The reported TKG Huchems Yasojima acquisition has sent ripples through the specialty chemicals sector, marking a potentially transformative moment for TKG Huchems Co.,Ltd. (069260). This ambitious move, pursued in partnership with IMM Private Equity, could either catapult the company into a new growth trajectory or introduce significant financial and operational risks. For investors, understanding the nuances of this deal is paramount.

This comprehensive analysis delves into the strategic rationale behind the bid, TKG Huchems’ robust financial standing, and the potential impact on its corporate value and stock performance. We’ll unpack the opportunities and threats to provide investors with the deep insights needed for informed decision-making.

The Bid for Yasojima: What We Know

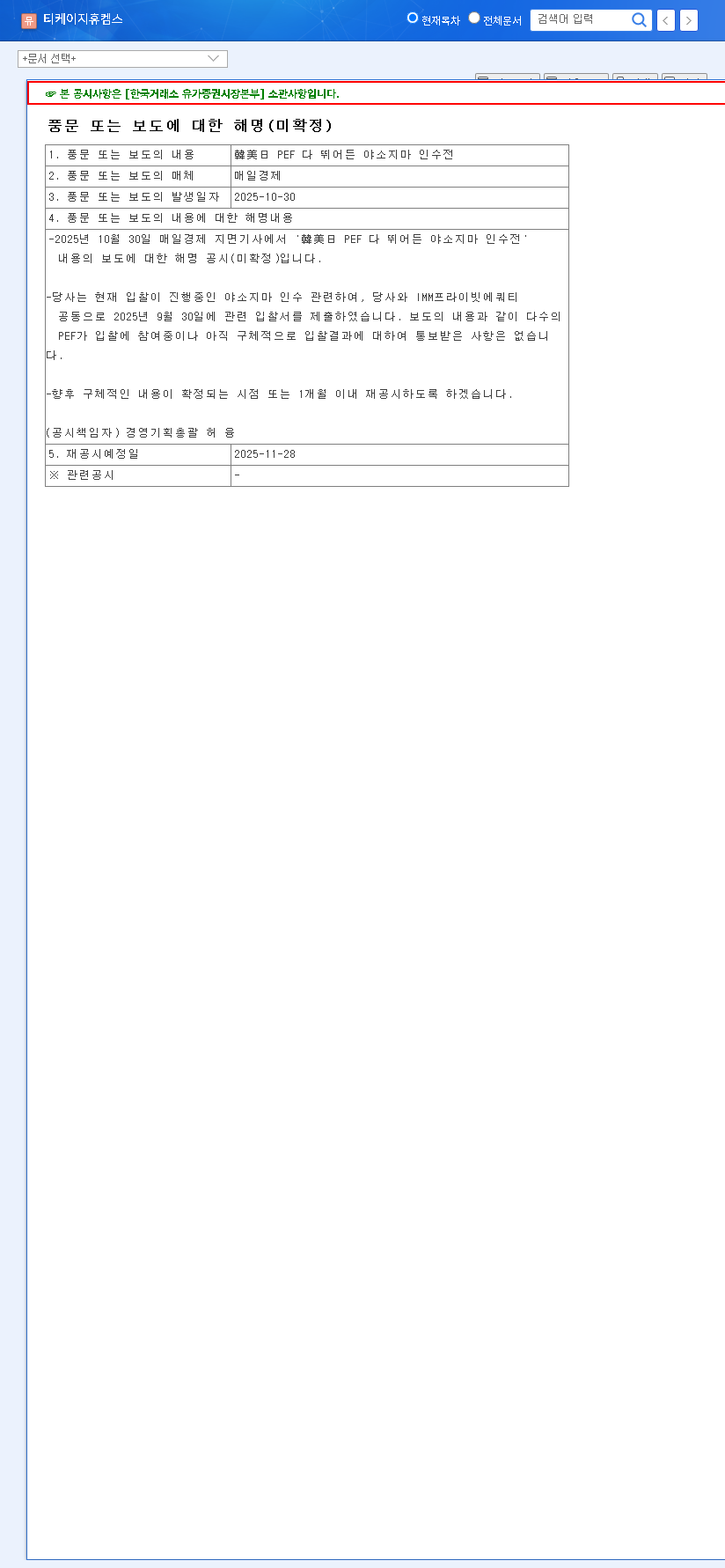

On October 30, 2025, reports emerged confirming that TKG Huchems, in a consortium with IMM Private Equity, submitted a bid for Yasojima on September 30, 2025. While the bidding process is ongoing and the final outcome remains uncertain, the company’s intent is clear. The market awaits further details, with a crucial re-disclosure scheduled for November 28, 2025. This development was confirmed in an Official Disclosure via the DART system, which serves as the primary source for this information.

While the TKG Huchems Yasojima acquisition presents a compelling growth narrative, investors must balance this potential with a clear-eyed assessment of the financial and operational risks involved in such a large-scale integration.

Analyzing TKG Huchems’ Financial Foundation

Before any major acquisition, a company’s underlying financial health is critical. TKG Huchems stands on a solid foundation as a fine chemical manufacturer. Its primary revenue streams come from NT-series products (DNT, MNB) and NA-series products (Nitric Acid, Ammonium Nitrate), which are essential materials in industries ranging from polyurethane production to agriculture.

As of the first half of 2025, the company’s financials paint a picture of stability. With total equity of KRW 871.3 billion dwarfing total liabilities of KRW 239.4 billion, TKG Huchems maintains a very healthy balance sheet. This low leverage provides significant financial flexibility, a key advantage when pursuing a major acquisition. Although operating profit saw a year-over-year decrease, the recent completion of new production facilities is expected to enhance cost competitiveness and bolster future profitability.

The Acquisition: Opportunities vs. Risks

Potential Upside of the Yasojima Deal

- •New Growth Engine: The primary driver for the TKG Huchems Yasojima acquisition is to secure a new, long-term growth engine. Acquiring Yasojima could diversify TKG Huchems’ product portfolio and provide entry into new, high-margin markets, reducing reliance on its current core products.

- •Enhanced Corporate Value: A successful M&A of this scale signals ambition and strategic vision to the market. It can boost corporate recognition, attract new investors, and ultimately lead to a higher valuation if synergies are realized.

- •Strategic Partnership: Partnering with IMM PE distributes the immense financial burden of the acquisition, mitigating risk and preserving capital for post-merger integration and operational investments.

Inherent Risks and Considerations

- •Acquisition Uncertainty: The deal is not yet final. If the bid fails, the market’s positive expectations could evaporate, leading to negative pressure on the TKG Huchems stock price.

- •Financial Strain: Even with a partner, the acquisition will require significant capital. This could lead to increased debt, potentially straining short-term financials and impacting dividend policies.

- •Integration Challenges: Post-merger integration is notoriously difficult. Risks include clashing corporate cultures, operational inefficiencies, and failing to achieve the projected synergies, which could ultimately destroy rather than create value.

Stock Impact (069260) & Investor Outlook

The announcement of the Yasojima bid has likely introduced a new catalyst for the TKG Huchems stock. Investor sentiment will be a key driver in the short term, hinging on news and speculation leading up to the November 28 disclosure. This trend of consolidation is common in the global chemical industry, as reported by leading financial news outlets like Reuters, as companies seek to gain a competitive edge.

Investors should adopt a strategy of cautious optimism. It is essential to monitor official communications from the company closely. For those looking to deepen their understanding of market dynamics, consider reviewing our guide on how to analyze chemical sector stocks. The long-term performance of the stock will depend entirely on the successful execution and integration of the acquisition, should the bid succeed.

Frequently Asked Questions (FAQ)

What are TKG Huchems’ primary business areas?

TKG Huchems is a fine chemical manufacturer specializing in NT-series products like DNT and MNB, and NA-series products such as Nitric Acid and Ammonium Nitrate. These form the core of its revenue.

What are the main benefits of the TKG Huchems Yasojima acquisition?

A successful acquisition could provide a significant long-term growth engine by expanding TKG Huchems’ business into new markets, enhancing overall corporate value, and improving its strategic position in the global chemical industry.

What should investors watch for regarding the 069260 analysis?

Investors should closely monitor the re-disclosure on November 28, 2025, for concrete details. Key factors for any 069260 analysis will be the final acquisition price, the financing structure, and management’s strategic plan for post-merger integration.

Disclaimer: This article is for informational purposes only and is based on publicly available information. It does not constitute financial advice. Investors should conduct their own research, and the final responsibility for investment decisions rests with the individual.