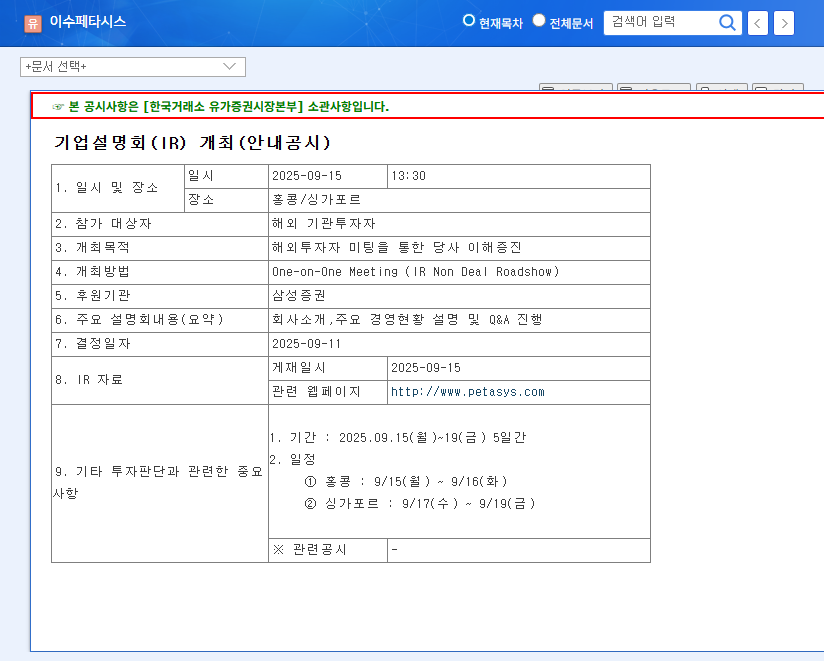

The upcoming ISUPETASYS Investor Relations (IR) conference, scheduled for November 18, 2025, is more than a standard financial update; it’s a critical moment for investors tracking the AI revolution. As artificial intelligence and high-performance computing reshape global industries, the foundational hardware—specifically advanced Printed Circuit Boards (PCBs)—has become a linchpin for growth. ISUPETASYS CO., LTD has emerged as a key player in this rapidly expanding AI hardware market, and this IR event will provide a crucial look into its future trajectory and its potential impact on the ISUPETASYS stock value.

This comprehensive analysis dissects the company’s recent performance, strategic growth initiatives, and the key questions investors should be asking. We’ll explore the monumental Q3 2025 results, the technological edge in the AI PCB market, and the risks that management must address to secure long-term investor confidence. Whether you’re a current shareholder or considering a new position, this deep dive will equip you with the insights needed to interpret the forthcoming announcements.

ISUPETASYS Investor Relations: Event Preview & Key Details

Mark your calendars: the ISUPETASYS IR conference will take place on November 18, 2025, at 9:00 AM. The primary objective is to transparently communicate the company’s financial health, operational strategy, and future outlook to enhance corporate value. The agenda will cover a review of the blockbuster ISUPETASYS Q3 2025 performance, a detailed explanation of key management initiatives, and a crucial Q&A session where analysts and investors can probe deeper.

This IR event is a pivotal moment for ISUPETASYS to articulate its vision and solidify its role as a core supplier in the AI era. The market will be listening intently for reassurances on growth sustainability and risk mitigation.

Fundamental Analysis: AI Boom Fuels Record Performance

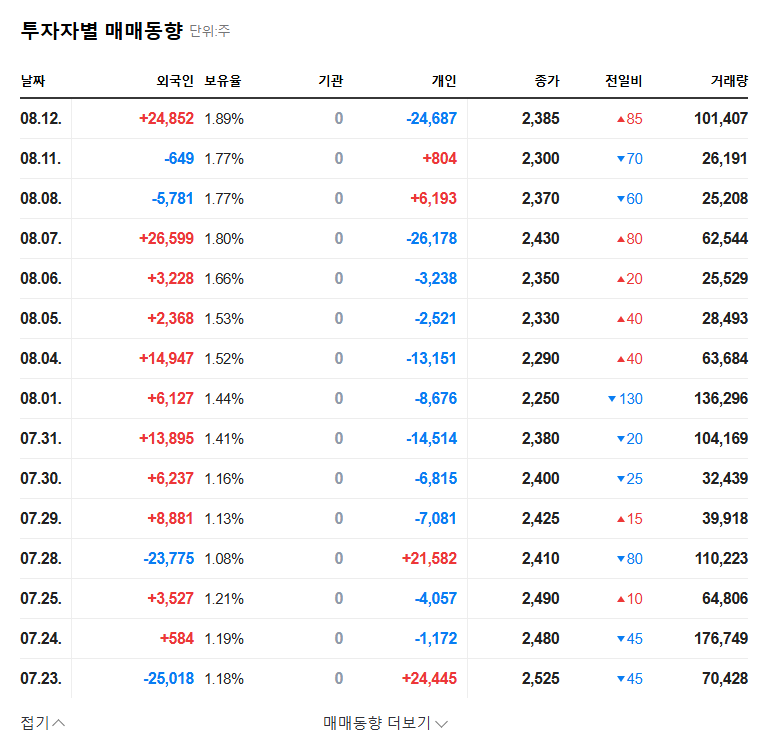

The explosive demand from the AI and data center sectors has directly translated into staggering financial results for ISUPETASYS. The company’s ability to capitalize on this trend is evident in its latest financial disclosures, which set a high bar of expectation for the upcoming IR.

Stellar Q3 2025 Financial Highlights

- •Record Revenue: Revenue surged by 29% year-over-year, reaching 790 billion KRW.

- •Explosive Profitability: Operating profit skyrocketed an incredible 94% year-over-year to 148.2 billion KRW.

- •Strategic Drivers: This performance was fueled by a strategic shift towards high-value-added products and deepening partnerships with global technology giants.

Securing Future Growth Engines

ISUPETASYS is not resting on its laurels. The company has laid out an aggressive investment plan to maintain its competitive edge in the demanding AI PCB market. This includes a planned CAPEX of 400 billion KRW between 2025 and 2028, dedicated to expanding production capacity and advancing R&D in next-generation technologies like 800G Data Center Networking and specialized AI Accelerator PCBs. For more background on industry trends, you can review our deep dive into the PCB industry.

Key Risks & Investor Questions for the IR

Despite the impressive growth, astute investors must consider the potential risks. The upcoming ISUPETASYS Investor Relations event is the perfect forum for management to address these concerns head-on. Transparency here will be key to sustaining long-term market confidence.

- •Foreign Exchange Volatility: The company has significant exposure to USD, JPY, and CNH. As noted in their Official Disclosure, a 5% change in exchange rates could materially impact earnings. Investors will expect a clear hedging strategy.

- •Customer Concentration: A single major customer accounts for approximately 42% of total sales. While this reflects a strong relationship, it also presents a concentration risk. The market will be looking for updates on customer diversification efforts.

- •Competitive Landscape: How does ISUPETASYS plan to maintain its technological lead against emerging competitors in the high-stakes AI PCB market?

Conclusion: A Defining Moment for ISUPETASYS Stock

ISUPETASYS is operating from a position of strength, powered by a favorable macroeconomic environment and superb execution. The company has improved its financial health, secured future growth drivers, and posted results that have rightfully captured the market’s attention. This investor relations conference is an opportunity to transform that attention into unshakable confidence.

If management can deliver a clear, convincing narrative that addresses key risks while powerfully communicating its long-term vision for the AI era, the investment appeal of ISUPETASYS could be significantly enhanced. Investors should watch the event closely, as the details presented and the answers given during the Q&A will likely set the tone for the stock’s performance in the months to come.