The recent news surrounding CHEMTRONICS stock (089010) has captured the market’s attention. A significant divestment by a major shareholder, Axis Investment, has raised critical questions among investors. Is this a sign of underlying weakness, creating downward pressure on the stock price, or does it open a window of opportunity for those with a long-term perspective? This comprehensive CHEMTRONICS stock analysis will dissect the event, evaluate the company’s core fundamentals, and consider the wider market forces at play to provide a clear, actionable outlook for investors.

The Catalyst: Axis Investment’s Major Stake Sale

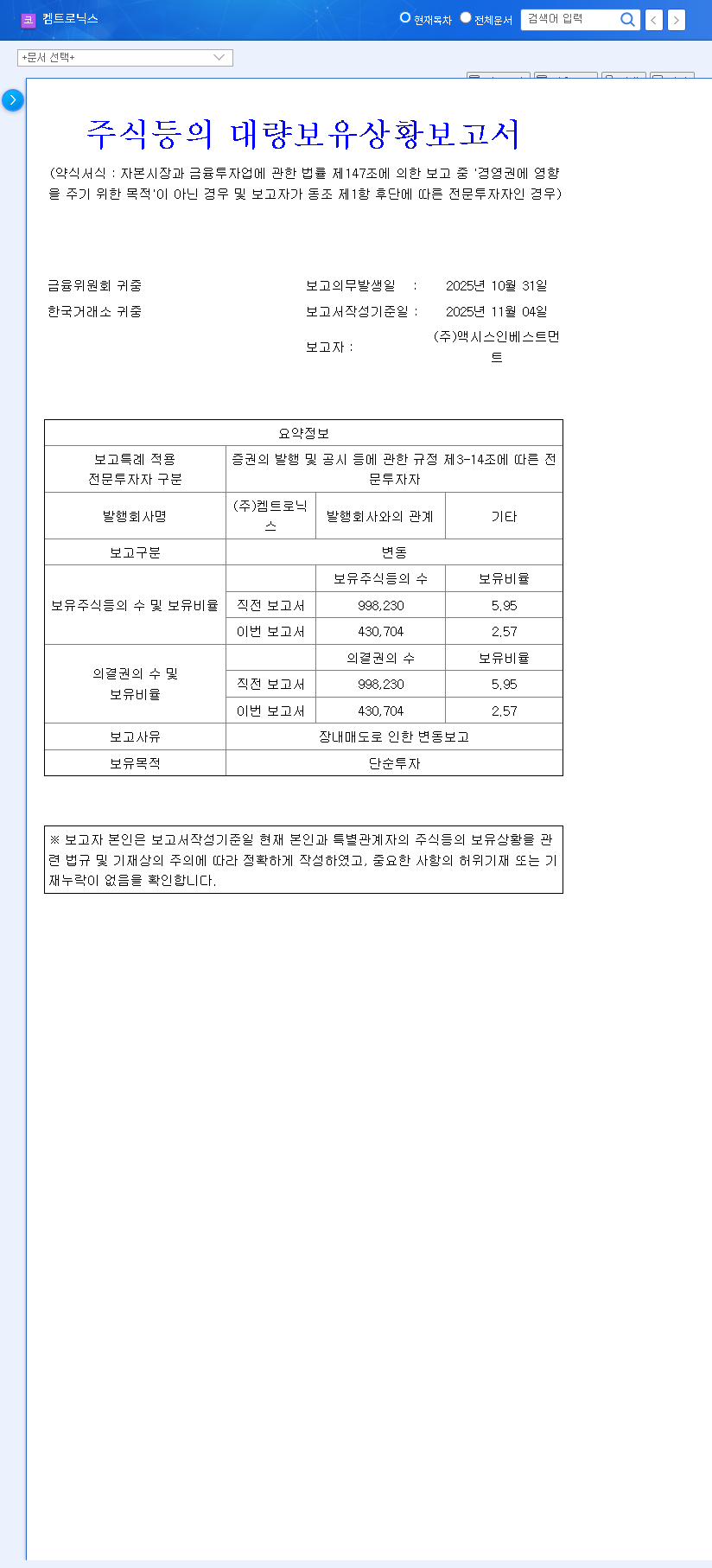

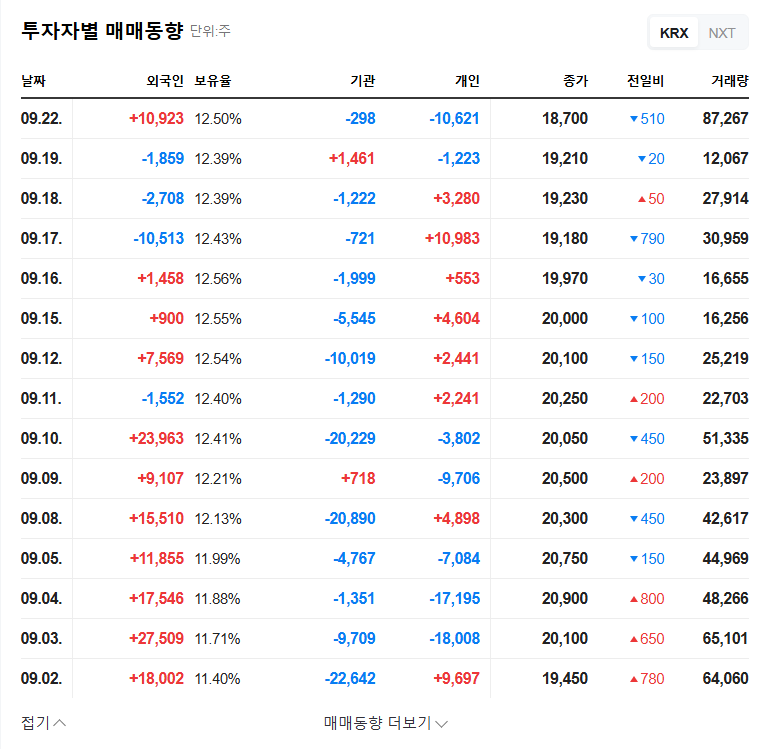

On November 4, 2025, a significant event unfolded for CHEMTRONICS. Axis Investment, along with related entities, announced a substantial reduction of their holdings. The details of this transaction were made public in an Official Disclosure, confirming the large-scale divestment through open market sales.

Axis Investment’s stake was reduced from 5.95% to 2.57%, a sale of approximately 3.38 percentage points of total shares, valued at roughly 694.4 billion KRW. This injection of shares into the market is a key factor influencing the current CHEMTRONICS stock price.

Deep Dive into CHEMTRONICS Stock Fundamentals

Beyond the immediate news, a sound investment decision requires a thorough look at the company’s underlying health and future prospects. This event provides an opportunity to reassess the fundamentals of the CHEMTRONICS stock.

Core Business and Growth Engines

CHEMTRONICS operates across several high-potential sectors, including advanced electronics, specialty chemicals, and automotive electronics. The company is actively developing future growth drivers that could significantly enhance its value:

- •EUV Materials: Development of materials for Extreme Ultraviolet lithography, a critical technology in next-generation semiconductor manufacturing.

- •Glass Substrate Technology: In-house processing technology for glass substrates, a key component for advanced displays and electronics.

- •Automotive Electronics Expansion: Growing its footprint in the automotive sector, supplying components for modern vehicles.

Recent Financial Headwinds

Despite these promising areas, the company’s performance in the first half of 2025 showed signs of weakness. A decrease in overall revenue and a notable decline in operating profit margins were primarily driven by reduced sales in the electronics and distribution segments. This mixed financial picture contributes to the uncertainty surrounding the 089010 stock.

The Broader Market Environment

No company operates in a vacuum. A complete CHEMTRONICS stock analysis must account for macroeconomic factors that could impact its performance. Investors should consider these external pressures, as discussed in many market analysis resources.

- •High Interest Rates: Elevated benchmark rates in the US and Korea increase borrowing costs for the company and can dampen overall investor sentiment.

- •Exchange Rate Volatility: Fluctuations in the KRW/USD and KRW/EUR exchange rates directly affect the profitability of CHEMTRONICS’ exports and imports.

- •Raw Material & Logistics Costs: The prices of international oil and shipping (e.g., Baltic Dry Index) can impact manufacturing costs and supply chain expenses.

Impact Analysis of the Stake Sale

Short-Term: Increased Selling Pressure

The most immediate consequence of the Axis Investment sale is the increased supply of CHEMTRONICS stock on the market. This surge in selling volume is likely to create short-term downward pressure on the stock price. Furthermore, the market may interpret the sale as a negative signal, regardless of the stated ‘simple investment’ purpose, leading to weakened investor confidence and potentially higher trading volatility.

Long-Term: A Renewed Focus on Fundamentals

In the long run, this event shifts the focus squarely back to the company’s performance. While the stake reduction is significant, Axis Investment’s remaining 2.57% holding does not pose an immediate threat to management control. The true test will be whether CHEMTRONICS can deliver on its growth promises. Investors should compare its progress to others in the sector, similar to how one might analyze other semiconductor stocks. A dip in stock price could affect future capital raising, but sustained operational success will ultimately dictate the long-term value.

Action Plan for Prudent Investors

Given the current uncertainty, investors should adopt a cautious and analytical approach. Before making a decision on CHEMTRONICS stock, consider these key points:

- •Assess the Opportunity: Is a potential short-term price drop a genuine buying opportunity based on long-term value, or is it a reflection of deeper issues? A thorough analysis is critical.

- •Monitor Shareholder Activity: Keep a close eye on any further changes in shareholding by Axis Investment and watch for the emergence of new major investors.

- •Demand Performance Visibility: Look for concrete signs of sales and profitability improvement in upcoming quarterly reports. The performance of the EUV and automotive segments is particularly crucial.

- •Factor in Macro Trends: Continuously evaluate how macroeconomic indicators like interest rates and exchange rates are affecting the business environment for CHEMTRONICS.

Frequently Asked Questions (FAQ)

Why did Axis Investment sell its CHEMTRONICS stock?

The stated purpose was ‘simple investment’. The sale is likely a strategic move for portfolio rebalancing or to realize profits. No specific negative reason has been officially disclosed by the firm.

What is the immediate impact on the CHEMTRONICS stock price?

The large influx of shares is expected to increase selling pressure and could lead to a short-term downward trend in the stock price as the market absorbs the new supply.

Does CHEMTRONICS have long-term investment appeal?

CHEMTRONICS possesses strong future growth drivers in high-tech sectors like EUV and automotive electronics. However, its investment appeal is balanced against recent sluggish performance and macroeconomic risks. A patient approach focused on tangible performance improvements is advised.