The outlook for WITHTECH stock has entered a pivotal phase following a major contract announcement. WITHTECH, Inc., a key player in the semiconductor ecosystem, recently secured a substantial ₩3.6 billion supply deal with industry giant SK hynix. While this news injects significant optimism, it arrives amidst underlying profitability concerns. This comprehensive analysis will dissect the contract’s implications, evaluate the company’s fundamental health, and present a clear investment strategy for investors considering a position in WITHTECH Inc.

Can this landmark deal be the catalyst that resolves persistent profitability issues and propels the company into a new era of sustainable growth? We will explore the opportunities and risks to provide a balanced view on making a wise WITHTECH investment.

The Landmark SK hynix Deal: A Closer Look

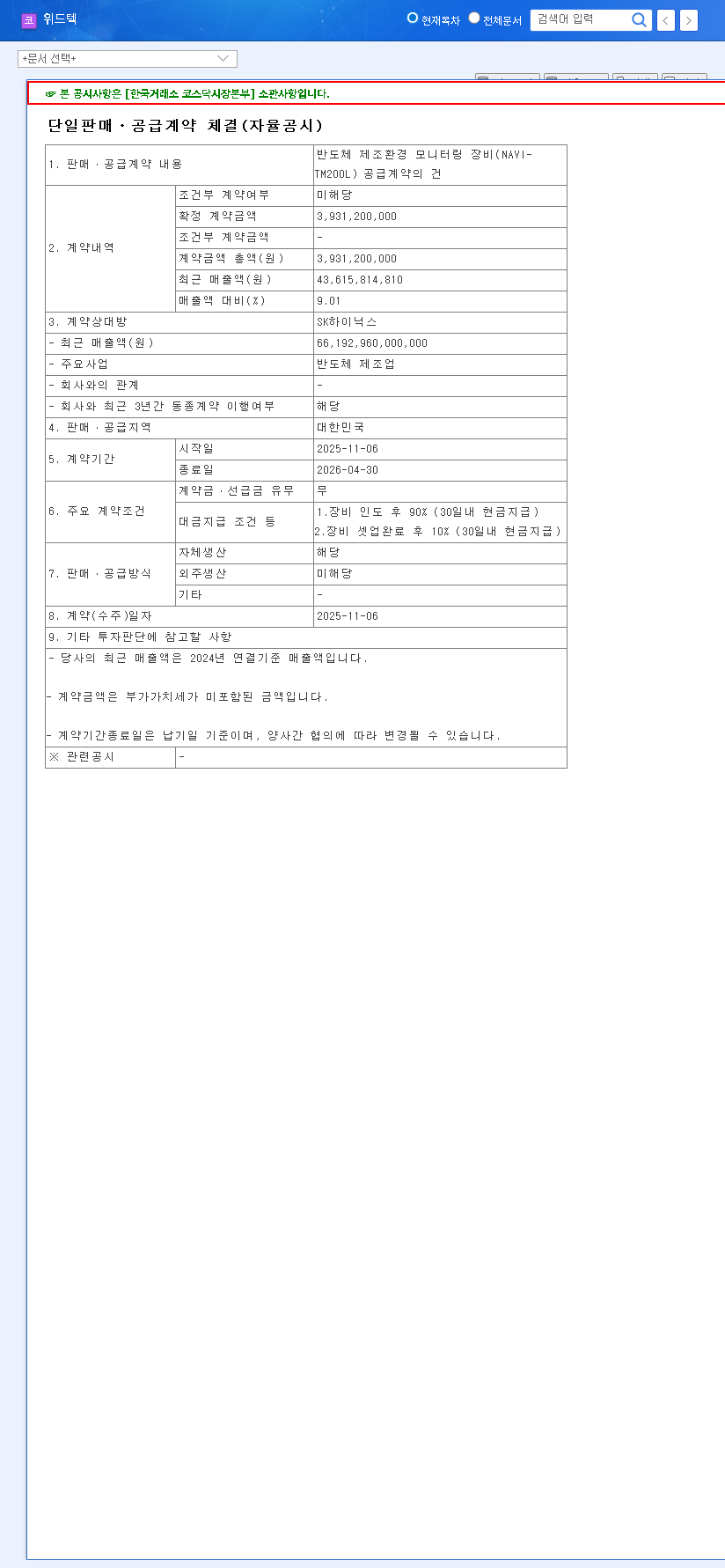

On November 10, 2025, WITHTECH, Inc. announced a significant supply contract with SK hynix, one of the world’s leading memory chip makers. The deal, valued at ₩3.6 billion, is for advanced semiconductor manufacturing environment monitoring equipment, including their flagship NAVI-TM200L model. According to the Official Disclosure, this contract represents a substantial 8.24% of the company’s projected 2025 revenue. The contract period extends from November 7, 2025, to May 31, 2026, ensuring a solid revenue stream for the next two quarters.

This SK hynix deal is more than just a financial boost; it’s a powerful endorsement of WITHTECH’s technological capabilities, solidifying its position as a critical supplier within the highly competitive semiconductor industry.

Fundamental Analysis: Growth with Underlying Challenges

A review of WITHTECH’s H1 2025 semi-annual report reveals a complex picture. The company achieved an impressive 16% year-on-year revenue growth, a clear sign of market demand. However, this top-line growth was overshadowed by an operating loss of ₩590 million, highlighting a critical decline in profitability. This was attributed to a rise in the cost of goods sold and increased SG&A expenses.

The AMC Segment: WITHTECH’s Growth Engine

The primary driver behind the revenue surge was the ‘Atmospheric Molecular Contamination’ (AMC) segment, which saw an explosive 393% increase. AMC control is vital in modern semiconductor fabrication, where even parts-per-billion level contaminants can ruin entire batches of wafers. WITHTECH’s expertise in high-sensitivity measurement and contamination control technology places it at the forefront of this crucial niche, a fact validated by the recent SK hynix deal.

Core Strengths and Weaknesses

- •Strengths: Leading-edge precision measurement technology, a robust portfolio of patents, a deep pool of engineering talent, and promising diversification into new markets like nuclear power plant decommissioning waste analysis.

- •Weaknesses: Deteriorating operating and net profit margins, negative ROE and EPS in H1 2025. The company faces an urgent need to improve its financial health and translate revenue into profit.

Navigating Macroeconomic Headwinds

The global environment presents both opportunities and risks for any semiconductor stock analysis. While the overall industry growth is a tailwind, WITHTECH must navigate several macroeconomic factors:

- •Interest Rates: A high-interest rate environment, particularly in the U.S., increases borrowing costs, which can strain a company working to improve its financial standing.

- •Exchange Rates: Fluctuations in the EUR/KRW and USD/KRW rates can impact the value of foreign currency assets and liabilities, affecting both revenue from exports and the cost of imported components.

- •Supply Chain & Logistics: As noted by the rising China Containerized Freight Index, global supply chain instability persists. This can lead to increased logistics costs, directly impacting WITHTECH’s bottom line. For more on this, see analysis from sources like The Wall Street Journal’s logistics reports.

Investment Strategy: A Prudent Approach to WITHTECH Stock

Our overall opinion on a WITHTECH investment is currently “Neutral.” The company holds significant growth potential validated by the SK hynix contract, but this is balanced by the critical challenge of improving profitability.

The core investment thesis hinges on whether WITHTECH can leverage its top-line momentum to achieve operational efficiency and deliver sustainable profit growth. A cautious, monitoring-focused approach is advised.

Short-Term Outlook (1-3 Months)

Investors should closely watch for initial market reactions to the deal and the company’s next quarterly earnings report. Look for specific commentary on cost management strategies during the SK hynix contract execution. A strategy of staggered buying or observing from the sidelines is recommended until clear signs of margin improvement appear.

Mid- to Long-Term Outlook (6+ Months)

The long-term health of WITHTECH stock depends on two key factors: the sustained growth of its core AMC business and tangible progress in its new ventures, particularly the nuclear power plant decommissioning analysis unit. Investment decisions should be guided by evidence of improving financial health and the successful expansion into these new, high-potential markets.