As the semiconductor industry evolves at a breakneck pace, investors are keenly watching key material suppliers like TOKAI CARBON KOREA CO., LTD (TCK, 064760). With its upcoming Investor Relations (IR) conference on November 17, 2025, the market is poised to gain critical insights into the company’s future. This event is more than a routine update; it’s a pivotal moment that could define the TCK investment strategy for the coming years. This comprehensive analysis will delve into TCK’s fundamentals, the explosive Solid SiC growth trajectory, and what the IR could mean for TCK’s stock valuation, providing a clear roadmap for investors.

Unpacking the 2025 TCK Investor Relations Event

The primary goal of TCK’s IR event is to foster transparency and bolster stakeholder confidence. Management is expected to provide a detailed overview of the company’s business status, field critical questions in a Q&A session, and outline future strategies. The spotlight will undoubtedly be on its core business segments, particularly the performance metrics and forward-looking plans that will shape the company’s path through the current semiconductor super-cycle. For any serious TCK stock analysis, this event is mandatory viewing.

This IR is a crucial litmus test. It will reveal whether TOKAI CARBON KOREA can not only meet but exceed lofty market expectations, potentially unlocking significant new growth momentum for its stock.

The Bedrock of Growth: TCK’s Robust Fundamentals

A successful TCK investment strategy must be grounded in its powerful fundamentals. The company’s strength is not just a story of market opportunity but one of financial prudence, technological leadership, and strategic foresight.

Stellar Financial Health & Performance

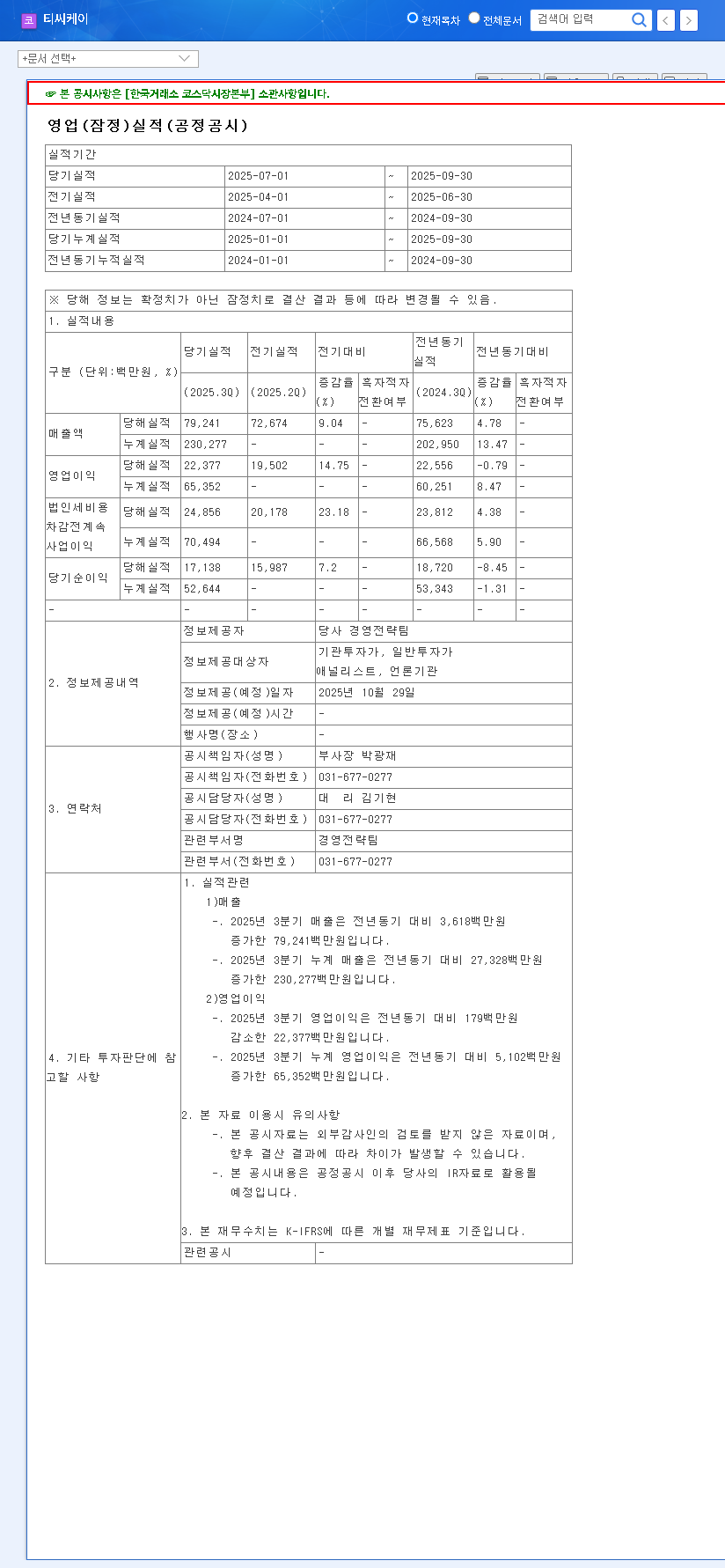

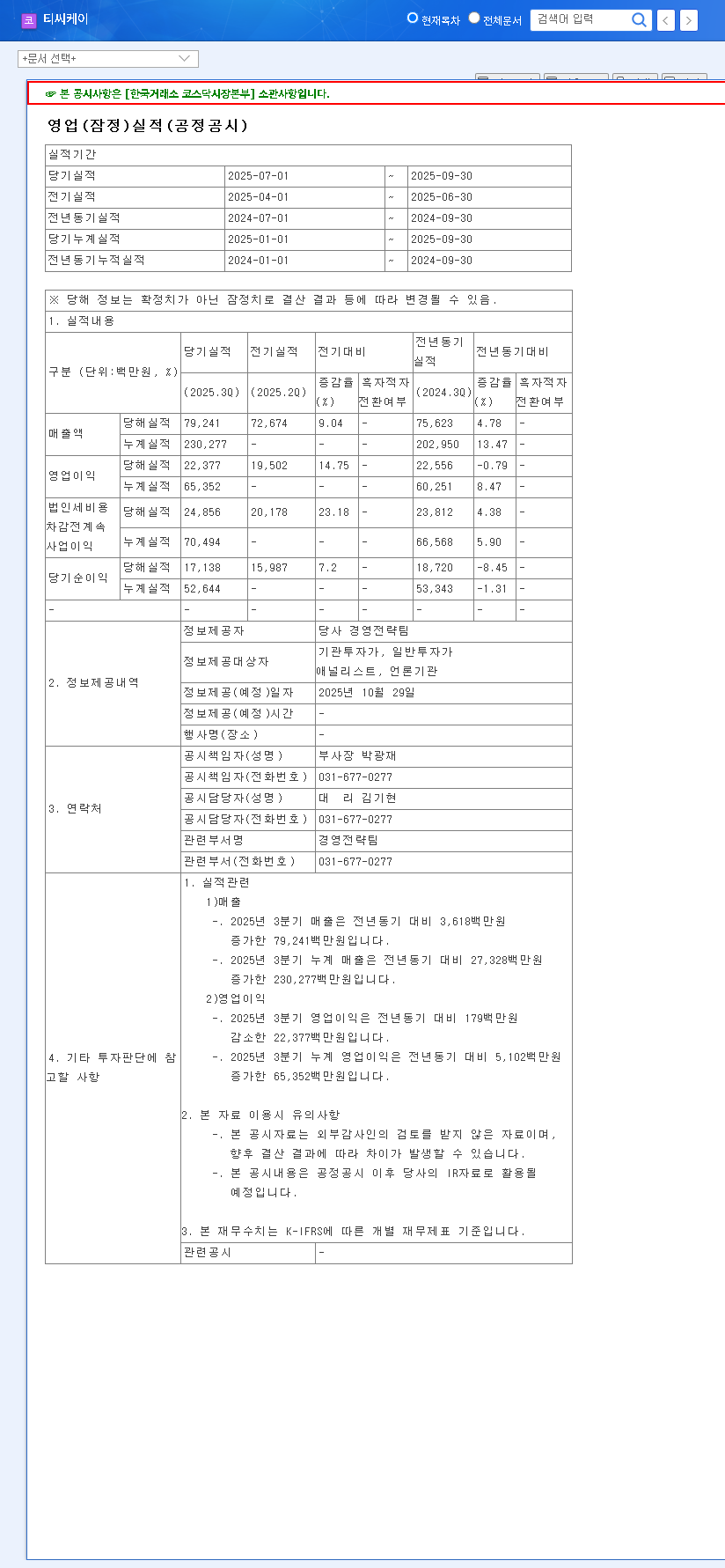

TCK’s financial foundation is remarkably solid. The accumulated sales for Q3 2025 reached 230.277 billion KRW, a significant 13.4% year-on-year increase, with operating profit growing 8.4% to 65.352 billion KRW. These figures, available in the company’s Official Disclosure (Source), highlight the company’s consistent performance. Key financial indicators include:

- •Exceptional Financial Stability: With a debt-to-equity ratio of just 8.04%, TCK showcases incredible resilience against market volatility and economic headwinds.

- •Healthy Profitability: While the Return on Equity (ROE) of 10.4% is healthy, it has seen a slight dip. This is attributed to strategic increases in total equity for future investments rather than a decline in operational efficiency.

- •Future-Focused Cash Flow: A temporary decrease in operating cash flow is linked to increased investment activities, signaling a strong commitment to fueling long-term growth.

Unrivaled Dominance in the Solid SiC Market

The engine of TOKAI CARBON KOREA is its Solid SiC (Silicon Carbide) division, which accounts for a staggering 83.8% of total sales. The demand for Solid SiC rings and components is exploding, driven by the semiconductor industry’s push towards finer processing nodes and 3D NAND architecture. TCK’s localization of high-purity graphite and SiC coating technologies gives it a near-insurmountable competitive advantage. The company’s consistent R&D investment ensures it stays ahead, developing next-generation products like 12-inch SiC Wafers to capture future market share.

Analyzing the IR’s Potential Impact on TCK Stock (064760)

The IR event can act as a powerful catalyst for TCK’s stock price. A clear, confident presentation of its growth strategy can significantly boost investor sentiment. Conversely, any ambiguity or failure to address market concerns could introduce volatility. Investors should weigh both the potential upsides and risks.

The Bull Case: Positive Catalysts

- •Enhanced Transparency: Detailed plans for Solid SiC capacity expansion and new investments can solidify investor confidence and lead to upward price revisions.

- •Positive Market Communication: Direct engagement helps management align with investor expectations, reinforcing the company’s long-term vision. Read more about the semiconductor industry’s growth trends in our related article.

The Bear Case: Potential Risks and Volatility

- •Expectation Mismatch: If the IR fails to deliver groundbreaking news or presents a conservative outlook, it could trigger a short-term sell-off from disappointed investors.

- •Macroeconomic Headwinds: The company’s presentation will be viewed through the lens of the current global economic climate, as detailed by sources like Bloomberg Economics. Unfavorable shifts in exchange rates or interest rates could overshadow positive company news.

A Comprehensive TCK Investment Strategy

Given the analysis, a prudent TCK investment strategy should be focused on the mid-to-long term. While short-term volatility around the IR is possible, the company’s core strengths—its dominance in the high-growth Solid SiC market, technological leadership, and robust financial health—point towards a positive long-term trajectory. Investors should monitor the IR for confirmation of capacity expansion plans and management’s outlook on market demand. Any price dips resulting from short-term market noise could present attractive entry points for those with a long-term horizon.

Frequently Asked Questions (FAQ)

1. What are the core growth drivers for TOKAI CARBON KOREA?

TCK’s primary growth driver is its Solid SiC business, which benefits from rising demand in advanced semiconductor manufacturing. This is supported by its strong technological leadership and ongoing R&D investments.

2. What are the main risks for investors considering a TCK investment strategy?

Key risks include the semiconductor industry’s cyclical nature, potential for increased competition, and macroeconomic factors like exchange rate volatility. Short-term risk also exists if the upcoming IR fails to meet high market expectations.

3. What is the long-term stock outlook based on this TCK stock analysis?

The mid-to-long-term outlook is positive. The sustained growth of the Solid SiC market, combined with TCK’s dominant position and planned capacity expansion, strongly supports a favorable stock price trend over time, despite potential short-term volatility.