The upcoming TFE Co., Ltd. Q3 2025 IR is a pivotal event for investors navigating the dynamic semiconductor industry. As a key player with unique technological capabilities, TFE Co., Ltd. (KRX: 425420) is poised at the intersection of market recovery and next-generation tech demands. This conference is more than a simple earnings report; it’s a critical window into the company’s future growth trajectory, financial health, and overall investment appeal.

In this comprehensive analysis, we will provide a detailed preview of the key IR topics, dissect TFE’s fundamental strengths, evaluate potential market impacts, and present an actionable strategy for making informed investment decisions. Join us as we explore the strategic positioning of TFE Co., Ltd. and its outlook for sustained growth.

Event Snapshot: The TFE Co., Ltd. Q3 2025 Investor Conference

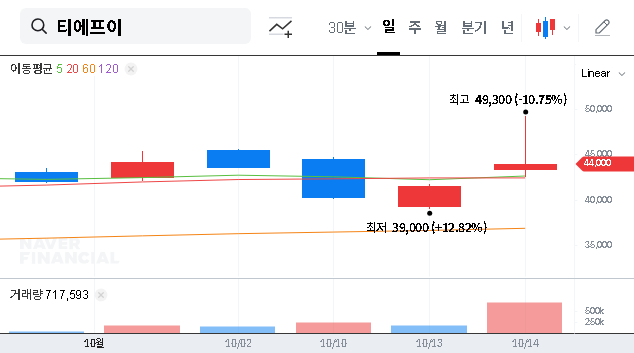

TFE Co., Ltd. has officially scheduled its Investor Relations (IR) conference to discuss third-quarter performance. The event is set for November 18, 2025, at 09:00 AM KST. The primary objective is to enhance investor understanding by presenting a thorough review of the Q3 2025 management performance, followed by an interactive Q&A session. This forum provides direct access to management’s perspective on both recent achievements and future strategies. The official disclosure for this event can be viewed here: Official Disclosure.

Fundamental Analysis: Why TFE Stands Out

TFE Co., Ltd. has carved a unique niche as a total solution provider for essential semiconductor testing components. The company designs, develops, and sells Change Over Kits (COK), Test Boards, and Test Sockets. Crucially, it is the only domestic company in Korea capable of supplying all three core components, giving it a significant competitive advantage and a diversified client base across memory and system semiconductor markets.

TFE’s ability to offer an integrated ‘total solution’ for the semiconductor test process is a key differentiator, reducing supply chain complexity for its clients and creating a strong economic moat.

Key Business & Financial Highlights (Q3 2025 YTD)

- •Robust Revenue Growth: Cumulative revenue reached KRW 74,293 million, a noteworthy increase year-on-year. This growth is propelled by the broader semiconductor market recovery and, more specifically, by surging demand in high-performance memory (like HBM) and Advanced Package testing, driven by the AI revolution. The export ratio has also climbed to 27.5%, indicating successful global market penetration.

- •Sound Financial Structure: The company boasts a stable balance sheet with assets of KRW 148,211 million against liabilities of KRW 59,168 million. While the recent issuance of convertible bonds increased liabilities, it simultaneously bolstered the company’s capital, providing essential resources for future R&D and capacity expansion projects.

- •Commitment to Innovation: TFE maintains an impressive R&D investment ratio of 8.27% of sales. This capital is funneled into developing next-generation solutions for high-performance memory (DDR5, LPDDR6, GDDR7) and complex Advanced Packages, ensuring the company remains at the forefront of technological advancement.

- •Strategic Market Alignment: The company is perfectly aligned with macro trends. As AI, autonomous vehicles, and IoT devices demand more powerful and efficient chips, the need for sophisticated semiconductor test solutions escalates. TFE is directly capitalizing on this secular growth trend.

Investment Impact: What to Expect from the IR Event

The TFE Co., Ltd. Q3 2025 IR is expected to be a significant market catalyst. Investor sentiment and the company’s stock price could see short-term volatility based on the details revealed. Here are the potential scenarios:

Potential Positive Catalysts

If Q3 results outperform market consensus or if management announces major new client acquisitions or technological breakthroughs in the Advanced Package segment, it could trigger a strong upward movement in the stock price. A confident and clear roadmap from the leadership team regarding future growth and risk management will also bolster investor trust.

Potential Negative Factors

Conversely, if earnings fall short of expectations or if guidance for Q4 is conservative, it could lead to a temporary downturn. Inadequate answers regarding the management of exchange rate risks (USD/JPY fluctuations) or competitive pressures could also dampen investor enthusiasm.

Investor Action Plan: Key Watch Points for the TFE IR

To make a well-informed decision, investors should focus on the following key areas during the conference call. Consider reviewing broader semiconductor market trends from an authoritative source like Bloomberg Technology for context.

- •Detailed Earnings Breakdown: Look beyond the headline numbers. Analyze revenue and profit margins by segment.

- •Forward-Looking Guidance: Pay close attention to the outlook for Q4 2025 and the preliminary forecast for 2026.

- •Growth Segment Progress: Seek specific updates on high-performance memory and Advanced Package projects.

- •Risk Mitigation Plans: How is the company addressing currency volatility and competition?

- •R&D Roadmap: What are the next major technological milestones and commercialization timelines?

Overall Investment Outlook: Cautiously Optimistic. TFE Co., Ltd. is a technologically robust company in a high-growth sector. Its consistent R&D spending and unique market position provide a solid foundation for future success. This IR is a crucial opportunity for the company to validate its growth narrative. A long-term investment perspective, based on a thorough analysis of the IR announcements, is the recommended approach for any TFE stock analysis.