In a bold financial maneuver, battery recycling specialist SungEel HiTech Co., Ltd. has announced its decision to extinguish ₩50 billion in SungEel HiTech convertible bonds. This move, executed amidst a challenging secondary battery market and macroeconomic headwinds, is being positioned as a decisive step to bolster shareholder value and prevent share dilution. But is this bond burn a genuine turning point for the company’s struggling stock, or a temporary fix for deeper financial issues?

This comprehensive analysis delves into the strategic rationale behind the decision, its potential impact on the SungEel HiTech stock price, and what investors should be watching for in the coming months. We’ll break down the company’s current financial health and provide a clear outlook on whether this move can truly pave the way for a sustainable recovery.

The Landmark Decision: Extinguishing ₩50 Billion in Convertible Bonds

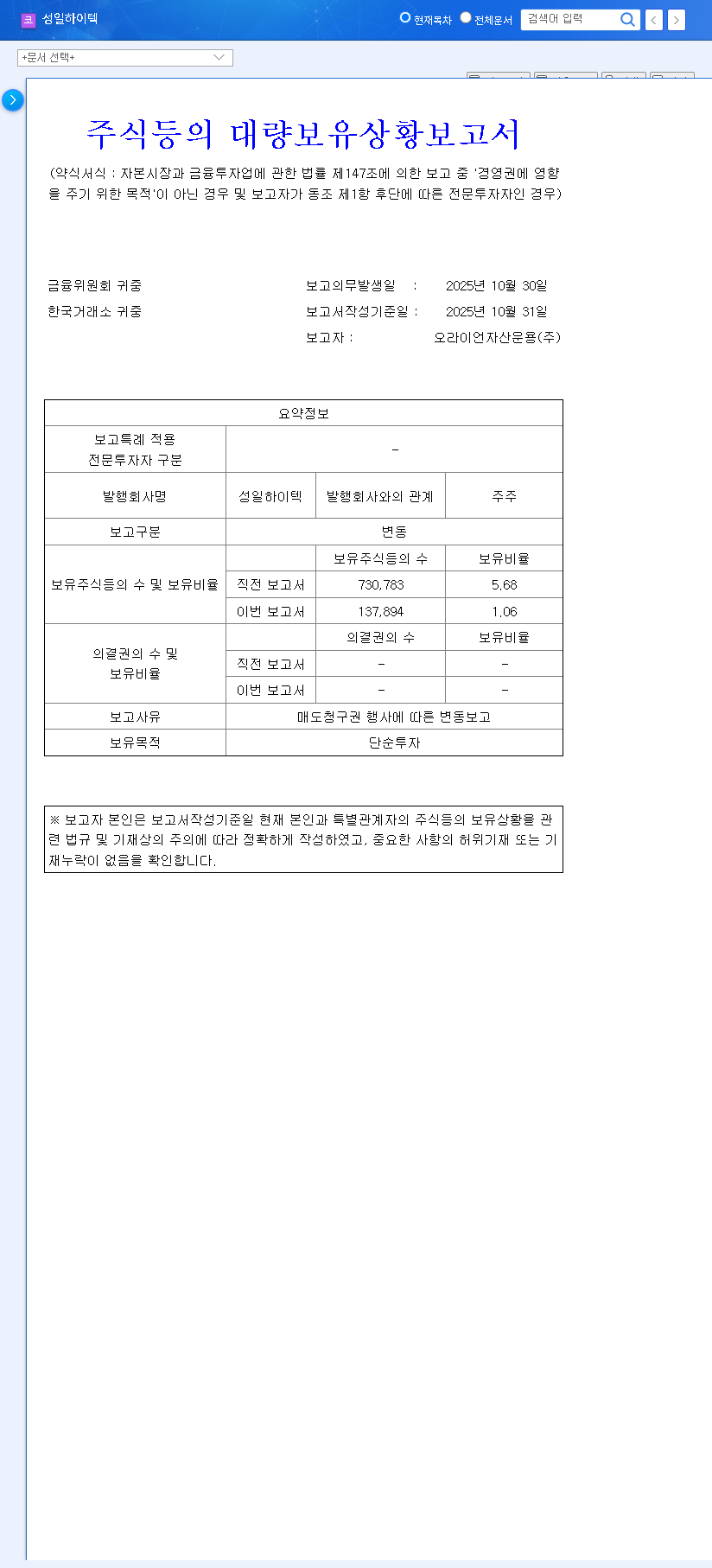

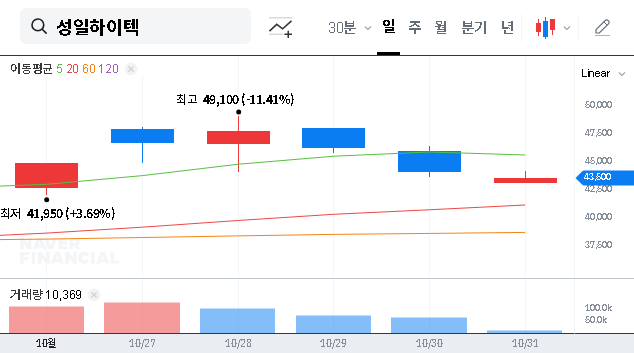

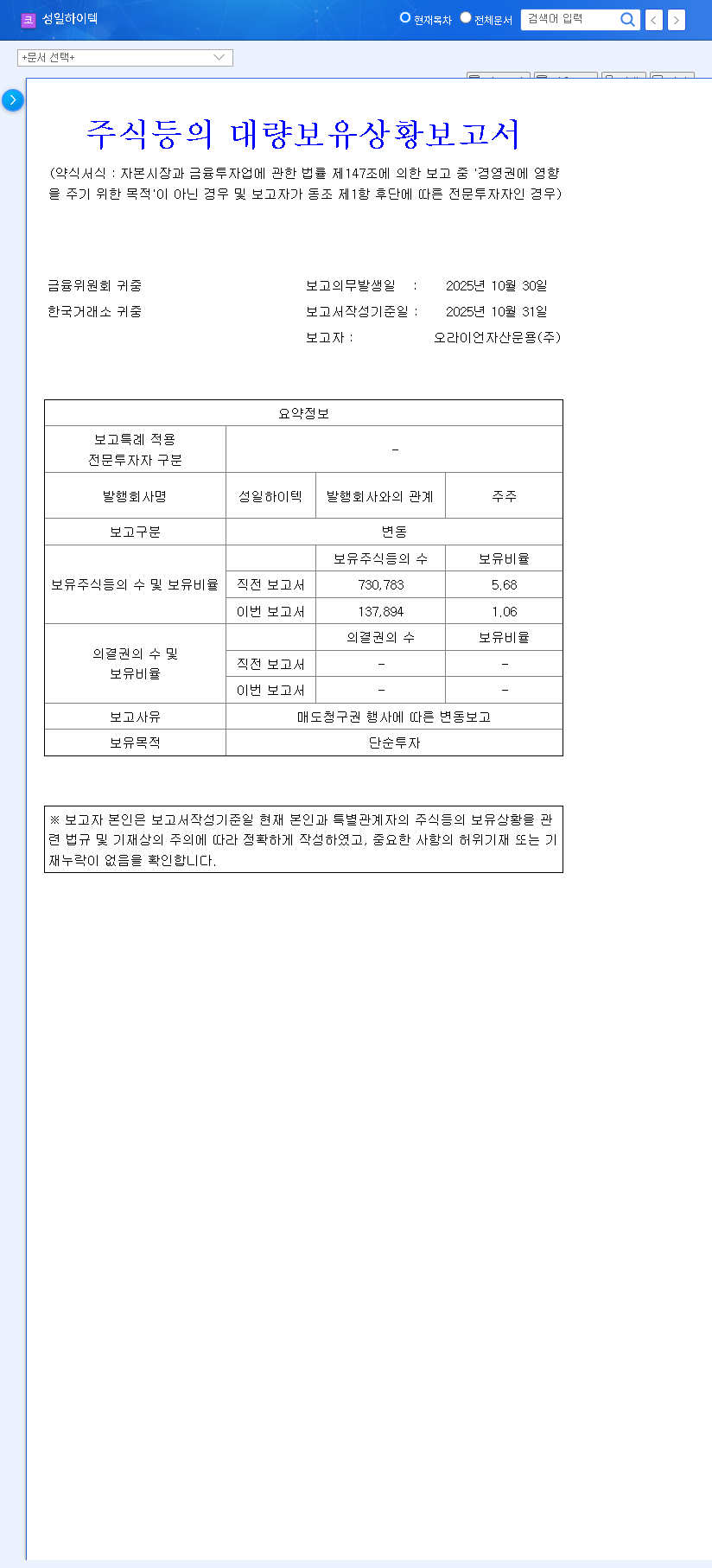

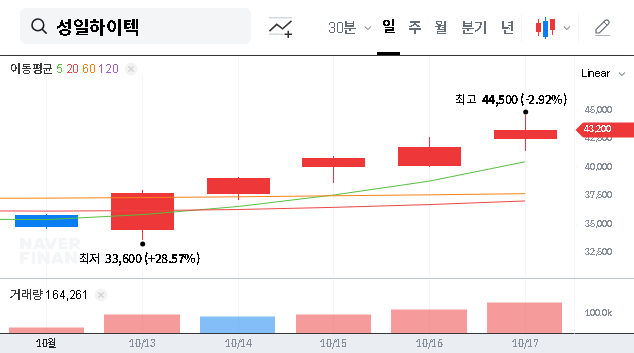

On November 10, 2025, SungEel HiTech’s board of directors passed a resolution to extinguish the entire ₩50 billion worth of its third-tranche convertible bonds (CBs), a decision that was finalized on November 12, 2025. This action, officially documented in the company’s public filing (Official Disclosure), effectively removes these bonds from existence. By repurchasing and canceling its own bonds, the company eliminates the potential for them to be converted into new shares, an event that would dilute the ownership stake of existing shareholders.

In corporate finance, extinguishing convertible bonds is a clear signal to the market. It demonstrates management’s confidence in the company’s future and a direct commitment to protecting and enhancing shareholder value.

Why Now? The Context Behind the Bond Burn

This decision wasn’t made in a vacuum. It comes at a critical juncture for SungEel HiTech, which has been grappling with significant financial and market-related challenges. Understanding this context is key to evaluating the move’s long-term effectiveness.

Deteriorating Financial Health

The company’s fundamentals have shown signs of strain, raising concerns among investors:

- •Revenue Decline: In the first half of 2025, revenue fell by 8.8% year-over-year to ₩64.01 billion, driven by a slowdown in the EV market which impacted secondary battery material sales.

- •Widening Losses: Operating losses grew to ₩32.9 billion due to a higher cost of goods sold and increased administrative expenses, highlighting profitability challenges.

- •Soaring Debt: The debt-to-equity ratio surged from 202.25% to an alarming 287.72%, signaling increased financial risk.

- •Negative Cash Flow: Operating cash flow turned negative at ₩-32.15 billion, raising questions about the company’s ability to generate cash from its core operations.

Unfavorable Market Conditions

External factors have further compounded SungEel HiTech’s problems. The sustained slowdown in the global battery recycling and EV industries has directly hurt performance. Additionally, currency volatility and high interest rates pose ongoing risks to profitability and increase the burden of debt servicing. While new EU regulations on waste battery recycling present a long-term opportunity, their immediate benefits are muted by low market utilization, a trend affecting the entire sector.

Analyzing the Impact of the SungEel HiTech Convertible Bonds Extinguishment

The decision to burn the bonds will have a multifaceted impact on the company.

- •Positive: The primary benefit is the immediate enhancement of shareholder value by eliminating dilution risk. It also directly improves the balance sheet by reducing total debt and lowering the debt-to-equity ratio, which can restore a degree of investor confidence and improve long-term financial stability.

- •Neutral: This is a financial engineering move, not an operational one. It does not inherently increase revenue or improve profit margins. Therefore, its direct contribution to solving the company’s core performance issues is limited. The ₩50 billion cash outflow was for maturing bonds, so it doesn’t create a new burden but rather settles an existing one.

- •Negative: The ₩50 billion cash outlay could temporarily strain liquidity. Given the company’s negative operating cash flow, careful management of remaining cash reserves will be absolutely critical to navigate the upcoming quarters without issue.

Investor Outlook: Cautious Optimism Required

For investors, the extinguishment of the SungEel HiTech convertible bonds is a welcome sign of proactive financial management. It demonstrates a commitment to shareholder interests and helps clean up the balance sheet. However, this action alone is not a silver bullet.

The fundamental challenges of declining revenue and poor profitability remain. A sustained turnaround in the SungEel HiTech stock price will depend entirely on the company’s ability to strengthen its core business and improve its operational performance. Any stock price rally based solely on this news may be short-lived unless it is followed by tangible improvements in upcoming quarterly reports.

Key Factors to Monitor:

- •Performance Improvement: Watch for any signs of revenue growth or margin improvement in the second half of 2025.

- •Cash Flow Management: Scrutinize the company’s ability to manage its cash reserves and return to positive operating cash flow.

- •Market Recovery: Keep an eye on the broader EV and battery recycling markets for signs of a rebound. More information on such instruments can be found from authoritative sources like Reuters Financial.

The investment thesis is one of ‘cautious observation.’ While the bond extinguishment is a positive step, the fundamental recovery of SungEel HiTech’s business remains the most critical driver for long-term investment success.