DI Corporation recently announced a major financial maneuver involving the disposition of treasury stock and the issuance of exchangeable bonds, sending ripples through the investment community. This DI Corporation stock analysis explores the critical question on every shareholder’s mind: What is the real share price impact of this decision? While the company’s semiconductor division is thriving, underlying financial health concerns and struggling business segments cast a shadow. We will dissect the company’s core fundamentals, evaluate the consequences of the DI Corporation treasury stock sale, and offer a clear-eyed view for potential investors.

The Catalyst: A Closer Look at the Announcement

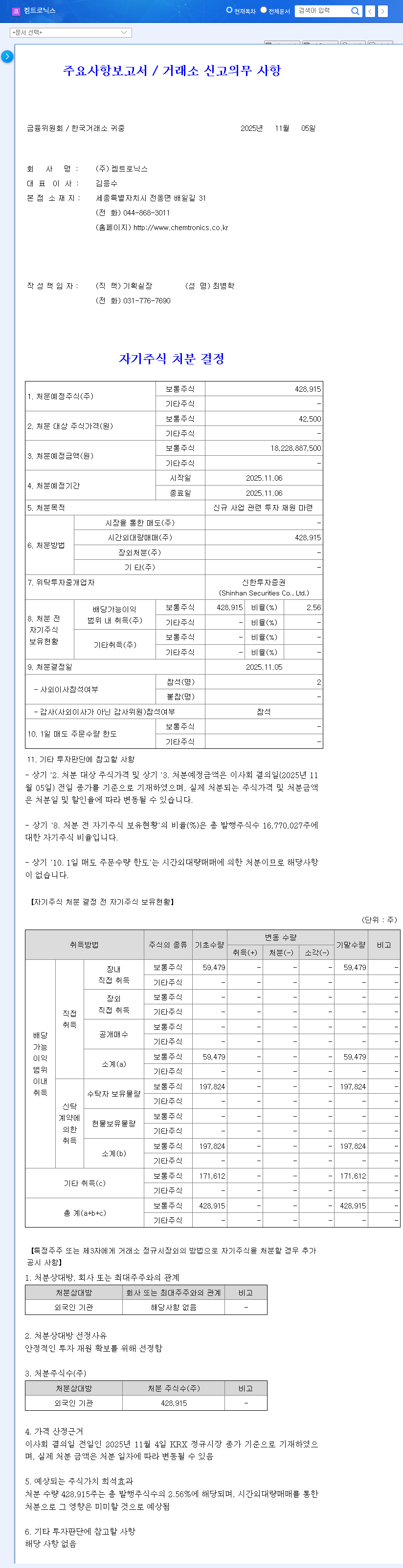

On November 13, 2025, DI Corporation confirmed its decision to dispose of 1,103,915 treasury shares, valued at approximately 30 billion KRW. According to the Official Disclosure filed with DART, these shares, representing 3.9% of total common stock, are being used to back a private issuance of exchangeable bonds. This move signals a significant pivot in the company’s capital-raising strategy, aiming to secure funds without immediately turning to traditional debt or public equity markets.

Decoding DI Corporation’s Financial Health

A comprehensive stock analysis requires looking beyond a single announcement. Based on its H1 2025 financial reports, DI Corporation presents a classic case of a company with a powerful growth engine alongside notable vulnerabilities.

Strengths: The Semiconductor Powerhouse

The company’s primary strength is its semiconductor equipment business, which is firing on all cylinders. In the first half of 2025, DI reported a consolidated revenue of 229.3 billion KRW and turned around to an operating profit of 22.2 billion KRW—a stunning 183.6% year-over-year revenue increase. This division now constitutes nearly 95% of total revenue, driven by soaring demand for its DDR5 and HBM inspection equipment. The company’s proactive development of next-generation wafer testers shows it is well-positioned for future industry shifts. Furthermore, a positive operating cash flow of 22.5 billion KRW marks a significant improvement in operational efficiency.

Weaknesses: Financial Strains and Lagging Divisions

However, the picture is not entirely rosy. Other business units, such as electronic components and audio equipment, are underperforming and generating operating losses. The once-promising secondary battery business has been temporarily suspended. These lagging segments are a drag on overall profitability. More concerning are the signs of financial strain: the debt-to-equity ratio has climbed to 111.37%, and a recent credit rating downgrade to BB(+) could increase future borrowing costs. This financial fragility is a key risk factor for investors to monitor.

The core challenge for DI Corporation is to leverage its semiconductor dominance to shore up its overall financial structure and either revitalize or divest its underperforming assets. The new capital is a critical tool in this endeavor.

Analyzing the Impact of the Treasury Stock & Bond Strategy

This financial strategy has both immediate and long-term implications for the share price impact and shareholder value.

- •Share Dilution Concerns: Releasing 1.1 million treasury shares into the market increases the total number of outstanding shares. This can lead to short-term share dilution, potentially putting downward pressure on the stock price as each share now represents a smaller piece of the company. The exchangeable bonds also carry a future dilution risk if and when bondholders exercise their right to convert them into stock.

- •Strategic Use of Capital: The long-term market reaction will depend heavily on how DI Corporation uses the 30 billion KRW. If deployed effectively for high-return R&D, strategic acquisitions in the semiconductor space, or paying down high-interest debt, the move could be a significant long-term positive. Transparency regarding the fund’s utilization plan is paramount to earning investor confidence.

- •Market & Economic Outlook: The semiconductor industry outlook remains strong, as detailed by industry reports from sources like Gartner. However, global economic headwinds and intense competition are persistent risks. Investors should also follow our Deep Dive into the Semiconductor Industry’s Future for more context.

Investor’s Playbook & Final Recommendation

For investors considering DI Corporation, this decision introduces both opportunities and risks. A prudent approach is essential. The success of this capital raise hinges on management’s ability to translate funds into tangible growth that outweighs the effects of share dilution. While the semiconductor division provides a powerful tailwind, the company’s financial weaknesses cannot be ignored.

The final verdict will be written by how efficiently DI Corporation allocates this new capital. Close monitoring of quarterly reports for improvements in the debt ratio and progress in other business segments will be key to making an informed investment decision.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. All investment decisions should be made with the consultation of a qualified financial advisor.