In the fast-paced world of tech and gaming stocks, corporate disclosures are a critical window into a company’s health and strategic direction. The recently released KRAFTON shareholding report provides just such a window, offering investors crucial clues about governance stability and insider confidence. While the headline numbers suggest minimal change, a deeper dive reveals significant implications for the future of KRAFTON stock and its long-term strategy. This analysis will decode the nuances of this corporate disclosure, from CEO Jang Byung-gyu’s steadfast control to the subtle meaning behind minor executive purchases and stock option exercises.

We will explore what this report means for both short-term market sentiment and the long-term investment thesis for KRAFTON, the powerhouse behind global phenomena like PUBG: BATTLEGROUNDS.

Deconstructing the KRAFTON Shareholding Report

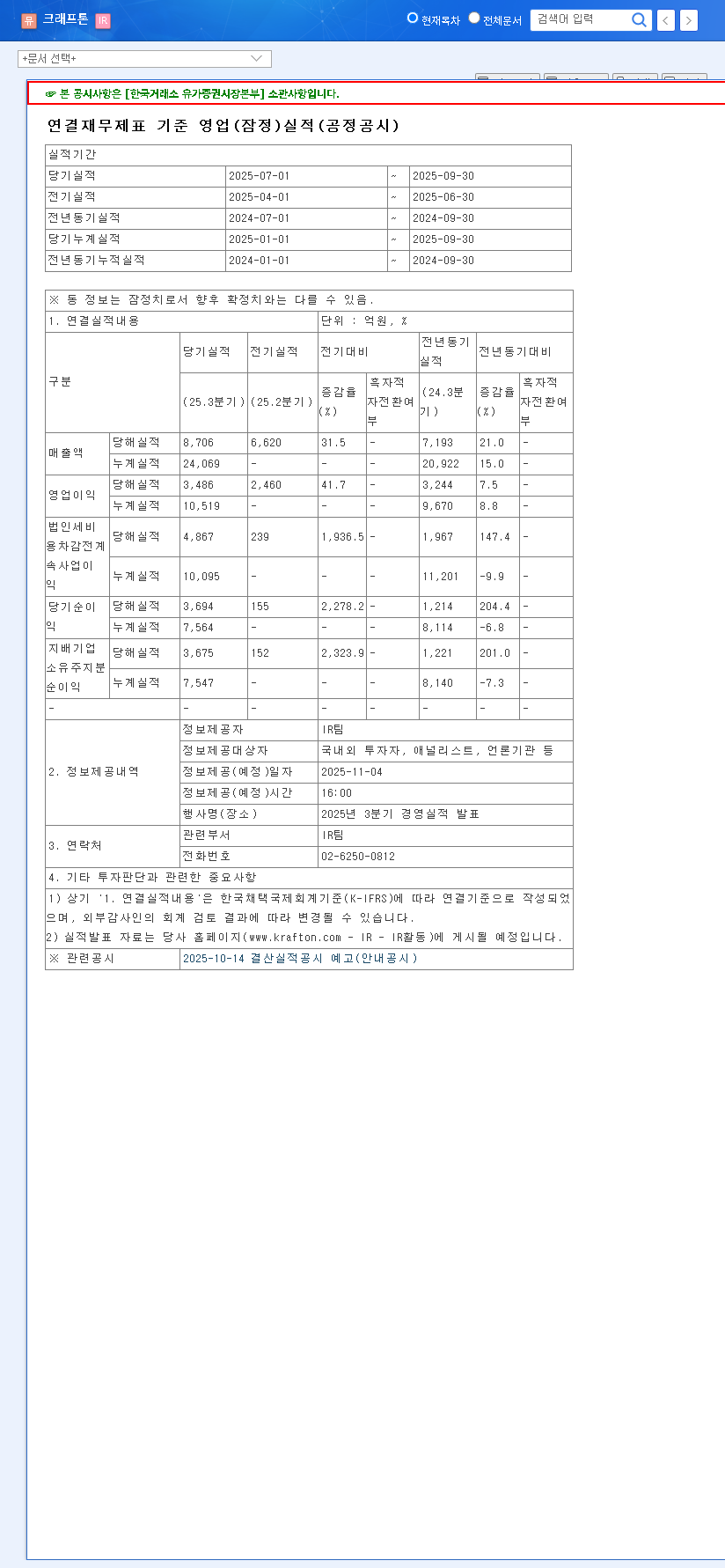

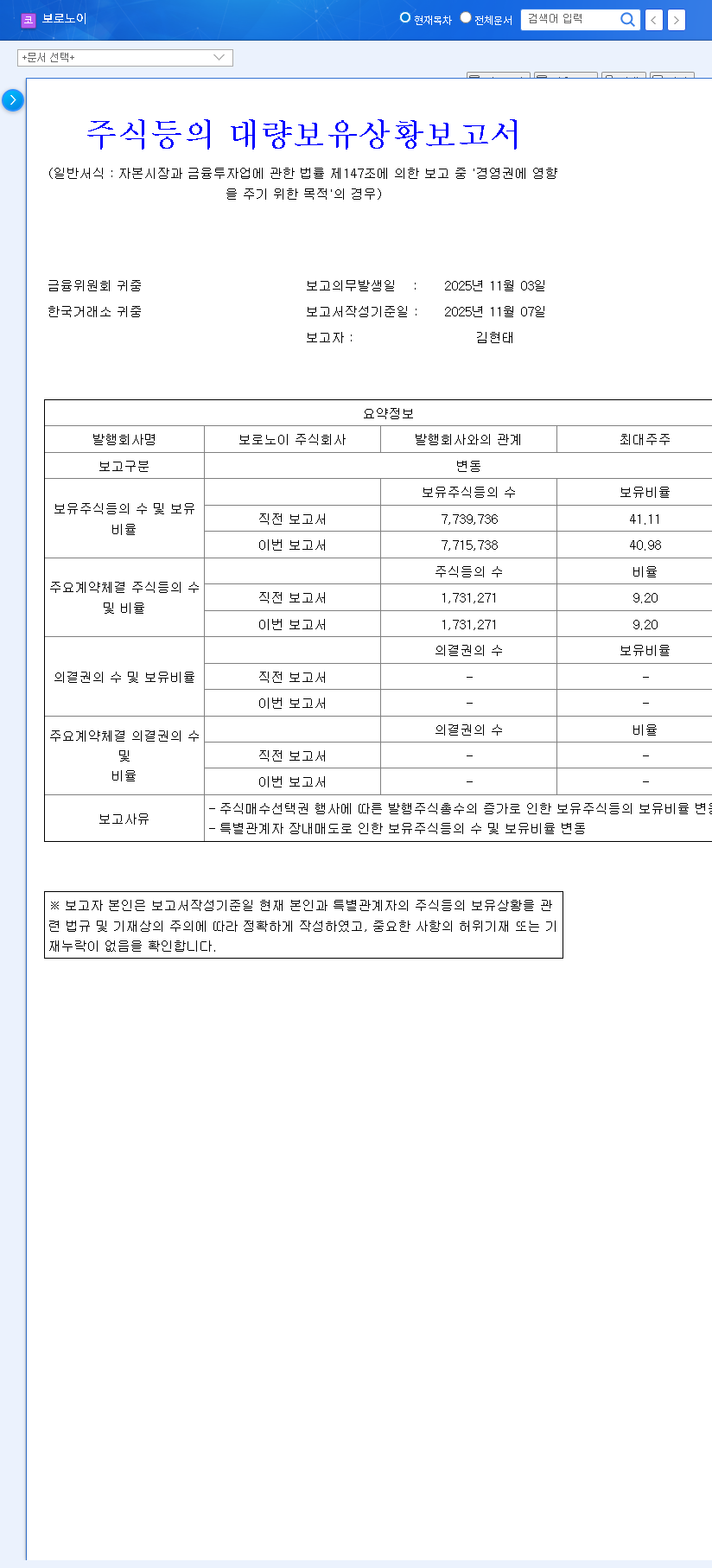

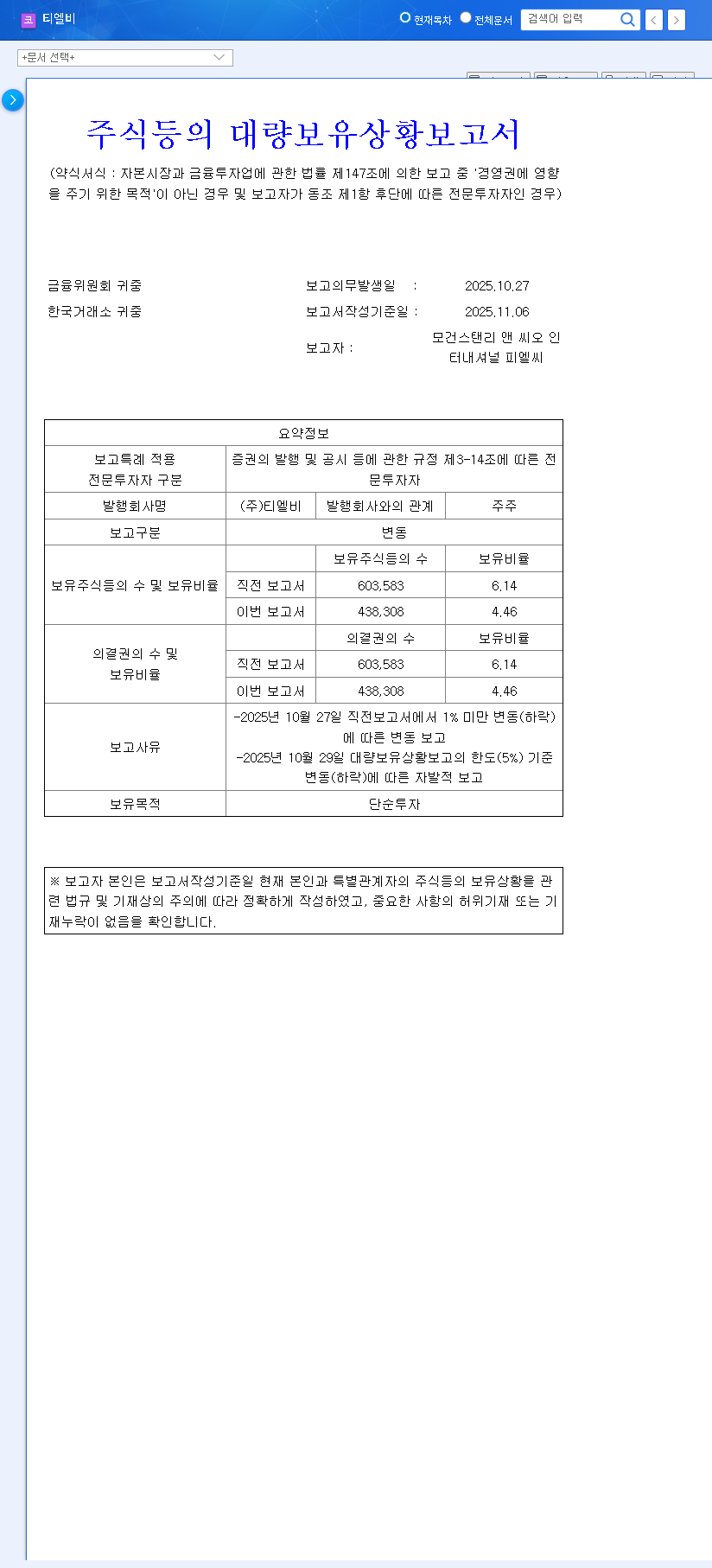

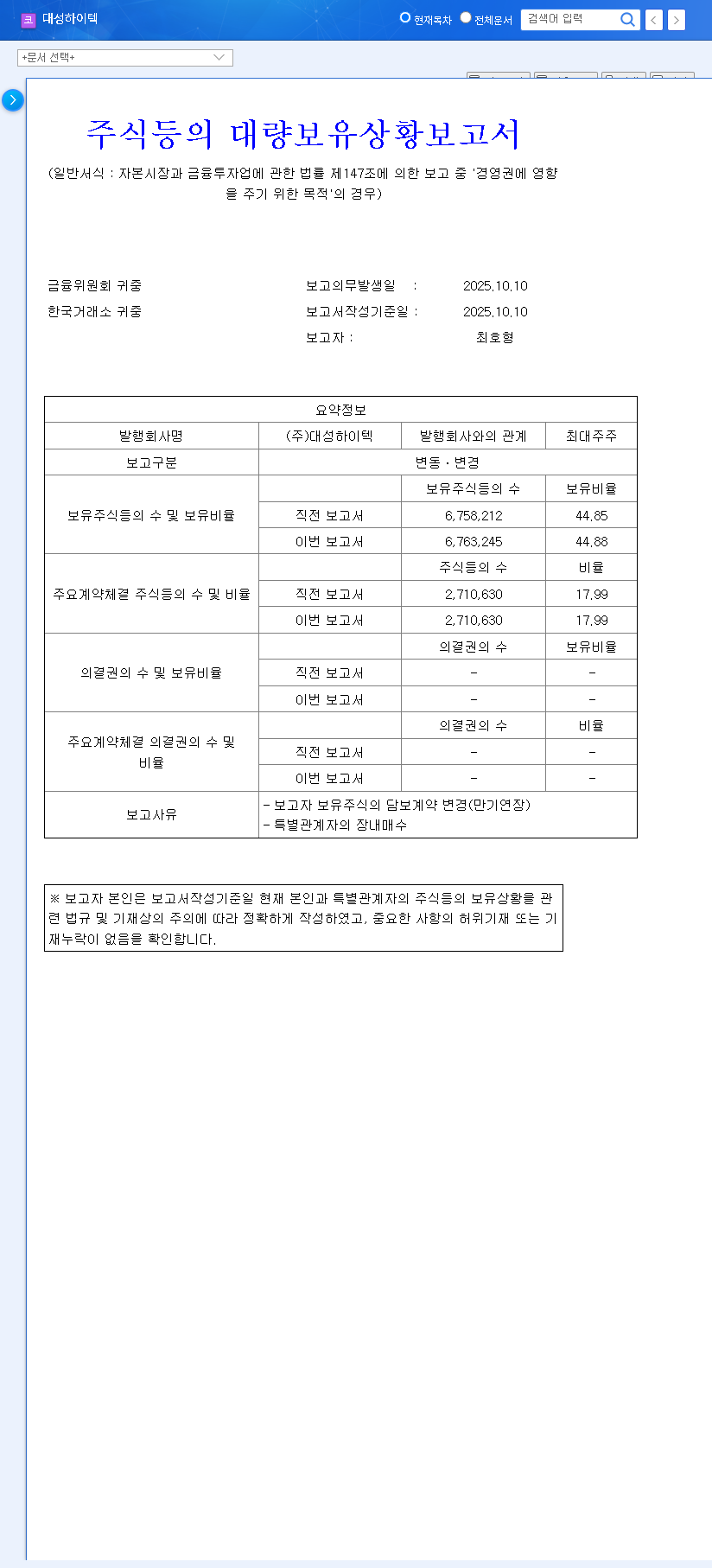

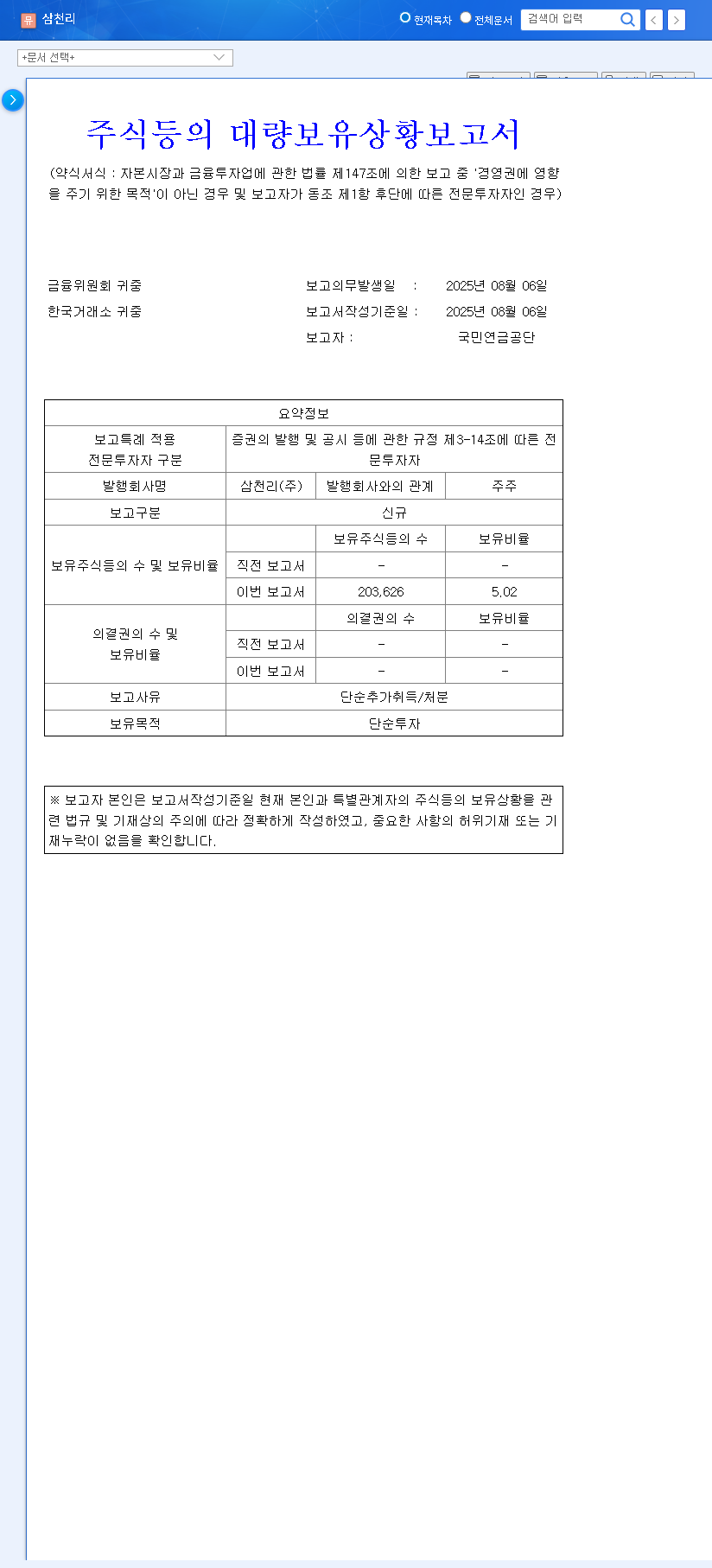

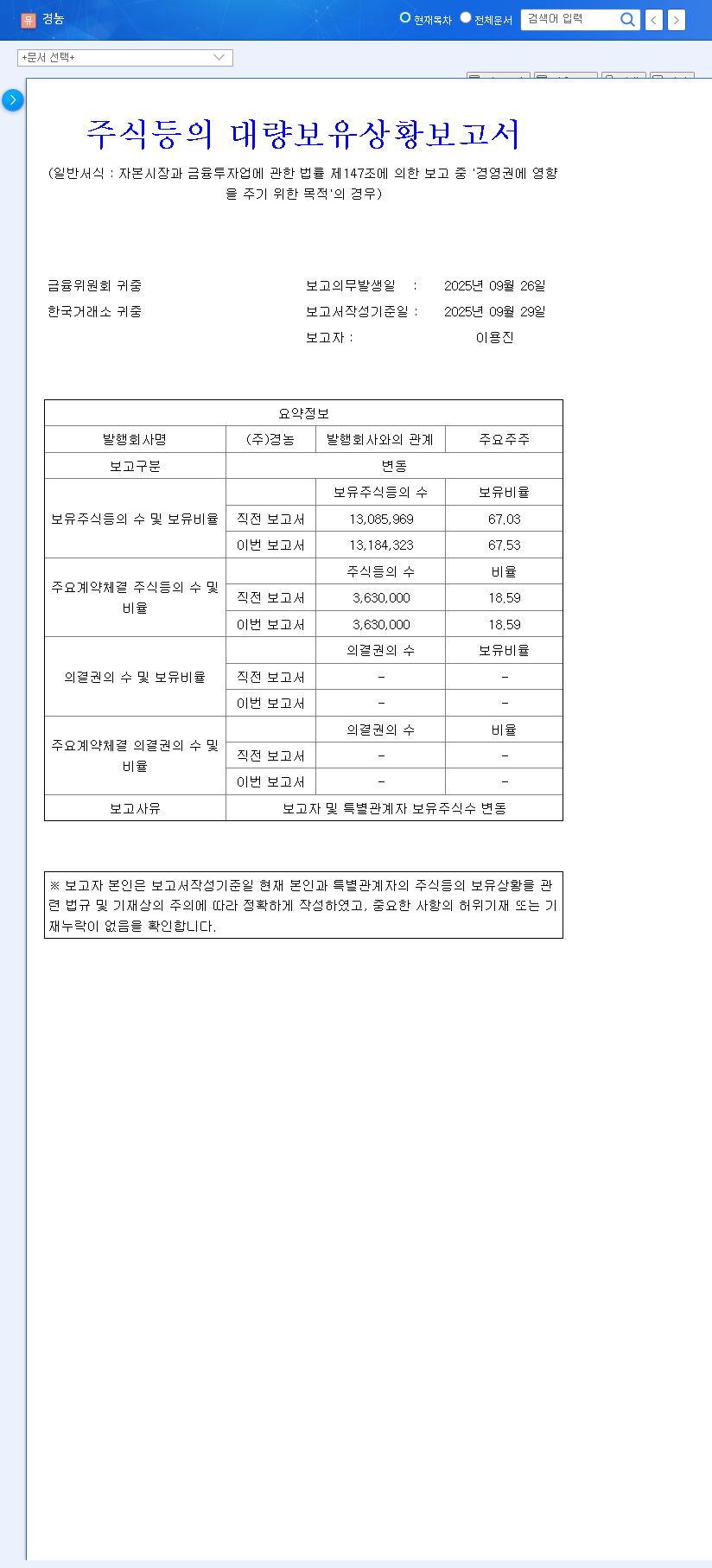

On November 14, 2025, KRAFTON, Inc. filed its official “Report on Large Shareholding Status.” This document, while seemingly routine, is essential for a thorough investor analysis. The full Official Disclosure provides the raw data, but the real value lies in its interpretation.

Key Takeaways from the Disclosure:

- •Chairman Jang Byung-gyu’s Unchanged Stake: The most critical piece of information is that Chairman Jang Byung-gyu’s ownership remains firm at 37.21%. This substantial holding is explicitly for ‘management influence,’ signaling a continued commitment to stable, long-term leadership.

- •Reason for Filing: The report was triggered by market purchases and the exercise of stock options by other individuals, not by a change in the Chairman’s position.

- •Minor Executive Purchase: Song Richard Kyong Chan made minor market acquisitions totaling 180 common shares, a small but symbolically positive gesture.

The stability of Chairman Jang Byung-gyu’s stake is the cornerstone of this report. For a company reliant on long-term IP development, consistent leadership is a significant asset that reassures the market and protects strategic initiatives from short-term pressures.

Investor Analysis: Reading Between the Lines

While the surface-level data shows little change, a sophisticated investor analysis requires looking deeper into the implications of this corporate disclosure.

The Strategic Importance of Stable Governance

Chairman Jang’s significant and stable shareholding is a powerful signal. In the gaming industry, success is often the result of multi-year development cycles and building enduring global franchises. A consistent leadership vision, free from the disruptions of shareholder activism or takeover threats, allows KRAFTON to invest confidently in ambitious projects, from new game development to pioneering the use of AI in its creative pipeline. This stability is a core component of the long-term investment case for KRAFTON stock.

Decoding the Mention of Stock Options

The report’s mention of ‘exercise of stock options’ deserves special attention. While the current impact is negligible, it serves as a reminder of potential future share dilution. Stock options are a common way for tech companies to incentivize key talent. When exercised, they create new shares, which can slightly dilute the ownership percentage of existing shareholders. Investors should monitor future disclosures for the scale and frequency of these exercises, as they relate directly to the company’s compensation strategies and potential impact on earnings per share. For more on how market trends affect tech valuations, you can read insights from sources like Bloomberg.

Impact on KRAFTON Stock: A Forward Outlook

Short-Term Market Reaction

The immediate impact on KRAFTON’s stock price from this report is expected to be minimal. The market thrives on significant news, and the key takeaway here is ‘no change’ in the controlling stake. The minor purchases by another executive are a positive but immaterial signal. Therefore, short-term volatility is unlikely unless further details about large-scale option exercises emerge.

Mid-to-Long-Term Governance and Growth

In the long run, this report reinforces the thesis of stable corporate governance. This stability is a crucial backdrop for KRAFTON’s fundamental growth drivers, which include:

- •Successful monetization and expansion of its flagship PUBG IP.

- •Strategic M&A activity to acquire new studios and technologies.

- •Investments in AI and next-generation gaming platforms.

Ultimately, an investment decision should be based on these fundamental factors, not solely on this shareholding report. For a deeper look at the company’s performance, consider reviewing our analysis of KRAFTON’s Q3 2025 earnings.

Frequently Asked Questions (FAQ)

Did KRAFTON CEO Jang Byung-gyu sell any shares?

No. According to the latest KRAFTON shareholding report, Chairman Jang Byung-gyu’s stake remains unchanged at 37.21%. This reinforces his commitment to management control and the company’s long-term strategy.

Will the minor share purchases affect KRAFTON’s stock price?

The purchase of 180 shares by executive Song Richard Kyong Chan is too small to have a material impact on the stock price. It is best viewed as a minor vote of confidence rather than a significant market event.

Should I invest in KRAFTON based on this corporate disclosure?

This report confirms governance stability, which is a positive factor. However, making an investment decision requires a comprehensive analysis of KRAFTON’s fundamentals, including revenue growth, new game pipeline, profitability, and the competitive landscape. This report is one piece of a much larger puzzle.