BNK Financial Group Inc. is poised for a pivotal moment as it prepares to host its 2025 Shareholder Roundtable on November 21, 2025. In an era of significant financial market volatility and macroeconomic uncertainty, this event represents a crucial opportunity for investors to gain direct insight into the company’s strategic direction. This comprehensive analysis will delve into the group’s recent performance, the external challenges it faces, and what stakeholders should watch for during this important investor relations event. We will explore the core investment value and future outlook for BNK Financial Group Inc. to provide a clear roadmap for current and prospective shareholders.

The upcoming Shareholder Roundtable is more than a standard meeting; it’s a critical juncture for BNK Financial Group Inc. to rebuild investor confidence and articulate a clear, compelling vision for sustainable growth in a rapidly evolving digital finance landscape.

Event Overview: The 2025 Shareholder Roundtable

Scheduled for 10:00 AM on November 21, 2025, the roundtable is designed to foster direct and transparent communication. The primary goal is to address key management issues, present forward-looking strategies, and engage in a live Q&A session with investors. This direct dialogue is essential for clarifying the company’s position on profitability, risk management, and digital innovation, ultimately helping to shape market perception of BNK Financial Group Inc.’s investment value.

Financial Health Check: H1 2025 Fundamentals Analysis

A thorough examination of BNK Financial Group Inc.’s first-half 2025 performance reveals a mixed but stable picture. While the group demonstrates robust risk management and capital adequacy, profitability remains a key area requiring strategic attention.

Key Performance Indicators

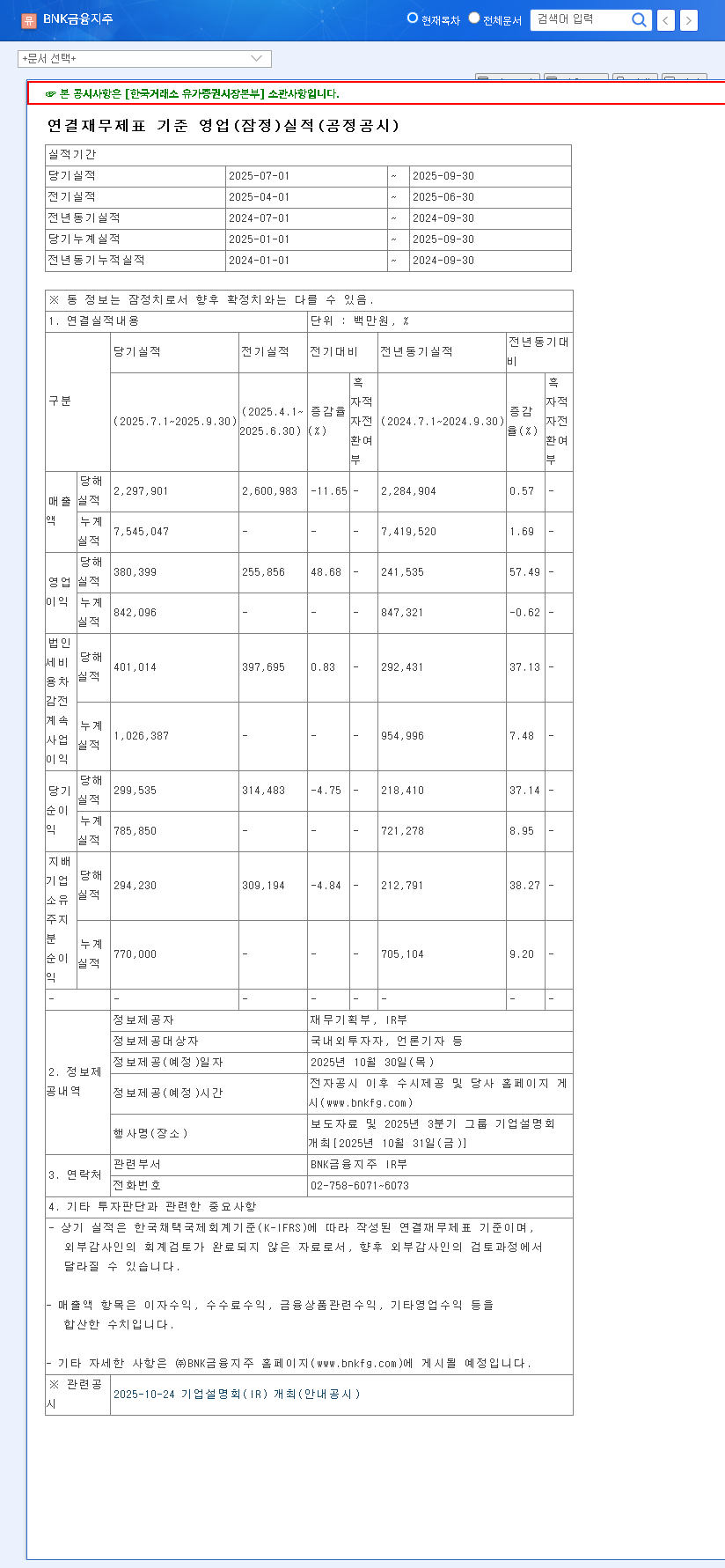

- •Asset Growth: Total assets grew by 2.7% to KRW 181.56 trillion, signaling consistent external expansion.

- •Profitability Concerns: Net profit saw a 3.4% year-over-year decrease to KRW 475.8 billion. While Busan Bank showed positive results, declines at Gyeongnam Bank and BNK Capital impacted overall earnings. Improving ROA (0.63%) and ROE (8.97%) is a top priority.

- •Asset Soundness: Risk management appears strong, with a non-performing loan ratio of 1.62% and a delinquency ratio of 1.39%, indicating a healthy loan portfolio.

- •Capital Adequacy: The group maintains a stable capital structure, with a CET1 ratio of 12.56%, comfortably above regulatory requirements. This solid foundation is crucial for navigating economic uncertainty. For further details, investors can review the Official Disclosure (DART).

Navigating Market Headwinds and Competition

BNK Financial Group Inc. operates within a complex environment characterized by global economic shifts and domestic competitive pressures. The ongoing US-China trade tensions and geopolitical instability, as discussed by sources like the World Bank, could dampen global growth and affect the group’s overseas ventures. Domestically, while there are hopes for a consumption recovery, interest rate volatility remains a significant factor that directly influences the Net Interest Margin (NIM).

Furthermore, the rise of FinTech disruptors and the convergence of financial services are intensifying competition. To thrive, BNK must accelerate its digital transformation, innovate its service models, and secure a competitive edge in both its home region and expanding metropolitan markets. To learn more about this sector, you can read our guide on how to analyze modern banking stocks.

Investor Outlook: Potential Scenarios Post-Roundtable

The market’s reaction will hinge on the substance and clarity of the strategies presented. The event could be a major catalyst or a source of increased uncertainty.

Potential Upside: Building Trust and Vision

A positive outcome would involve a transparent presentation of concrete plans to tackle profitability challenges, especially at Gyeongnam Bank and BNK Capital. If management effectively communicates a clear roadmap for digital transformation, ESG integration, and new growth engines, it could significantly boost investor confidence and lead to a positive re-rating of the stock.

Potential Risks: Heightened Uncertainty

Conversely, if the plans presented are vague or fail to address core concerns, investor disappointment could lead to negative pressure on the stock price. An overemphasis on external macroeconomic challenges without presenting robust mitigation strategies could also dampen sentiment and highlight perceived vulnerabilities.

Action Plan: What Investors Should Watch For

For investors evaluating BNK Financial Group Inc., the roundtable is a key data point. Pay close attention to the specifics of their future strategy.

- •Profitability Roadmap: Look for detailed strategies to expand non-interest income and improve the performance of underperforming subsidiaries.

- •Digital Competitiveness: Assess the commitment to and investment in technology to compete with FinTechs and deliver innovative customer experiences.

- •Risk Management Philosophy: Understand their approach to managing risks associated with the regional economy and global macroeconomic shifts.

- •Shareholder Value Commitment: Note any announcements regarding share buybacks, dividend policies, or other initiatives aimed at enhancing shareholder returns.

Ultimately, this Shareholder Roundtable will be a defining moment. It provides a platform for management to demonstrate its capability to navigate challenges and unlock the long-term investment value of BNK Financial Group Inc. Investors should listen closely to re-evaluate their positions based on the strength and credibility of the vision presented.