This comprehensive RedcapTour Co., Ltd. IR Analysis provides investors with a detailed preview of the upcoming online Investor Relations (IR) event scheduled for November 19, 2025. As the company navigates a complex macroeconomic landscape, this event, organized by the Korea Exchange, represents a pivotal moment for management to articulate its vision and address pressing shareholder questions. We will delve into the dual narrative of RedcapTour: the robust, high-growth engine of its rent-a-car division and the potential turnaround story of its travel business.

Our goal is to equip you with the insights needed to critically evaluate the company’s performance, understand its strategic direction, and make informed investment decisions. This report breaks down the H1 2025 financial results, analyzes key market drivers, and outlines the critical questions that will likely define the success of the IR event.

Event Overview: What to Expect on November 19, 2025

RedcapTour is set to host its online IR session at 2 PM KST. The agenda promises a thorough company introduction, a detailed breakdown of its core business segments—RedcapTour rent-a-car and RedcapTour travel business—and an interactive Q&A session. This is a prime opportunity for the market to gain clarity on corporate strategy and value directly from the source. For official filings, investors can refer to the Official Disclosure (DART).

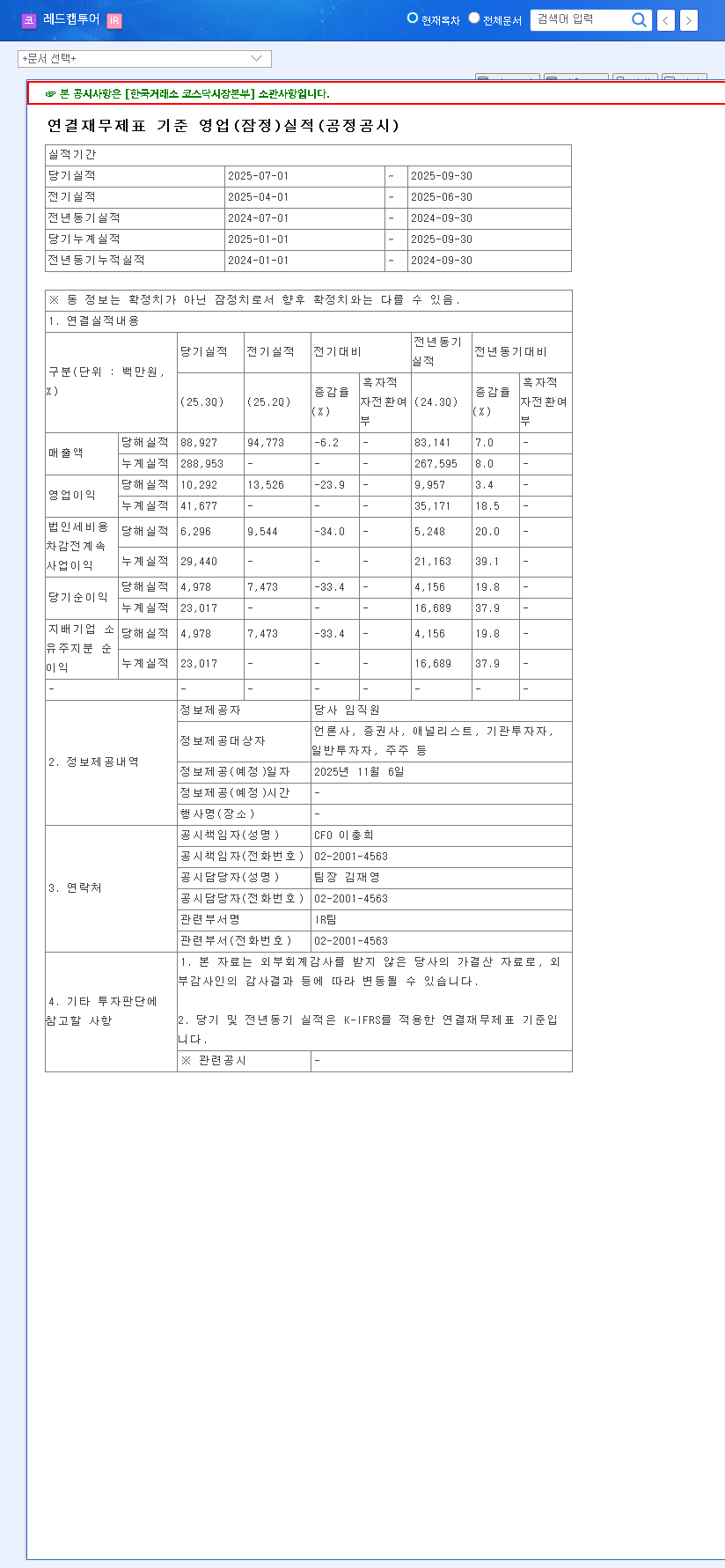

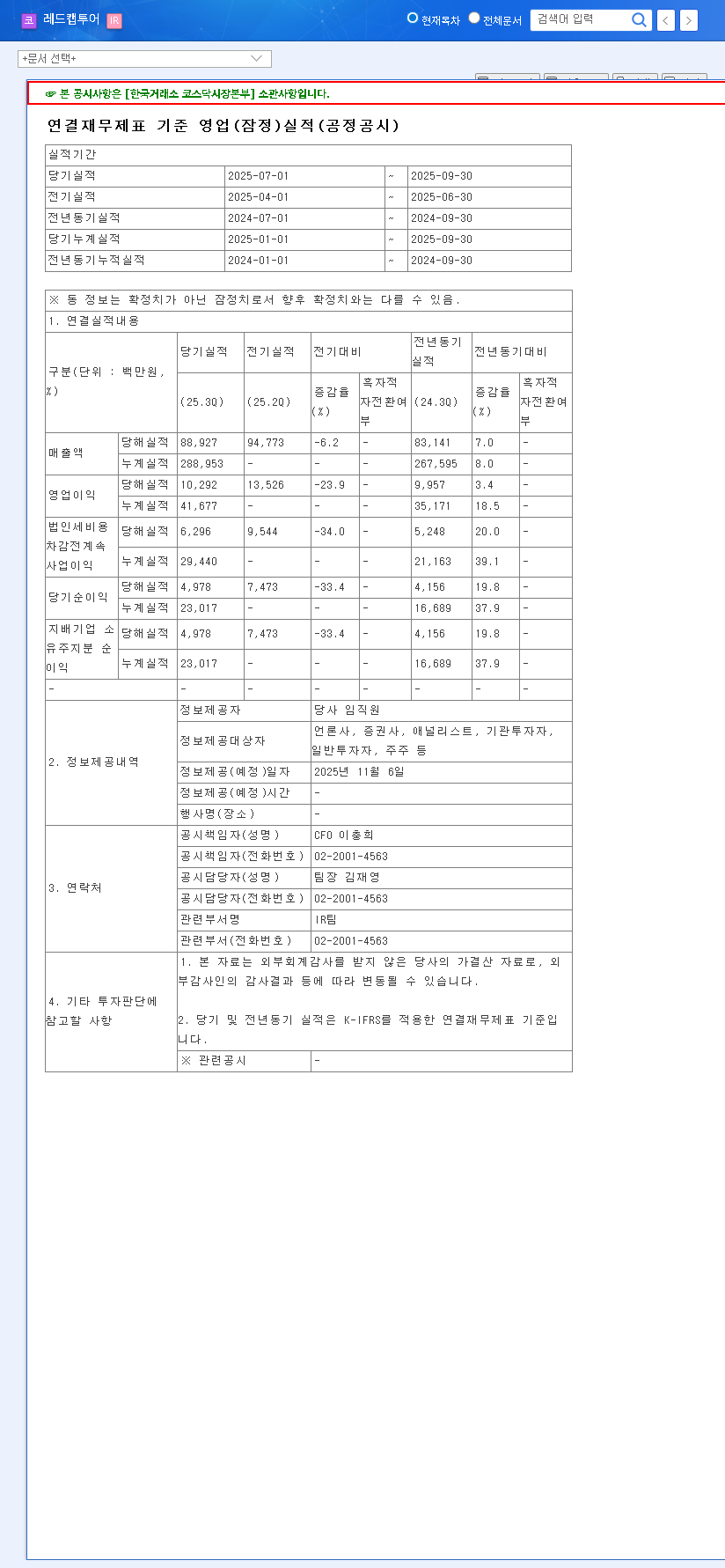

In-Depth Financial Analysis of RedcapTour H1 2025

The first half of 2025 painted a picture of divergence. While the rent-a-car segment fired on all cylinders, the travel arm faced headwinds, even as it improved profitability. Understanding these dynamics is central to a complete RedcapTour financial analysis.

Rent-a-Car Business: The Growth Juggernaut

The rent-a-car division continues to be the company’s crown jewel, demonstrating impressive resilience and growth. The focus on long-term rental contracts has created a stable, recurring revenue stream that is less susceptible to short-term market shocks.

- •Revenue: Reached KRW 179.17 billion, a significant 9.6% increase year-over-year.

- •Operating Profit: Surged to KRW 27.20 billion, marking a powerful 26.8% YoY growth.

- •Strategic Advantage: The company’s market position is bolstered by a modern fleet and superior service, driving customer loyalty and market share expansion.

Travel Business: A Story of Profitability Over Volume

While revenue saw a minor dip, the travel segment showcased commendable operational efficiency. The partnership with AMEX appears to be paying dividends, shifting the focus towards higher-margin, premium services. For more context, you can read our comprehensive guide to analyzing travel sector stocks.

- •Revenue: Declined slightly by 3.0% YoY to KRW 20.85 billion.

- ••Operating Profit: Increased by a healthy 9.6% YoY to KRW 4.18 billion, indicating improved margins.

- •Future Outlook: The key challenge is reigniting top-line growth while preserving these hard-won profitability gains amidst fluctuating travel demand.

The core tension for investors is clear: Can RedcapTour’s new ventures and travel segment recovery provide enough momentum to complement the already powerful rent-a-car business, justifying a higher valuation for the RedcapTour stock?

Navigating Macroeconomic Headwinds & Financial Health

No RedcapTour Co., Ltd. IR Analysis would be complete without scrutinizing the external risks and internal financial structure. The company faces several macroeconomic pressures that investors must monitor.

- •Currency Risk: A weaker Korean Won could impact its Chinese subsidiary’s earnings.

- •Interest Rates: While stable short-term rates are a positive, rising long-term bond yields could increase future financing costs. For updates, investors often follow reports from sources like Bloomberg’s market analysis.

- •Operating Costs: Rising oil prices and freight costs directly pressure the margins of both the rent-a-car and travel segments.

- •Financial Health: The debt-to-equity ratio has crept up to 245.6%, and a high dividend payout has reduced total equity. While short-term liquidity is not a concern, a clear plan for managing this leverage will be expected.

Key Investor Questions for the IR Event

A successful IR hinges on management’s ability to provide transparent and convincing answers. Here are the critical areas investors should focus on during the Q&A:

1. Strategy for New Growth Engines

The company has entered the used car import/export and information services sectors. What is the specific roadmap for monetization? What are the expected revenue contributions and synergy effects with existing businesses over the next 2-3 years?

2. Financial Prudence and Capital Allocation

What is the plan to manage the 245.6% debt-to-equity ratio? How does the board justify the high dividend payout in light of decreasing operating cash flow and rising leverage? Will this capital allocation strategy change?

3. Travel Business Turnaround Plan

Beyond improving margins, what concrete steps are being taken to reverse the revenue decline in the travel segment? How is the company positioning itself against fierce competition in a post-pandemic travel market?

4. Macroeconomic Risk Mitigation

What specific hedging strategies or operational adjustments are in place to counter the negative impacts of currency fluctuations, rising oil prices, and potential interest rate hikes?

Ultimately, this IR event is RedcapTour’s platform to reassure investors. By effectively communicating the strengths of its core businesses and providing a clear, credible vision for tackling its challenges, the company has an opportunity to positively influence its market valuation and build long-term shareholder trust.