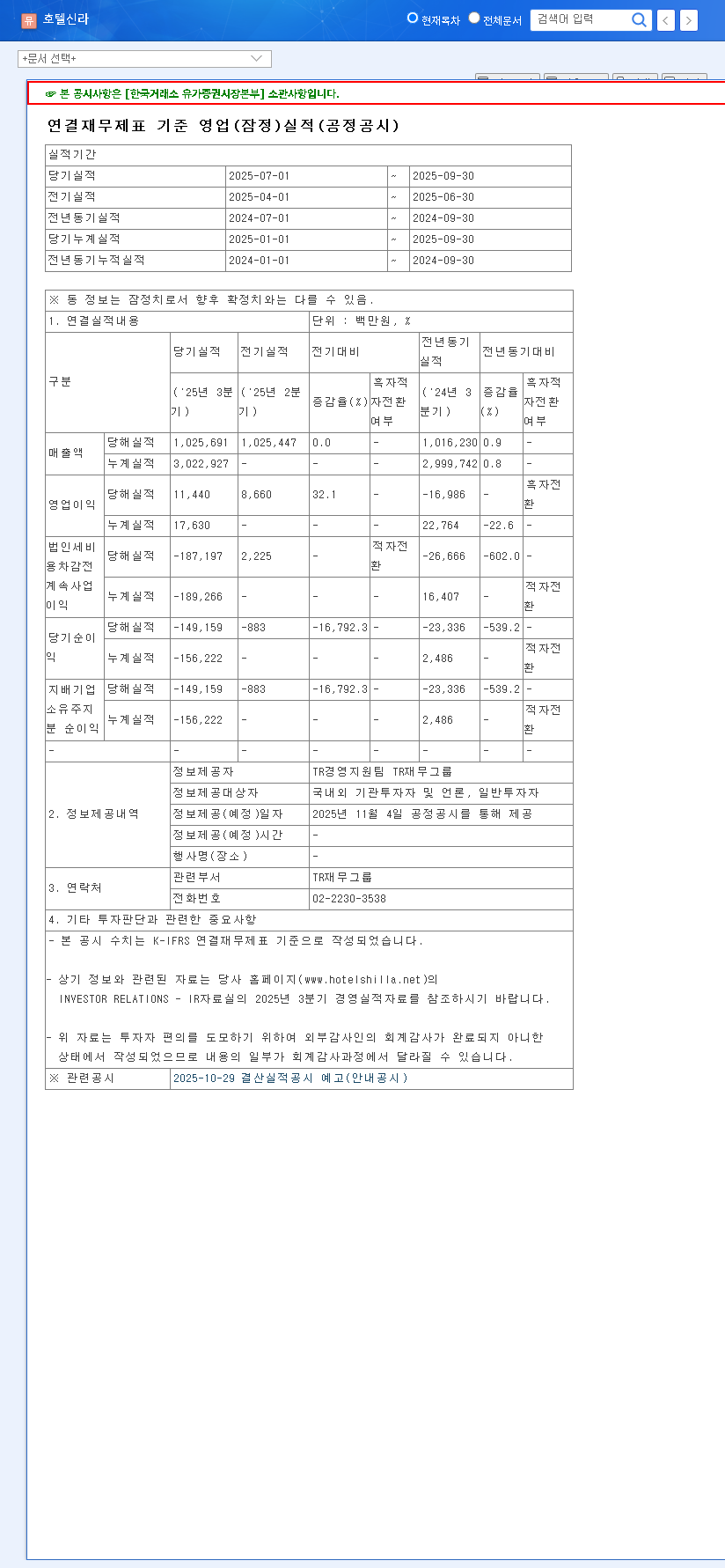

HOTEL SHILLA CO.,LTD’s preliminary financial results for the third quarter of 2025 were a clear disappointment for the market. The significant miss on key profitability metrics signals underlying pressures that require close scrutiny.

- •Revenue: 1,025.7 billion KRW (5% below market expectation of 1,076.0 billion KRW)

- •Operating Profit: 11.4 billion KRW (a staggering 37% below market expectation of 18.0 billion KRW)

- •Net Income: -149.2 billion KRW (a significant loss, 111% below the expected loss of -70.8 billion KRW)

The severity of the miss, particularly in operating and net income, is expected to weigh heavily on investor sentiment in the short term. For a granular look at the financials, investors can review the company’s Official Disclosure on DART.

Divisional Deep Dive: A Tale of Two Segments

The Struggling Travel Retail (TR) Division

The duty-free business, historically the engine of Hotel Shilla’s growth, remains its biggest challenge. The operating losses in the Travel Retail division are not a new phenomenon but a continuation of structural issues exacerbated by the current economic climate. The core problems include:

- •Slow Chinese Tourist Recovery: The anticipated wave of returning Chinese group tourists has been more of a trickle, with individual travelers showing more cautious spending habits. The large-scale reseller (‘daigou’) market has also shifted, reducing high-volume sales.

- •Intense Competition: The Korean duty-free landscape is fiercely competitive. This environment, combined with high fixed costs like airport rents, squeezes margins and makes profitability a constant battle.

- •Adverse Exchange Rates: An appreciating KRW against the USD negatively impacts the cost of goods sold for imported products and diminishes the price advantage for foreign shoppers.

The Resilient Hotel & Leisure Division

In stark contrast, the Hotel & Leisure segment has been a pillar of strength. Capitalizing on the post-pandemic travel boom, this division has posted consistent growth. Strong occupancy rates and higher average daily rates (ADR) at its flagship properties, The Shilla Seoul and Shilla Jeju, have been major contributors. The strong KRW has also incentivized domestic travel, channeling more demand towards high-end local resorts and boosting this division’s performance, partially offsetting the gloom from the TR side.

Macroeconomic Headwinds Impacting the Hotel Shilla Analysis

The broader economic environment, as detailed by sources like global economic reports, is a double-edged sword for Hotel Shilla. High interest rates are increasing the company’s debt servicing costs, directly impacting the bottom line and contributing to the large net loss. Meanwhile, volatile exchange rates and fluctuating commodity prices create uncertainty in both operational costs and consumer demand patterns.

Investment Outlook: What’s Next for Hotel Shilla Stock?

Given the disappointing Hotel Shilla earnings, investors must adopt a cautious and analytical approach. The short-term outlook for the Hotel Shilla stock is likely to be bearish. However, a medium-to-long-term view requires monitoring several key factors:

- •TR Profitability Strategy: Can management successfully renegotiate airport leases, optimize merchandising, and attract a more diverse customer base beyond Chinese tour groups?

- •Source of Net Loss: A thorough investigation is needed to see if the net loss is due to one-off impairments or reflects a sustained deterioration in financial health.

- •Pace of Chinese Tourism Recovery: This remains the single most significant variable for the TR division’s revival. Any positive policy changes or travel trends from China could be a powerful catalyst.

While the current results are concerning, the strength of the Hotel & Leisure brand and the potential for an eventual TR recovery could present long-term value. Investors should stay informed by reading the full quarterly report and learning more about the intricacies of the Korean duty-free market dynamics before making any decisions.