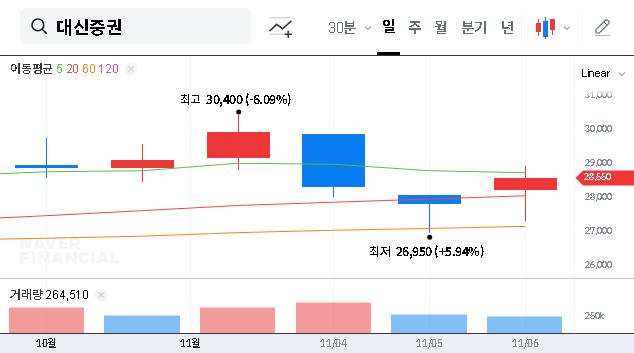

The latest DAISHIN SECURITIES Q3 2025 earnings report presents a fascinating and complex picture for investors. In a period of sustained market volatility, the company has posted a provisional earnings announcement that is stirring significant debate. On one hand, core business performance, reflected by operating profit, has shattered market expectations. On the other, the bottom-line net income has faltered, raising critical questions about underlying financial health and future prospects.

This comprehensive DAISHIN SECURITIES earnings analysis will dissect these contrasting results, explore the driving factors behind them, and provide a strategic guide for current and potential investors. What does this divergence signify for the DAISHIN SECURITIES stock, and how should you position your portfolio in response?

While operating profit surged an impressive 36% above expectations, net income unexpectedly dipped 6% below forecasts, creating a complex narrative that requires a deeper look beyond the headlines.

DAISHIN SECURITIES Q3 2025 Earnings: The Official Numbers

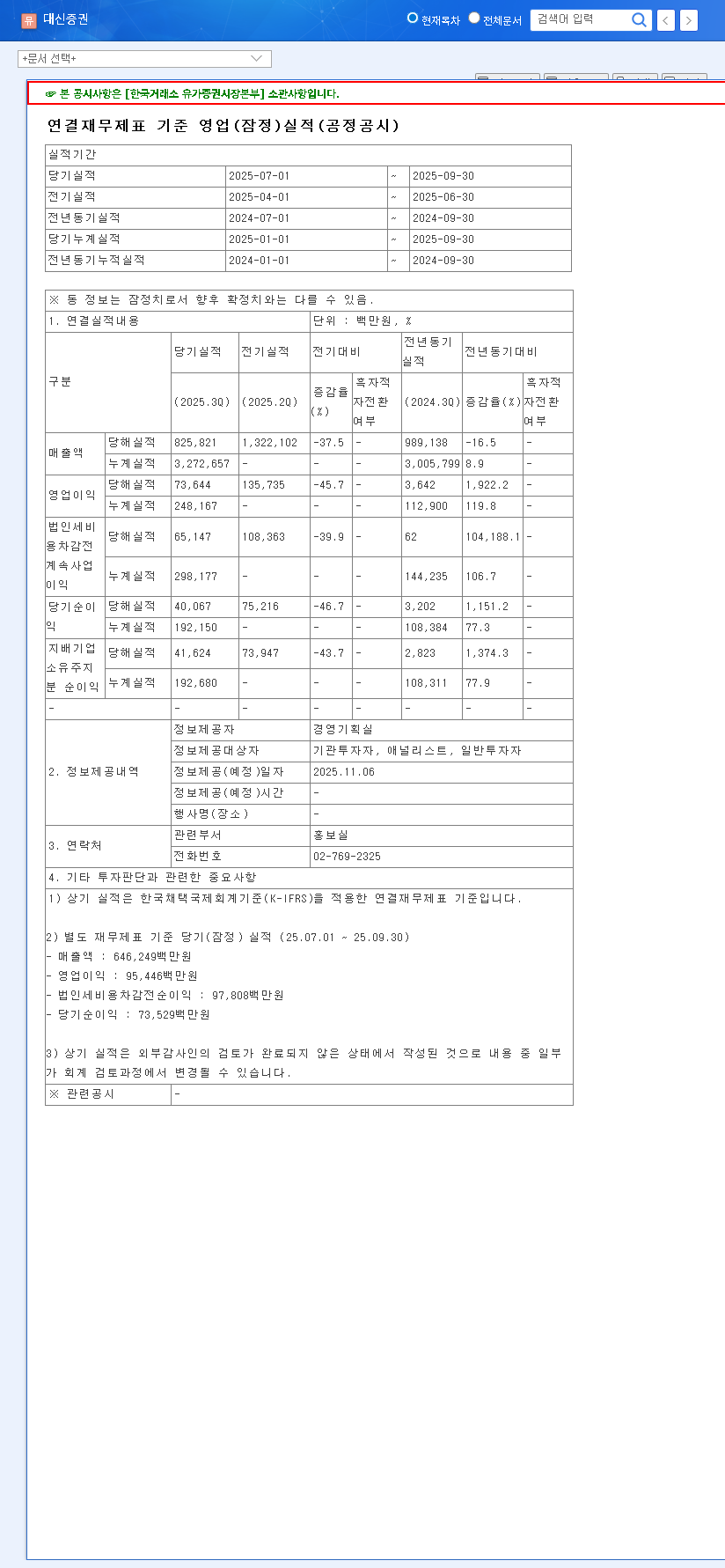

According to the provisional data disclosed on November 6, 2025, the company’s consolidated performance for the third quarter revealed the following key metrics. For a complete and unfiltered view, investors can review the Official Disclosure filed with the Financial Supervisory Service (DART).

- •Revenue: KRW 825.8 billion (Market Estimate N/A)

- •Operating Profit: KRW 73.6 billion (36% above the market estimate of KRW 54.3 billion)

- •Net Profit: KRW 41.6 billion (6% below the market estimate of KRW 44.3 billion)

The Bull & Bear Case: Deconstructing the Results

The core of this quarter’s story lies in the significant gap between operational success and net profitability. Let’s break down the positive and negative drivers influencing these outcomes.

The Bull Case: A Resilient Core Business

The standout figure—operating profit of KRW 73.6 billion—is a powerful testament to the strength of DAISHIN SECURITIES’ primary business activities. This performance indicates that segments like brokerage, investment banking, and asset management are thriving despite a challenging economic backdrop. The company has shown a remarkable turnaround, maintaining a strong positive operating profit trend since Q1 2025, following a loss in Q4 2024. This consistent recovery builds confidence in the management’s strategy and operational execution.

The Bear Case: The Mystery of the Net Income Miss

Despite the robust operating profit, the net income of KRW 41.6 billion is a point of concern. This shortfall suggests that factors outside of core operations negatively impacted the bottom line. Such factors could include:

- •Non-operating Losses: Losses from the valuation of financial assets, investments in associate companies, or foreign exchange translations could be significant culprits.

- •One-Time Expenses: A specific, non-recurring cost or a significant litigation provision could have dragged down net profit.

- •Higher Corporate Taxes: An increase in the effective tax rate for the quarter could also explain the discrepancy. For more details, investors might want to review our guide on analyzing a company’s income statement.

This quarterly decline in net income, when compared to Q1 (KRW 76.9 billion) and Q2 (KRW 75.2 billion), warrants close scrutiny in the full, audited report.

Market Outlook and Strategic Considerations

The forward-looking picture for securities company earnings is tied to broader market forces. A projected revenue decline for Q4 2025 could signal weakening investor sentiment or lower asset management fees. Furthermore, macroeconomic variables such as high KRW/USD exchange rates and interest rate policies from central banks can introduce significant volatility, as highlighted by recent global market analysis from Reuters. While stable U.S. Treasury yields may offer some stability, the overall environment remains uncertain.

The company’s previously stated purpose for holding treasury shares—to enhance shareholder value and improve its financial structure—is a positive signal of shareholder-friendly policies. However, its direct impact on near-term profitability remains to be seen.

Investor Guide: A Smart Action Plan

Given the mixed signals from the DAISHIN SECURITIES Q3 2025 earnings, investors should adopt a cautiously optimistic approach. While the operational recovery is encouraging, the potential red flags cannot be ignored. Here is a checklist for informed decision-making:

- •Analyze the Full Report: Wait for the finalized, detailed financial statements to pinpoint the exact cause of the net income decline.

- •Monitor Revenue Trends: Closely watch for signs that the company is developing new growth drivers to counter the potential slowdown in revenue.

- •Track Treasury Stock Utilization: Observe how and when the company uses its treasury stock to ensure it translates into tangible shareholder value.

- •Assess Macro-Environment: Stay informed about changes in exchange rates, interest rates, and overall market sentiment that directly affect the securities industry.

Frequently Asked Questions (FAQ)

What are the key takeaways from DAISHIN SECURITIES’ Q3 2025 earnings?

The key takeaway is a dual narrative: the company’s core operations are performing exceptionally well (operating profit up 36% over estimates), but its final net profit was dragged down by other factors (down 6% vs. estimates), signaling a need for deeper investigation.

Why did net income decrease while operating profit rose?

The most likely causes are non-operating factors. These can include valuation losses on investments, foreign exchange impacts, one-time expenses, or a higher-than-expected corporate tax bill. The full financial report will provide clarity.

What should investors watch for in the coming months?

Investors should focus on the detailed explanation for the net income miss, the company’s strategy to address declining revenue trends, and how management plans to use treasury stock to benefit shareholders.