The latest movements in Han’s Biome stock have caught the attention of the market, primarily driven by a significant development: Osstem Implant, a major shareholder, has reduced its stake. This action is more than just a line item on a report; it’s a signal that can have profound implications for the company’s valuation and future trajectory. For current and prospective investors, the key question is what this means for their investment strategy. Is this a warning sign or a temporary fluctuation in a complex market?

This comprehensive Han’s Biome stock analysis will dissect the details of Osstem Implant’s sale, evaluate the company’s underlying fundamentals, and assess the broader market environment. We will provide a clear, actionable framework to help you navigate the potential risks and opportunities ahead.

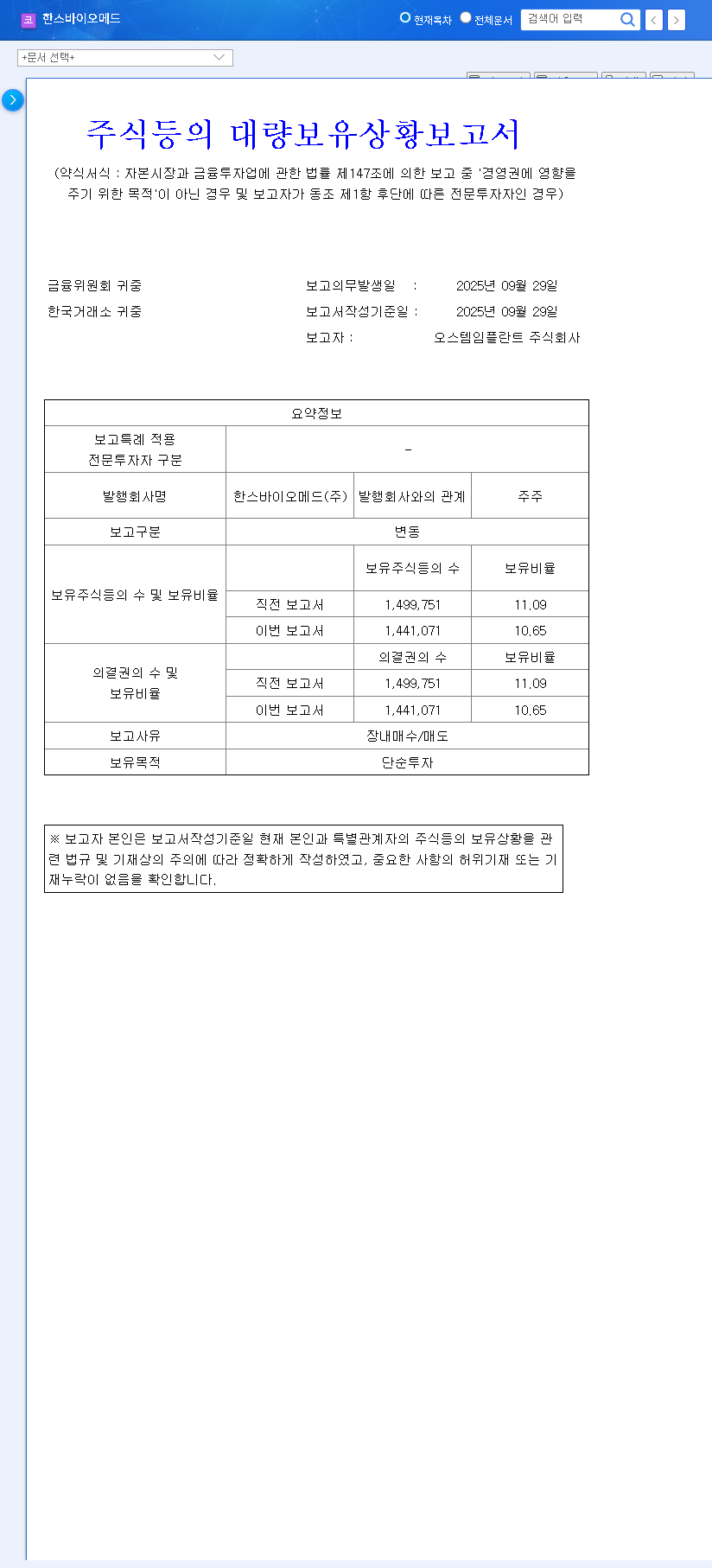

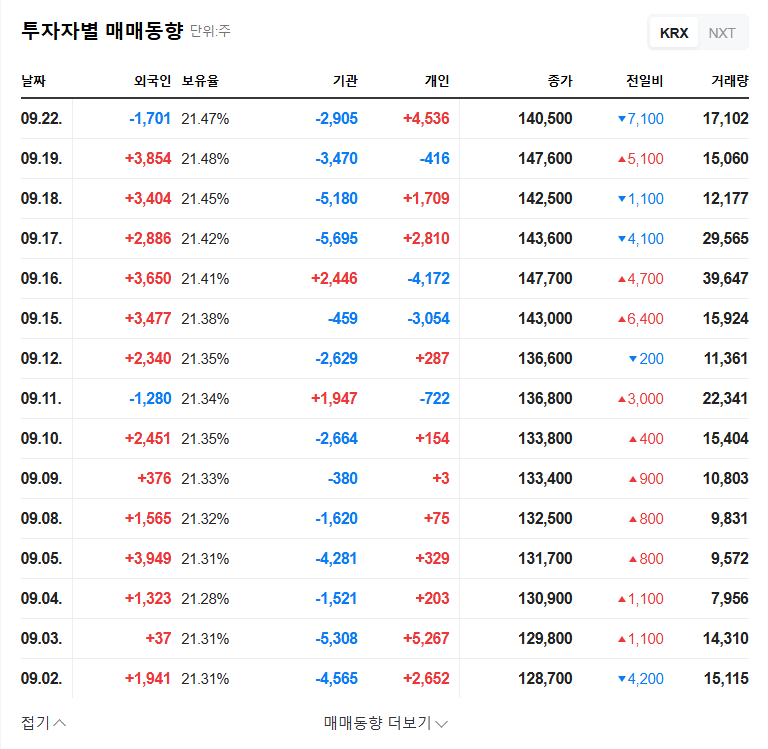

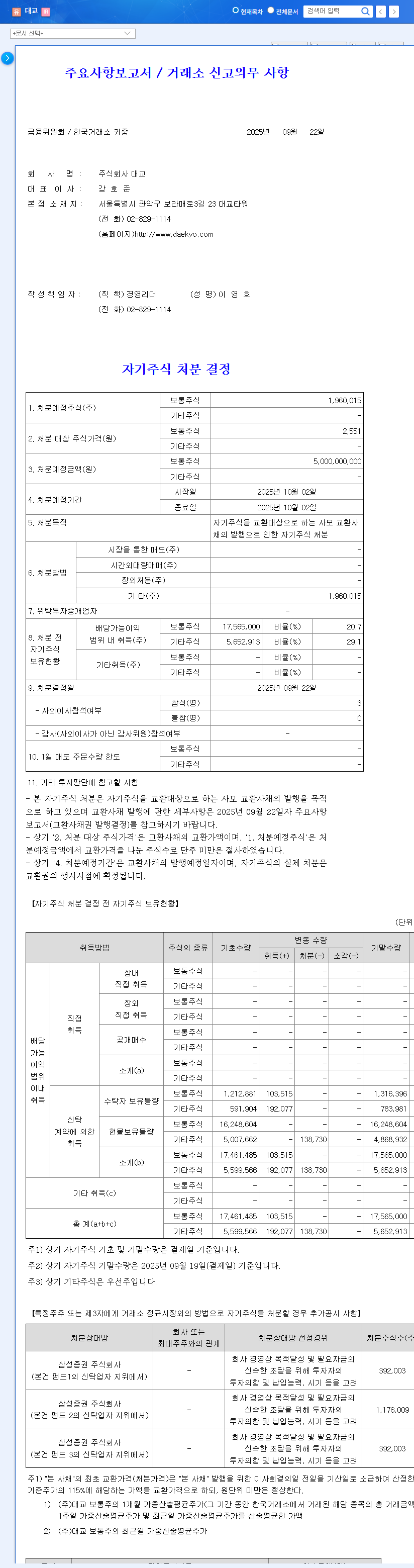

The Catalyst: Osstem Implant’s Stake Reduction

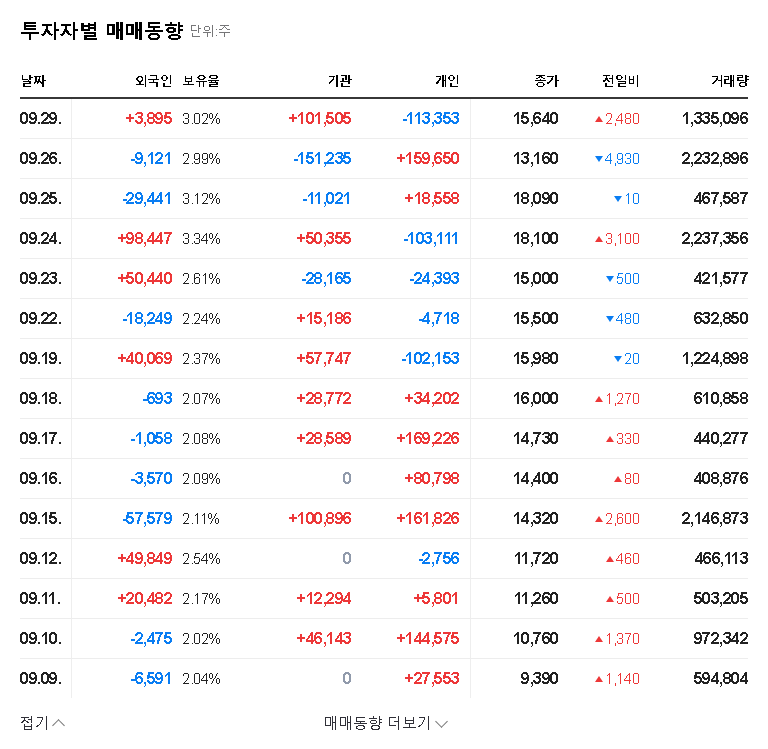

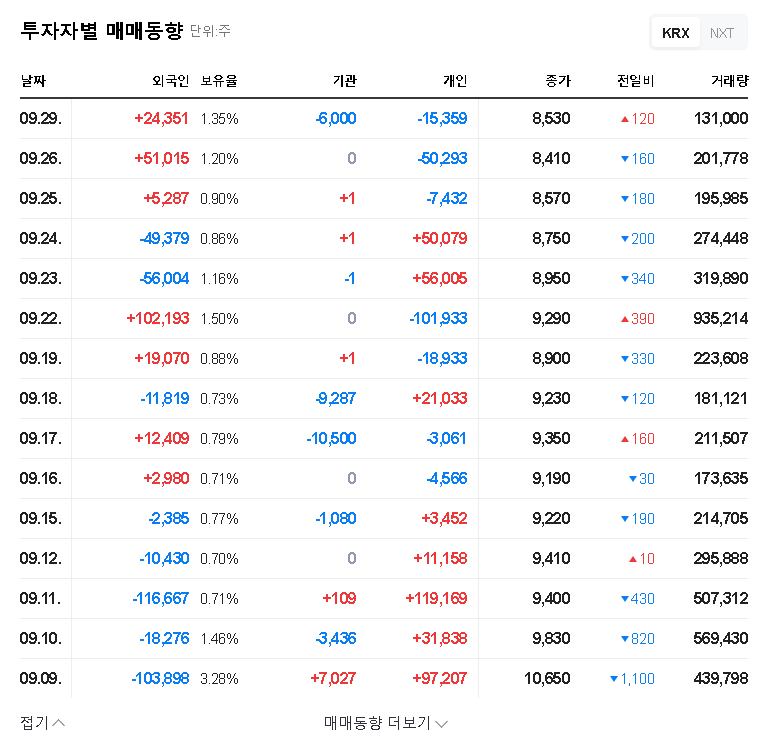

According to the official disclosure filed on September 30, 2025, Osstem Implant Co., Ltd. sold 64,000 shares of Han’s Biome Co., Ltd. on the open market. This transaction reduced its total holding from 11.09% to 10.65%, a decrease of 0.44 percentage points. While the stated purpose was ‘simple investment,’ such a move by a significant institutional holder often prompts a deeper look into the company’s health and outlook. You can review the complete filing here: Official Disclosure (DART).

When a major shareholder trims their position, the market takes notice. It’s crucial to determine if this is a strategic portfolio adjustment or a reaction to underlying weaknesses within the company.

Financial Health: A Look Under the Hood of Han’s Biome

A thorough analysis of the Q3 FY27 quarterly report reveals a mixed but concerning financial picture for Han’s Biome. Understanding these fundamentals is key to any sound investment strategy.

Revenue vs. Profitability

On the surface, the 69.4% year-on-year increase in operating profit seems positive. However, this is overshadowed by an 18.6% decline in revenue, which fell to KRW 66.065 billion. This suggests that while cost-cutting measures may be effective, the core business is shrinking. Furthermore, net income losses expanded significantly to KRW -4.203 billion, indicating that profitability at the bottom line remains elusive, a major red flag for Han’s Biome stock investors.

Business Segment Performance

The company’s performance is a tale of two segments. The Human Tissue segment shows solid growth and remains a core strength, bolstered by FDA clearances and its contract with Osstem Implant. Conversely, the Medical Device segment, despite the competitiveness of its ‘Mintlift’ product, is experiencing an overall revenue decline. Efforts in new ventures, like the ‘Revoss’ joint venture in China, are promising but have yet to contribute meaningfully to offset current weaknesses.

Key Risks and Financial Soundness

Several risks cloud the company’s future. The consolidated debt-to-equity ratio has climbed to 108.65%, and operating cash flow has deteriorated. This tightening financial position could limit the company’s ability to invest in growth or weather economic downturns. Additionally, major litigation risks persist, which could result in unforeseen financial liabilities. For a deeper dive into market trends, investors often consult resources like Reuters Market Data for broader context.

Analyzing the Ripple Effect on Stock Price

Osstem Implant’s sale is likely to impact Han’s Biome stock price forecast in both the short and long term.

- •Short-Term Impact: The immediate reaction could be negative. The sale acts as a bearish signal, potentially triggering a sell-off from retail investors and increasing stock volatility. Downward pressure is a distinct possibility as the market digests this news.

- •Medium-to-Long-Term Impact: The long-term effects depend on Han’s Biome’s ability to address its fundamental challenges. If the company can reverse the revenue decline and strengthen its balance sheet, this event will become a minor footnote. However, if performance continues to lag, Osstem’s sale might be seen as the first of many institutional exits, creating sustained pressure on the stock.

Investment Thesis: A Cautious Approach is Warranted

Given the combination of declining sales, financial risks, and the negative signal from Osstem Implant’s sale, a cautious investment approach is recommended. While there are positive aspects, the headwinds are significant. If you are new to this sector, consider reading our guide on how to evaluate biotech company stocks.

Investment Opinion: Cautious Sell or Hold

For current investors, holding the position while closely monitoring for signs of a turnaround—such as revenue recovery and litigation resolution—is a viable strategy. For new investors, it would be prudent to wait for more concrete evidence of fundamental improvement before initiating a position. The near-term outlook for Han’s Biome stock appears challenged, and better entry points may present themselves in the future.

Frequently Asked Questions (FAQ)

Why did Osstem Implant sell its Han’s Biome shares?

The official reason cited is ‘simple investment’ through an on-market sale. However, market analysts often interpret such moves as a strategic portfolio reallocation or a potential re-evaluation of the company’s growth prospects and intrinsic value.

What is Han’s Biome’s current financial health?

The company’s financial health is mixed. While operating profit saw an increase in Q3 FY27, this was against a backdrop of falling revenue. Key concerns include a widening net loss, a rising debt-to-equity ratio, and weakening operating cash flow.

What is the investment recommendation for Han’s Biome stock?

The current recommendation is ‘Cautious Sell or Hold.’ The combination of fundamental weaknesses and the negative market signal from the stake sale suggests significant near-term headwinds. Long-term success hinges on the company’s ability to execute a turnaround.