The recent Bohae Brewery treasury share acquisition has captured the attention of the market, signaling a pivotal moment for investors in BOHAE BREWERY CO.,LTD (000890). When a company buys back its own stock, it’s often a sign of confidence in its own future and a direct commitment to increasing shareholder value. This strategic move, backed by improving financial health, warrants a closer look. This comprehensive analysis will break down the details of the acquisition, evaluate the company’s underlying fundamentals, and provide a clear roadmap for what this means for the Bohae Brewery stock price.

This analysis explores Bohae Brewery’s 100 million KRW share buyback, its improved H1 2025 financial performance, and the potential impact on its stock valuation and long-term investor returns.

The Details: What We Know About the Share Buyback

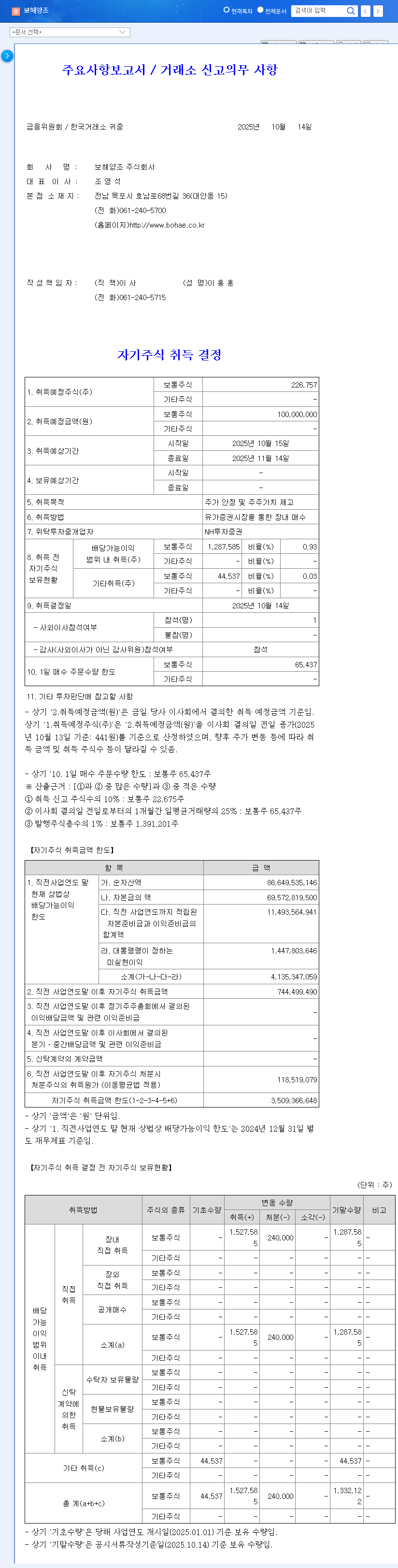

On October 14, 2025, Bohae Brewery formally announced its plan to acquire its own shares from the open market. According to the Official Disclosure (Source: DART), the primary goals are to stabilize the stock price and boost shareholder value—two key pillars of investor confidence. The specifics of the plan are as follows:

- •Total Acquisition Value: 100 million KRW

- •Number of Shares: Approximately 226,757 common shares.

- •Percentage of Market Cap: This represents about 0.16% of the company’s total market capitalization.

- •Method: On-market purchases via the KOSPI exchange.

Under the Hood: Analyzing Bohae Brewery’s Financial Health

A share buyback is most meaningful when it’s supported by strong company fundamentals. Bohae Brewery’s decision appears well-founded, based on its impressive performance in the first half of 2025.

Profitability Turnaround

The H1 2025 report reveals a significant positive shift. While revenue saw a slight dip to 43.19 billion KRW, the company’s strategic focus on cost reduction and efficient management of selling, general, and administrative (SG&A) expenses paid off. This resulted in an operating profit of 2.46 billion KRW and a net profit of 1.94 billion KRW, marking a successful return to profitability. This demonstrates operational excellence even in a challenging market.

A Rock-Solid Balance Sheet

Perhaps the most compelling metric is the company’s financial stability. The debt ratio has been dramatically reduced to a mere 6.91%, an exceptionally healthy figure that indicates very low financial risk. Combined with strong liquidity ratios and a substantial increase in operating cash flow, Bohae Brewery is not just profitable—it’s financially resilient and managing its working capital effectively.

Impact Analysis: What Does This Mean for the Stock?

The Bohae Brewery treasury share acquisition is a multifaceted event with both immediate and long-term implications for the stock price.

The Bull Case: Positive Signals for Investors

The buyback sends a powerful message: management believes the stock is undervalued. This can create a floor for the stock price, providing downside protection. By reducing the number of shares outstanding, the company increases its earnings per share (EPS), a key metric for valuation. This act of confidence, coupled with solid fundamentals, is likely to improve investor sentiment and attract new capital. To learn more about how buybacks work, you can read this guide on stock buybacks from Investopedia.

The Bear Case: Important Considerations

While positive, it’s crucial to maintain perspective. The acquisition size of 100 million KRW (0.16% of market cap) is relatively modest. Its direct impact on supply and demand dynamics will be limited. Therefore, this single event is unlikely to trigger a massive, sustained rally. The long-term trajectory of the Bohae Brewery stock price will depend more on continued operational performance, market trends, and future shareholder return policies, such as dividend increases or more substantial buyback programs.

Investor Action Plan & Final Verdict

For current and prospective investors, this news should be viewed as a confirmation of the company’s positive direction. Here’s how to approach it:

- •Short-Term Outlook: View this as a stabilizing factor. The buyback provides support for the current stock price and enhances investor confidence, which could lead to modest near-term gains.

- •Long-Term Outlook: Focus on the bigger picture. The true driver of shareholder value will be sustained profitability, successful new product launches, and the company’s ability to navigate macroeconomic headwinds. Monitor future announcements regarding dividends and other capital allocation strategies. For a deeper dive into financial health, consider reading our guide on Understanding Financial Ratios for Stock Analysis.

In conclusion, the Bohae Brewery treasury share acquisition is a clear positive for the company. It validates the impressive financial turnaround and signals a commitment to rewarding shareholders. However, investors should see it not as a silver bullet for the stock price, but as one piece of a larger, encouraging puzzle. Prudent investment decisions will be based on a continued analysis of the company’s intrinsic value and its execution of long-term strategy.