The latest DoubleUGames earnings report for Q3 2025 presents a complex picture for investors. While the social casino giant surpassed market expectations on revenue and operating profit, a notable miss on net profit has raised important questions. This detailed DoubleUGames financial analysis will unpack the headline figures, explore the underlying strengths and risks, and provide a clear action plan for anyone monitoring DoubleUGames stock.

We’ll examine the stability of its core business, the impact of recent M&A activities, and the external pressures like foreign exchange volatility that are shaping its financial future.

DoubleUGames Q3 2025 Earnings: The Official Numbers

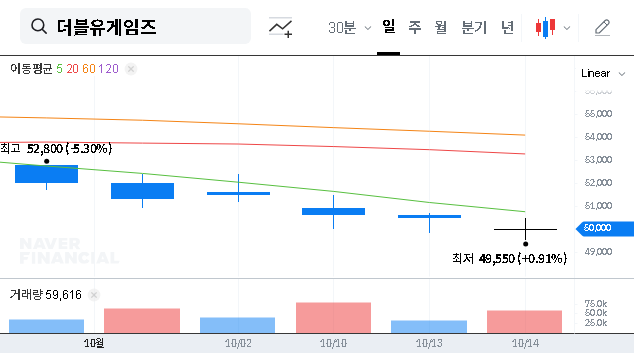

On November 11, 2025, DoubleUGames released its preliminary consolidated financial results for the third quarter, revealing a mixed but generally solid operational performance. Here are the key metrics compared to market consensus:

- •Revenue: KRW 186.2 billion (1% above estimate of KRW 184.7 billion)

- •Operating Profit: KRW 59.2 billion (2% above estimate of KRW 58.3 billion)

- •Net Profit: KRW 46.1 billion (4% below estimate of KRW 47.9 billion)

These figures were sourced from the company’s official filing. You can view the full details in the Official Disclosure (DART Report). While the top-line and operational beats signal strong core business health, the net profit shortfall requires a deeper look into the company’s financial structure and external pressures.

Fundamental Analysis: Growth Strategy and Underlying Risks

DoubleUGames is executing a two-pronged strategy: fortifying its cash-cow social casino business while aggressively pursuing mergers and acquisitions (M&A) to fuel new growth. This creates both exciting opportunities and notable risks for investors.

Key Strengths and Positive Factors

- •Dominant Market Position: Maintaining a Top 5 position in the global social casino market provides a stable revenue base and significant cash flow, powered by sophisticated in-house marketing and big data analytics.

- •Strategic M&A Growth: The acquisition of SuprNation AB is already bearing fruit, contributing over 12% of revenue and marking a successful entry into the iGaming sector. The purchase of Paxie Games further diversifies the company’s portfolio into casual gaming.

- •Shareholder-Friendly Policies: The company is actively working to enhance shareholder value through treasury stock buybacks and planned share cancellations, which can increase earnings per share.

- •Solid Financial Health: With strong credit ratings (A2/A0) and a healthy cash reserve of KRW 561.7 billion, the company is well-positioned to weather economic shifts and fund future growth.

Challenges and Risk Factors to Monitor

The primary drag on the recent DoubleUGames earnings came from non-operational factors: amortization of intangible assets from recent acquisitions and foreign exchange losses.

- •Intangible Asset Amortization: M&A deals result in significant ‘intangible assets’ like goodwill on the balance sheet. These must be expensed over time (amortized), which reduces net profit on paper without affecting cash flow. This will continue to be a headwind.

- •Foreign Exchange (FX) Volatility: With a large portion of revenue in USD and EUR, a strengthening of those currencies against the KRW can lead to significant translation losses, impacting the bottom line as seen in Q3.

- •New Business Integration: The success of the iGaming and casual game ventures is not yet guaranteed. Investors must monitor their performance to ensure they contribute meaningfully to long-term growth and justify their acquisition costs.

Investor Action Plan: Navigating the Future of DUG Stock

Given the balance of strong operational performance and specific, identifiable headwinds, a ‘Neutral’ investment stance is warranted. Long-term success depends on the company’s ability to manage these factors effectively. Here’s what to watch for in upcoming DoubleUGames earnings calls and reports.

Key Metrics and Developments to Monitor

- •Growth from New Segments: Look for consistent, quarter-over-quarter revenue growth from the iGaming (SuprNation) and casual games (Paxie Games) divisions. Is their contribution to the consolidated total increasing? For market context, see this analysis from Bloomberg on the gaming sector.

- •Profit Margin Stability: Monitor operating and net profit margins. While amortization will pressure net margins, a stable or improving operating margin would confirm the underlying health of the business.

- •Execution of Shareholder Returns: Track the progress of the announced treasury stock buyback and cancellation. Concrete actions here are a direct return of value to shareholders and signal management’s confidence.

- •Management’s Commentary on FX: Listen for any strategies or hedging policies the company plans to implement to mitigate the impact of currency fluctuations on future earnings.

Conclusion: A Stable Core with Manageable Headwinds

DoubleUGames’ Q3 2025 earnings demonstrate a company with a robust and competitive core business capable of beating operational estimates. The challenges it faces—primarily from M&A-related accounting and FX market volatility—are significant but not insurmountable. For investors, the path forward requires diligent monitoring of the company’s new ventures and its effectiveness in managing costs. The current DoubleUGames stock valuation appears to balance this potential against the known risks, supporting a patient, long-term perspective.