![(069260) TKG Huchems Co.,Ltd. Investment Analysis [2025]: Navigating the H1 Slowdown & IR Event](https://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/07103033/069260-1.png)

For investors tracking the chemical sector, TKG Huchems Co.,Ltd. presents a complex but compelling case. Amidst challenging global economic currents, the company has reported a short-term performance dip. However, strategic investments in future growth and an upcoming Investor Relations (IR) event signal a potentially pivotal moment. This comprehensive analysis will explore the factors behind the H1 2025 slowdown, evaluate the company’s long-term strategy, and provide a framework for making an informed TKG Huchems investment decision.

We will dissect the financials, unpack the market pressures, and look ahead to what the critical Q3 IR event could reveal about the trajectory of the TKG Huchems stock.

Deconstructing the H1 2025 Performance Slowdown

The first half of 2025 proved to be a challenging period for TKG Huchems Co.,Ltd., reversing the positive recovery trend seen in the previous year. The company, a key manufacturer of polyurethane intermediates (NT series) and nitric acid-based chemical products (NA series), reported a noticeable downturn in key financial metrics.

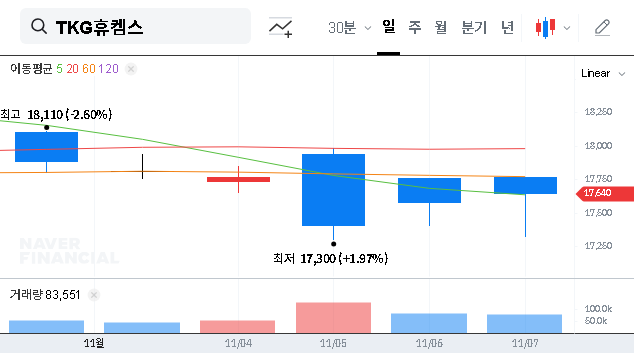

Specifically, revenue fell by 3.6% year-on-year to KRW 559.5 billion, while operating profit experienced a more significant decline of 32.6%, settling at KRW 34.6 billion. This performance data is corroborated by the company’s official filing with the Financial Supervisory Service (Source: Official Disclosure). These figures have understandably raised questions among investors about the company’s immediate prospects.

Core Factors Driving the Downturn

The performance of TKG Huchems Co.,Ltd. was not impacted by a single issue, but rather a confluence of macroeconomic headwinds and market volatility.

1. Global Economic Pressures

A widespread slowdown in global economic activity, as highlighted in recent reports from leading financial institutions, directly led to diminished demand from key industrial customers in sectors like automotive and construction, which are major consumers of polyurethane products. This was compounded by:

- •Cost Volatility: Sharp fluctuations in international oil prices, raw material costs, and shipping logistics placed significant upward pressure on the cost of goods sold, eroding profit margins.

- •Currency Fluctuations: An unstable exchange rate environment (with KRW/USD near 1,300) introduced complexity into pricing for both exports and imports, making profit forecasting more difficult.

2. A Silver Lining: Financial Stability & Future Investments

Despite the short-term profit headwinds, the company’s balance sheet remains a source of strength. TKG Huchems Co.,Ltd. has demonstrated prudent financial management, successfully reducing total liabilities while steadily growing its total equity. This foundation of financial health is crucial for navigating market turbulence. Furthermore, a consistent commitment to shareholder-friendly policies, including dividends and treasury stock holdings, continues to appeal to long-term value investors.

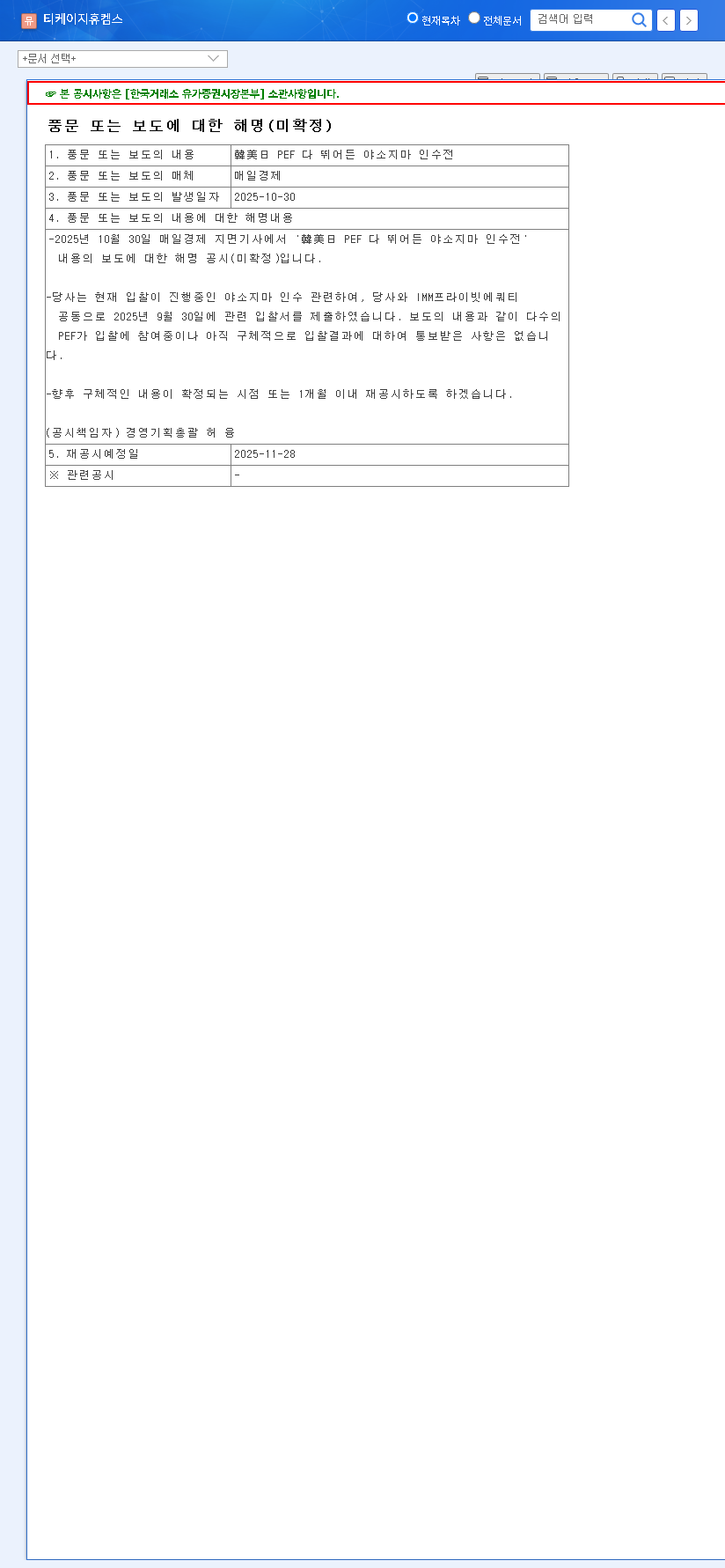

Even in a downturn, the company’s focus has not wavered from securing future growth. Strategic capital expenditures are proceeding as planned, signaling confidence in a long-term recovery and market leadership.

Key initiatives include capacity expansions for nitric acid and MNB plants, alongside the acquisition of new technology certification for P-PDA manufacturing—a material used in high-strength fibers—positioning the company to capture future demand in advanced materials. These are the kinds of forward-looking moves that underpin a positive long-term TKG Huchems investment thesis.

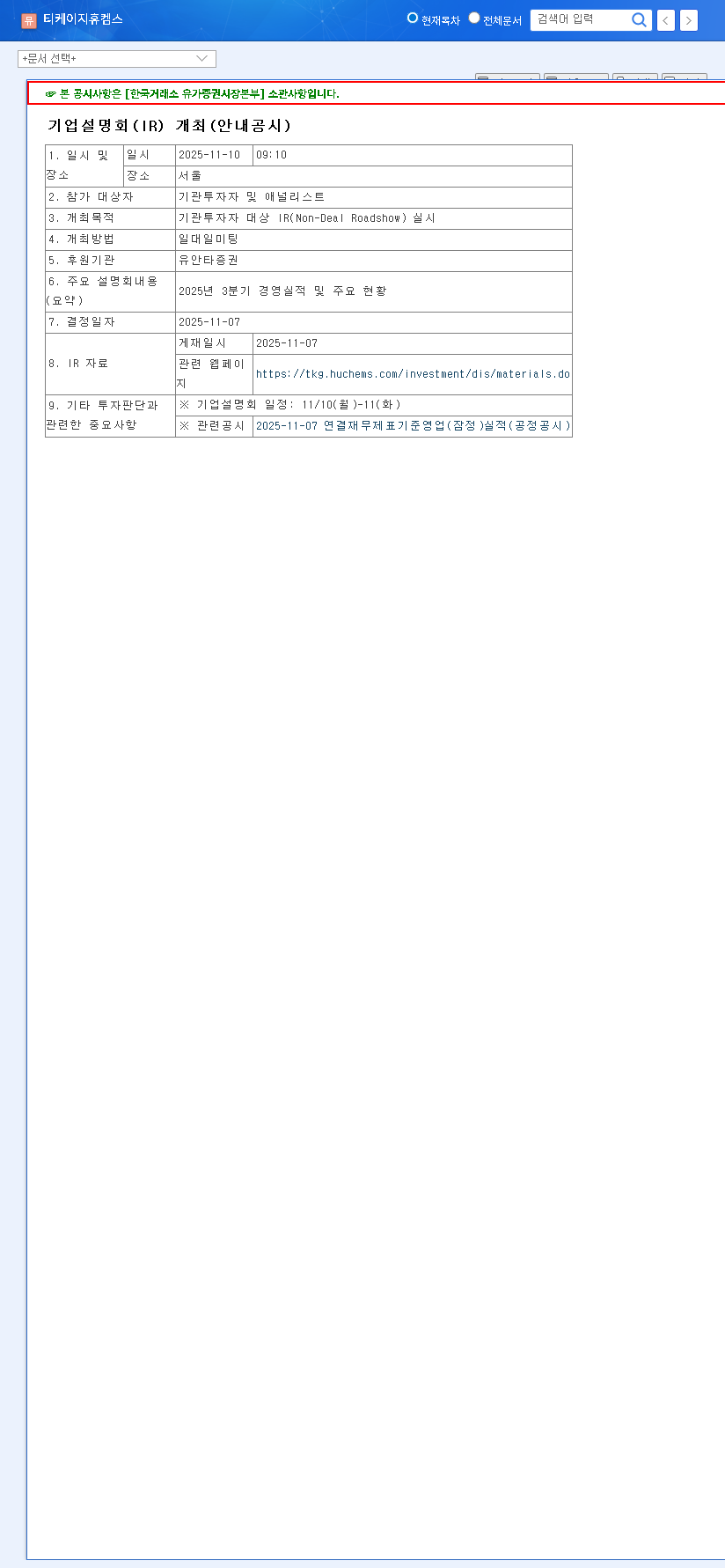

The Upcoming IR Event: A Turning Point for TKG Huchems Stock?

The scheduled TKG Huchems IR event for institutional investors is more than a standard earnings call; it’s a critical opportunity for management to reshape the narrative. The event’s success will hinge on its ability to restore confidence and provide a clear, credible vision for the future.

Key Questions the IR Event Must Address:

- •Q3 Performance & Outlook: What are the initial signals for Q3, and what is the forecast for the remainder of the fiscal year?

- •Risk Management Strategy: What specific measures are being implemented to mitigate the impact of raw material price and currency volatility?

- •CapEx ROI Timeline: When can investors expect to see tangible financial contributions from the nitric acid, MNB, and P-PDA investments?

- •Path to Profitability Recovery: What is the strategic plan to return the core business to its previous levels of profitability?

A confident and transparent presentation could lead to a re-evaluation of the company’s value and attract new institutional buying interest. Conversely, an evasive or uncertain tone could exacerbate investor concerns.

Investment Strategy & Outlook

A prudent approach to a TKG Huchems investment requires a dual focus on short-term catalysts and long-term fundamentals. For those looking for broader market context, you can learn more about investing in the chemical sector on our blog.

Short-Term Strategy (3-6 Months)

The IR event is the primary catalyst. If management provides a positive outlook with credible strategies, a short-term rebound in the stock price is plausible. If the outlook remains cautious, a wait-and-see approach may be warranted until macroeconomic indicators improve.

Mid-to-Long-Term Strategy (1-3 Years)

The focus here shifts to the execution of growth projects. Investors should monitor the progress of plant expansions and the successful commercialization of new technologies. The recovery of profitability in the core NT and NA series businesses is paramount for a sustained upward trend in the TKG Huchems stock price. The company’s ability to manage its balance sheet and continue shareholder-friendly policies will also be key indicators of long-term value creation.

Conclusion: A Balanced View

TKG Huchems Co.,Ltd. is at a crossroads. While current performance is impacted by cyclical and macroeconomic factors, its strong financial health and strategic investments in future growth drivers provide a solid foundation for recovery. The upcoming IR event will be a critical litmus test for management’s ability to navigate these challenges and articulate a compelling vision. For discerning investors, this period of uncertainty could represent an opportunity, provided they carefully analyze the forthcoming information and maintain a long-term perspective.

![(069260) TKG Huchems Co.,Ltd. Investment Analysis [2025]: Navigating the H1 Slowdown & IR Event 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/07103036/069260_%EA%B3%B5%EC%8B%9C-1.png)