This comprehensive EnGIS Technologies share price forecast delves into the critical factors shaping the future of stock ticker 208860. With its trading resumption on the horizon for July 7, 2025, investors are closely watching the recent shareholding adjustments by its largest shareholder, DASAN Networks. We will dissect the company’s fundamentals, analyze the transformative acquisition of DMC Co., Ltd., and weigh the significant financial risks to provide a clear, data-driven outlook for potential investors.

Understanding the nuances of EnGIS Technologies’ fundamentals is more critical than ever, especially after a prolonged stock trading suspension. This analysis serves as an essential guide to navigating the opportunities and risks associated with its much-anticipated return to the market.

Unpacking the Shareholding Changes by DASAN Networks

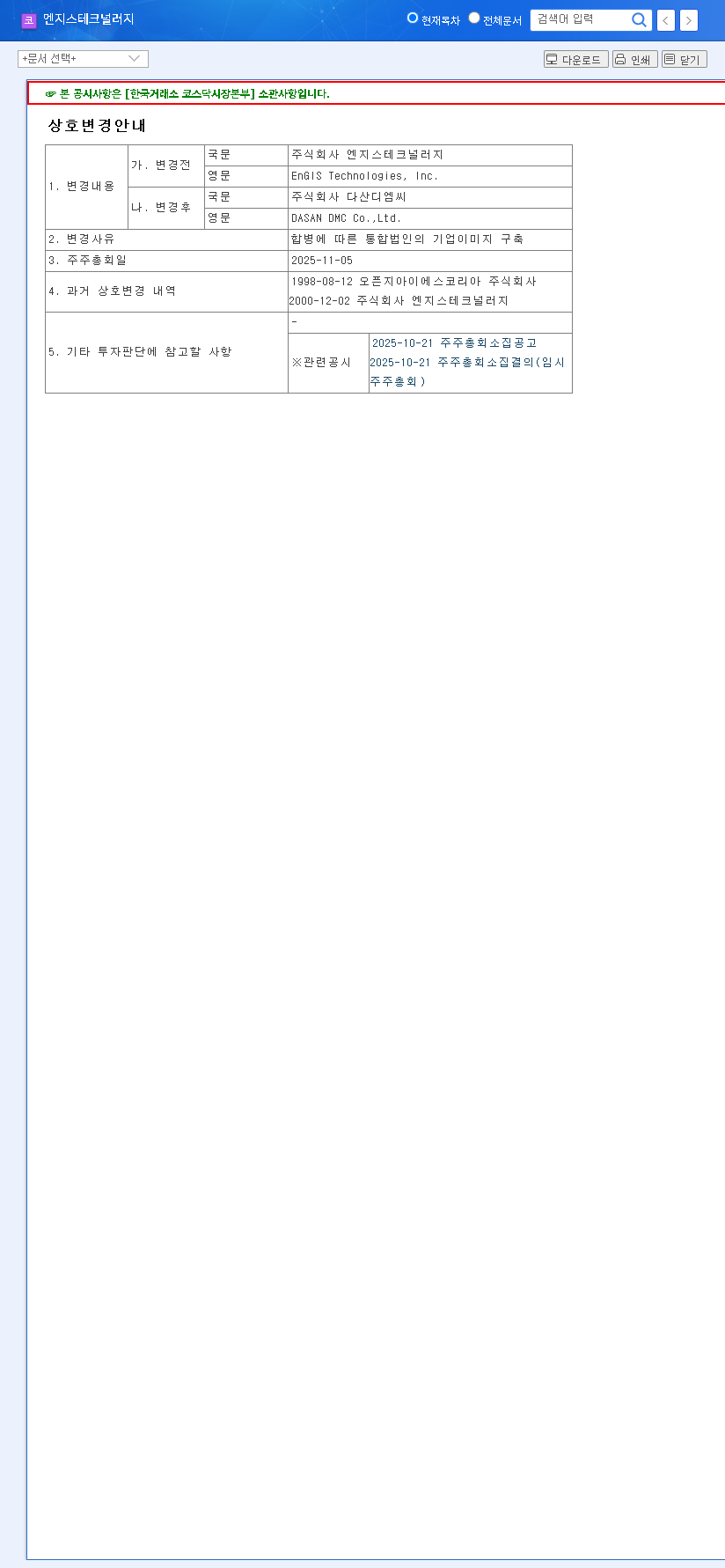

On November 12, 2025, a report on large shareholdings revealed a notable shift. The largest shareholder, DASAN Networks, along with its special related parties, adjusted its stake in EnGIS Technologies, Inc. from 79.27% down to 78.17%. While a 1.1% reduction may seem minor, the stated purpose of ‘management influence’ warrants closer inspection. This change was the result of complex transactions including over-the-counter sales and on-exchange activities by related parties. For complete transparency, you can view the Official Disclosure on the DART system. While this doesn’t signal an immediate loss of control, it does suggest strategic repositioning among stakeholders, which could have ripple effects.

In-Depth Fundamental Analysis of EnGIS Technologies

A clear EnGIS Technologies share price forecast cannot be made without a thorough review of its corporate health. The company is at a pivotal crossroads, balancing explosive growth with significant financial challenges.

The Bullish Case: DMC Acquisition and New Growth Engines

The primary driver of optimism is the recent acquisition of DMC Co., Ltd. This strategic move has catalyzed immense external growth, transforming the company’s revenue streams.

- •Explosive Revenue Growth: Post-acquisition sales soared to KRW 42.799 billion, with an operating profit of KRW 3.377 billion, establishing the automotive parts sector as a new core business.

- •Future-Facing Technology: Entry into the Human Interface Module (HIM) business provides a strong engine for future growth, tapping into the next generation of automotive technology.

- •Path to Normalization: Key steps like terminating rehabilitation procedures and securing the largest shareholder’s pledge of mandatory retention are positive signals of returning stability.

The Bearish Case: Financial Health and Profitability Hurdles

Despite the top-line growth, significant risks loom beneath the surface, primarily concerning the company’s financial structure and core profitability.

- •Soaring Debt Ratio: The DMC acquisition was costly, causing the debt ratio to surge to a concerning 91.51%. This level of leverage introduces significant financial risk. For more on this topic, review our guide to Understanding Financial Ratios for Stock Analysis.

- •Persistent Operating Losses: Both the legacy Automotive Solution and the new HIM business units continue to post operating losses, highlighting an urgent need for widespread profitability improvements.

- •Macroeconomic Vulnerability: High debt makes the company susceptible to external shocks. Future interest rate hikes, as discussed by global financial authorities like the Federal Reserve, could substantially increase interest burdens and strain cash flow.

EnGIS Technologies presents a classic high-risk, high-reward scenario. The success of its share price post-resumption hinges on management’s ability to translate acquisition-led growth into sustainable profitability while carefully managing its debt.

Investor Strategy and Recommendations

Given the complex situation, a prudent investment strategy is essential. The initial market reaction upon trading resumption will be a key barometer of investor sentiment. We recommend focusing on the following areas:

- •Monitor Trading Resumption: Closely observe trading volumes and price action on and after July 7, 2025, to gauge the market’s initial assessment of the EnGIS Technologies stock.

- •Track Fundamental Improvements: Scrutinize quarterly reports for evidence of synergy with DMC, improving profit margins, and a tangible reduction in the overall debt ratio.

- •Analyze Shareholder Actions: Keep an eye on any further reports from DASAN Networks. The rationale behind future stake changes will provide valuable insight into their long-term strategy.

- •Demand Transparency: Pay attention to the company’s investor relations activities and information disclosures. Proactive communication is vital for rebuilding trust after a delisting scare.

Frequently Asked Questions (FAQ)

Q1: When will EnGIS Technologies’ stock (208860) resume trading?

Stock trading for EnGIS Technologies, which was suspended on April 7, 2021, is officially scheduled to resume on July 7, 2025. This event will be a critical test of market confidence.

Q2: What is the biggest positive factor for the EnGIS Technologies share price forecast?

The most significant positive factor is the external growth from the acquisition of DMC Co., Ltd. This has made the automotive parts sector a major revenue contributor and signals a bold strategic shift for the company.

Q3: What is the primary risk facing EnGIS Technologies?

The primary risk is its precarious financial health, highlighted by a debt ratio of 91.51% following the acquisition. This high leverage, combined with ongoing operating losses in key business units, makes the company vulnerable to economic downturns and rising interest rates.