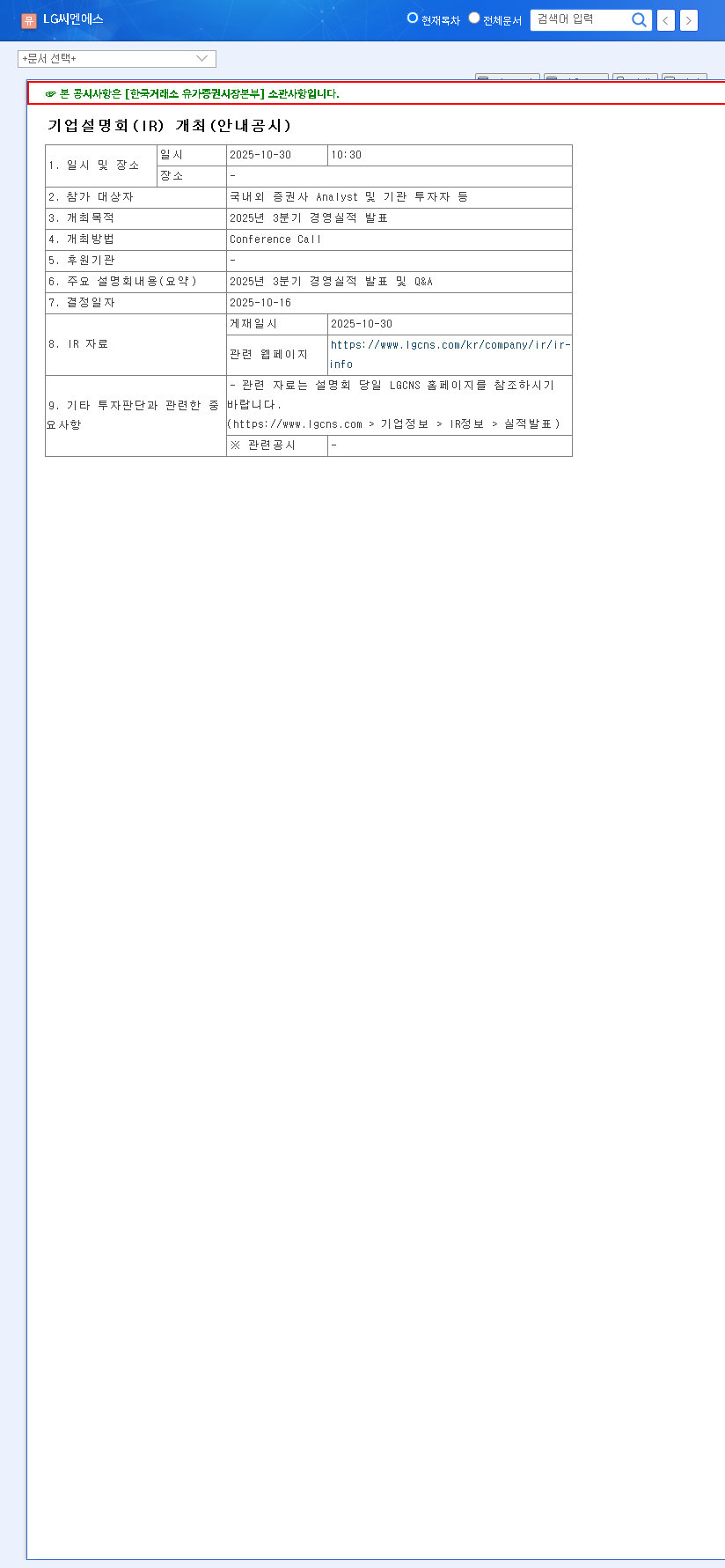

The upcoming LG CNS Q3 2025 IR, scheduled for October 30, 2025, represents a pivotal moment for investors tracking one of South Korea’s leading IT service providers. This event is more than just a financial report; it’s a critical window into the company’s operational health, strategic direction, and future growth prospects. For savvy investors, understanding the potential outcomes and preparing a clear action plan is essential to navigate the expected market volatility and make informed decisions regarding their LG CNS investment strategy.

This comprehensive guide provides a deep-dive analysis of the event, exploring potential market reactions, key metrics to watch, and crucial questions that will define the narrative for LG CNS’s stock performance in the months to come.

Who is LG CNS? A Leader in Digital Transformation

Before delving into the IR specifics, it’s important to contextualize LG CNS’s position in the IT services industry in South Korea. As a subsidiary of the LG Corporation, LG CNS has established itself as a powerhouse in digital transformation (DX). The company provides a wide array of services, including cloud computing, artificial intelligence (AI) and big data analytics, smart factory solutions, and enterprise IT system integration. Its client base spans various sectors, from finance and manufacturing to public services, making its performance an indicator of broader corporate IT spending trends.

An Investor Relations event is the company’s opportunity to control its own narrative. For investors, it’s the opportunity to read between the lines and verify that narrative against the hard data.

Analyzing the Potential Impact of the LG CNS Q3 2025 IR

The market’s reaction to the LG CNS Q3 2025 IR will hinge on the variance between the reported results and prevailing analyst expectations. While precise consensus estimates are often difficult to obtain for non-listed or recently listed giants, we can analyze potential scenarios.

The Bull Case: Exceeding Expectations

A positive surge in LG CNS’s stock price could be triggered by several factors. Investors should watch for announcements that outperform market sentiment.

- •Robust Cloud & AI Growth: Higher-than-expected revenue or margin expansion in high-growth segments like cloud services and AI-powered solutions.

- •Major Contract Wins: Disclosure of new, large-scale digital transformation projects with major domestic or international clients.

- •Improved Profitability: Effective cost management leading to better-than-forecasted operating margins, signaling operational efficiency.

- •Strong Forward Guidance: A confident and optimistic outlook for Q4 2025 and early 2026 would significantly boost investor confidence.

The Bear Case: Falling Short

Conversely, a negative market reaction could stem from disappointing results or a cautious outlook. Key triggers for a stock decline include:

- •Revenue Miss: Failure to meet revenue expectations, possibly due to project delays or a slowdown in corporate IT spending.

- •Margin Compression: Increased competition or rising labor costs eating into profitability and squeezing margins.

- •Weak Guidance: A conservative or uncertain forecast for future quarters, citing macroeconomic headwinds or industry challenges.

- •Underperformance in Key Segments: A notable slowdown in a previously strong division, such as smart logistics or financial IT.

Investor Action Plan: How to Prepare

A proactive approach is crucial. Rather than reacting to headlines, investors should conduct their due diligence before, during, and after the LG CNS earnings call.

1. Pre-IR Research and Benchmarking

Gather all available information. Start with the company’s official filings. The primary source for financial data can be found in the Official Disclosure (DART). Additionally, seek out analyst reports and market commentary from high-authority financial news sources like Bloomberg or Reuters to establish a baseline for market expectations.

2. Focus on the Q&A Session

The prepared remarks are important, but the unscripted Q&A session often reveals the most valuable insights. Listen closely to management’s tone and specificity when answering questions about future strategy, competitive threats, and capital allocation. This is where you can gauge their confidence and transparency.

3. Post-IR Analysis

After the event, compare the actual results to your benchmarked expectations. Read post-earnings analysis from multiple sources to understand the broader market reaction. Consider how the new information affects the long-term LG CNS stock analysis and whether it aligns with your investment thesis. For more context, you can review our Deep Dive into South Korea’s IT Services Market.

Conclusion: A Prudent and Informed Approach

The LG CNS Q3 2025 IR is more than a single data point; it’s a comprehensive update that can cause significant short-term stock price movement. However, for the long-term investor, its true value lies in the details about the company’s strategic direction and operational execution. By conducting thorough due diligence and analyzing the results within the broader context of the industry, investors can move beyond short-term noise and make decisions grounded in a solid, fundamental understanding of LG CNS’s investment potential.