The future of Icure Pharmaceutical Incorporation hangs in the balance following a critical decision by the Corporate Review Committee. On November 12, 2025, the company announced it had been granted an 8-month Icure Pharmaceutical improvement period, a formal warning that places its continued stock market listing in serious jeopardy. This development signals profound operational and financial distress, forcing investors to confront the very real possibility of a delisting event.

This in-depth analysis unpacks the severe challenges facing Icure Pharmaceutical, explores the stringent requirements of the improvement period, and outlines what this means for the company, its stock, and its stakeholders. For investors, this is a crucial time for diligence and understanding the high-stakes road ahead.

Understanding the Corporate Review Committee’s Mandate

The decision, officially announced on November 12, 2025, grants Icure until July 12, 2026, to demonstrate significant and sustainable improvements. According to the Official Disclosure (DART Report), Icure must submit a comprehensive implementation report and an expert verification within 15 days of this deadline. Following submission, the committee will make a final ruling on whether to delist the company within 20 business days. This tight timeline places immense pressure on management to execute a dramatic turnaround.

An improvement period is not a lifeline; it is a final warning. The risk of delisting is now the primary factor that should govern any investment decision related to Icure Pharmaceutical stock.

In-Depth Analysis: The Roots of Icure’s Crisis

The committee’s decision was not made in a vacuum. It is the culmination of prolonged financial deterioration and a failure to achieve commercial viability despite promising technology. Here’s a closer look at the core issues.

1. Alarming Financial Deterioration

The company’s financial statements paint a grim picture. As of December 2024, Icure reported revenues of only KRW 33.4 billion against a staggering operating loss of KRW -59.4 billion. This massive deficit, coupled with a net loss of KRW -55.5 billion, highlights a business model that is hemorrhaging cash. Further red flags include:

- •Capital Erosion: An extremely low equity ratio of 17.18% indicates that the company’s asset base is heavily financed by debt, and its shareholder equity has been severely depleted by persistent losses.

- •Negative Shareholder Value: The Earnings Per Share (EPS) of -1,094 KRW for 2024 confirms that the company is destroying value for its shareholders, not creating it.

- •Unsustainable Operations: Negative operating and net profit margins show that the core business is fundamentally unprofitable at its current scale and cost structure.

2. The Promise vs. Reality of its Business

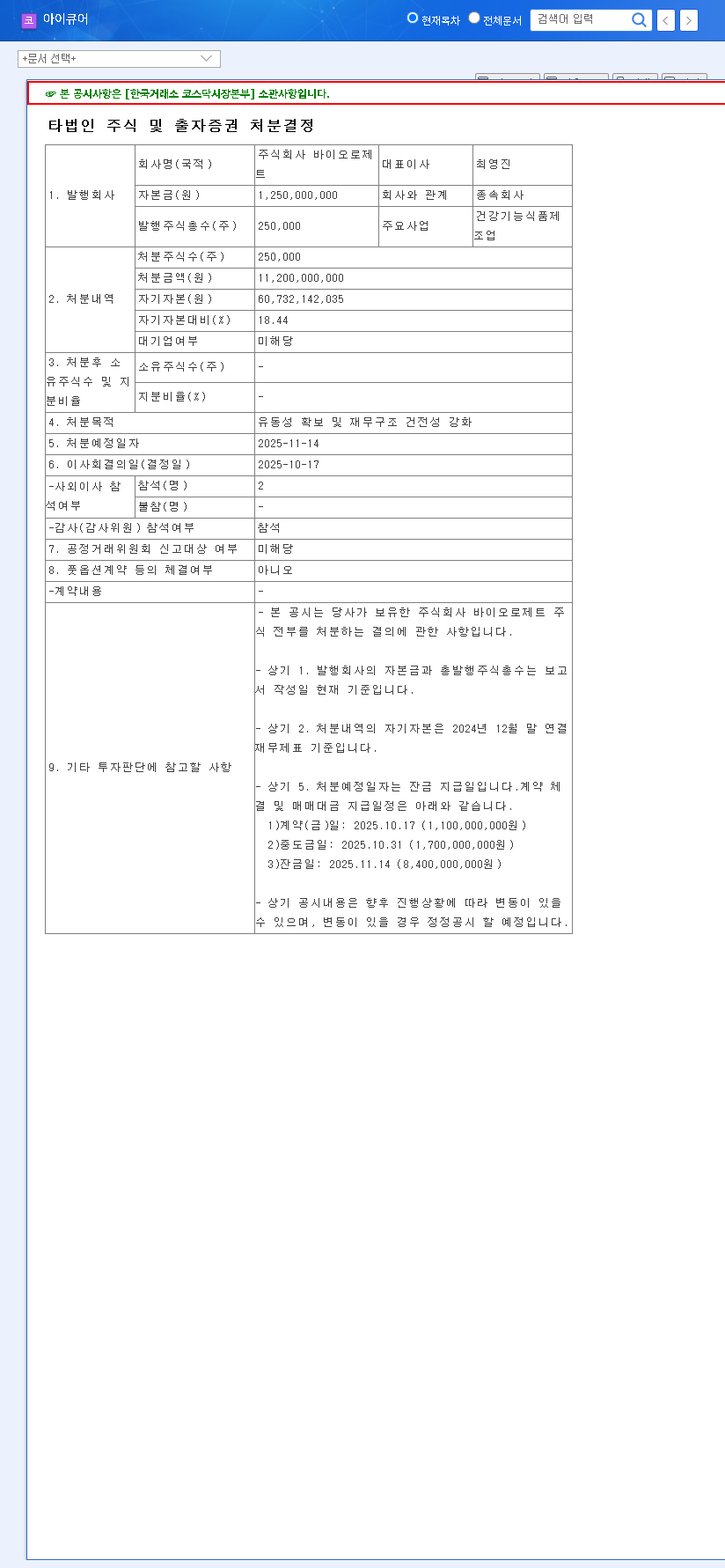

Icure operates in the promising pharmaceutical and cosmetics sectors, built upon its proprietary Transdermal Drug Delivery System (TDDS) technology. This technology, which allows drugs to be administered through the skin via patches, has shown potential, particularly with its overseas licensing agreements for a Donepezil patch for Alzheimer’s treatment. However, the high costs of R&D, intense market competition, and regulatory hurdles have prevented this potential from translating into profitability. For more on market dynamics, expert analysis from sources like Bloomberg can provide wider industry context. The current financial crisis now overshadows any technological promise the company holds.

What’s Next? Investor Strategy During the Improvement Period

The Icure Pharmaceutical improvement period triggers extreme uncertainty. The stock price will likely experience severe volatility, driven by panic selling and speculative buying. For current and prospective investors, a cautious and informed approach is paramount.

Key Actions Icure Must Take

To survive, Icure’s management must implement a drastic and convincing turnaround plan. This will likely involve a combination of painful but necessary measures:

- •Capital Injection: Securing significant new funding through strategic investors or rights offerings is non-negotiable.

- •Aggressive Restructuring: This could include selling non-core assets, streamlining operations, and significant cost-cutting initiatives.

- •Enhanced Governance: Restoring market trust requires absolute transparency in communication and corporate governance.

How Investors Should Respond

Given the heightened Icure Pharmaceutical delisting risk, investors should exercise extreme caution. This situation is not suitable for those with a low risk tolerance. It is essential to monitor the company’s announcements and progress against its improvement plan. For a broader perspective on managing high-risk assets, consider reading articles on diversification strategies for volatile portfolios. The feasibility and execution of the company’s turnaround plan will be the sole determinant of its future. Until a clear, credible, and funded path to profitability is demonstrated, the investment case for Icure remains exceptionally speculative and high-risk.