In the highly competitive and volatile semiconductor market, fabless company FADU INC. (KRX: 440110) has just announced a pivotal development that demands a closer look from investors. This comprehensive FADU INC. stock analysis explores the implications of its newly secured KRW 14.5 billion contract for its innovative FADU SSD controller technology. The deal validates the company’s tech but also highlights existing financial challenges, creating a complex picture for its future.

While this contract represents a significant step forward, potential investors must weigh the positive catalysts against lingering risks like inventory burdens and profitability hurdles. This report provides an in-depth breakdown of the opportunities and threats to help you make an informed decision about FADU INC. stock.

Breaking Down the Landmark Deal

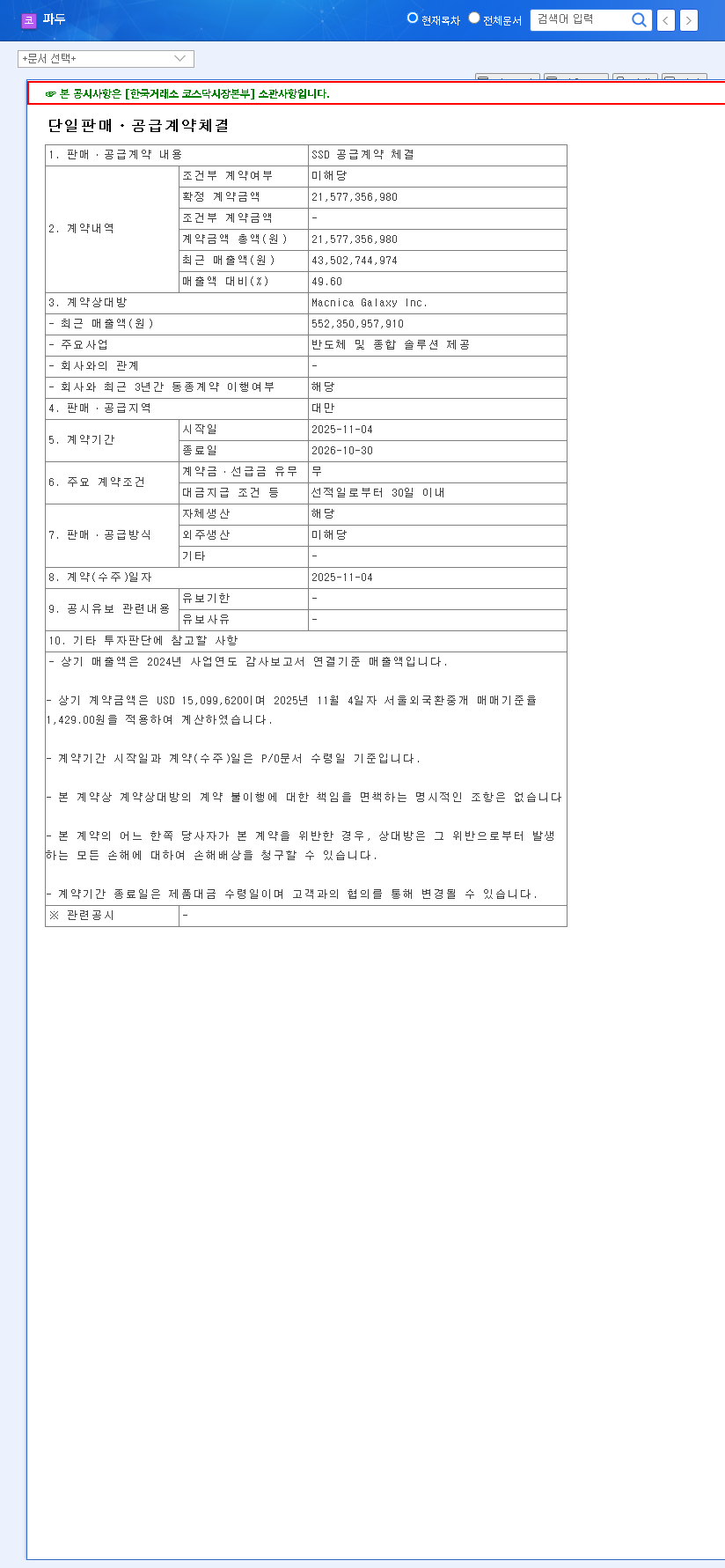

On November 10, 2025, FADU INC. officially disclosed a substantial single sales and supply contract for its enterprise-grade SSD controllers. According to the Official Disclosure, the deal is with a major overseas NAND Flash Memory manufacturer and carries a significant value of KRW 14.5 billion (approx. USD 10.5 million). This figure is not trivial; it represents a staggering 33.28% of FADU’s recent annual revenue. The contract term ensures a direct and positive impact on the company’s top-line revenue through 2025 and into the first half of 2026.

The Bull Case: Catalysts for FADU’s Growth

This contract is far more than just a revenue boost; it sends powerful signals to the market and sets the stage for potential long-term growth. Here are the primary positive drivers for FADU INC. stock.

Validation of Technological Leadership

Securing a deal of this magnitude with a major global player is a powerful endorsement of FADU’s technological prowess. It proves that its high-performance enterprise FADU SSD controller solutions are not only innovative but also commercially viable and competitive on the world stage. This validation can act as a bridgehead, making it easier to attract new high-profile customers and deepen relationships with existing clients.

Financial Health and Revenue Acceleration

The direct revenue contribution is a clear positive. After a difficult period where revenue fell sharply in 2023, this contract solidifies the company’s recovery trajectory. Beyond the top line, the deal is expected to improve financial health by:

- •Improving Profitability: Enterprise SSD controllers are high-margin products, which should positively impact the bottom line.

- •Reducing Inventory: The new demand will help clear existing inventory, which has been a significant financial burden.

- •Strengthening Cash Flow: Improved sales and reduced inventory carrying costs are expected to enhance cash flow and reduce borrowing needs.

This contract is a critical turning point, validating FADU’s technology and providing a clear path to revenue growth. The key for long-term success will be translating this momentum into sustainable profitability.

The Bear Case: Headwinds and Risks for FADU Investors

Despite the positive news, a thorough FADU investment analysis must acknowledge the significant challenges that remain. These risks could temper the stock’s performance if not managed effectively.

Persistent Financial Burdens

FADU’s balance sheet carries notable burdens from its recent past. The inventory of KRW 31.3 billion and associated valuation losses are significant hurdles. Furthermore, a net loss of KRW 91.5 billion in 2024 and high R&D spending (151.93% of revenue) highlight the urgent need for stringent cost controls and a clear strategy to convert revenue into profit. For more on sector trends, investors often consult resources like the Semiconductor Industry Association reports.

Intense Competition and Market Dynamics

The global semiconductor market for SSD controllers is fiercely competitive. FADU faces pressure from established giants and nimble startups alike. Rapid technological shifts mean that today’s cutting-edge product can quickly become obsolete. Investors must monitor the competitive landscape and FADU’s ability to maintain its technological edge. If you’re new to the sector, consider reading our guide to investing in semiconductor stocks.

Investment Thesis & Strategic Outlook

The KRW 14.5 billion contract is a clear positive catalyst for FADU INC. stock in the short term, likely boosting investor sentiment. However, the mid-to-long-term outlook hinges on the company’s ability to execute. Key performance indicators to watch include:

- •Profitability Margins: Can the high-value contract translate into improved gross and net profit margins?

- •Inventory Management: How quickly can the company reduce its inventory overhang and associated costs?

- •Follow-on Deals: Can FADU leverage this success to secure more contracts and diversify its customer base?

Recommendation: A cautiously optimistic stance is warranted. Investors should view this as a significant positive development but must continue to monitor FADU’s financial health and execution closely. The stock holds high potential for growth but also comes with considerable volatility until a clear trend of sustainable profitability is established.

Frequently Asked Questions (FAQ)

What is the nature of FADU INC.’s recent KRW 14.5 billion contract?

FADU INC. signed a sales and supply contract worth KRW 14.5 billion (approx. USD 10.5 million) with a major overseas NAND Flash Memory manufacturer for its enterprise SSD controllers. This deal represents about 33.28% of FADU’s 2024 revenue.

How will this contract impact FADU’s financials?

The contract will directly boost revenue in 2025 and 2026. Because it involves high-value enterprise products, it is also expected to improve profitability. Additionally, it should help reduce inventory levels and strengthen the company’s overall cash flow.

What are the main risks for FADU INC. stock investors?

Key risks include the company’s existing high inventory levels, a history of net losses, and the intense competition within the global SSD controller market. Investors should monitor FADU’s progress in achieving sustainable profitability.