This comprehensive stock analysis offers a deep dive into the Green Cross Medical Science Corporation (GCMS) Q3 2025 earnings report, announced on November 3, 2025. While the company showcases long-term potential in key growth sectors, the latest preliminary figures reveal short-term challenges that investors must carefully consider. We will dissect the financial data, evaluate the health of its core business segments, and outline a strategic investment strategy for both cautious and forward-looking investors.

The report, which initially drew significant market attention, showed a decline in key metrics from the previous quarter, raising questions about immediate stock price trajectory. Our analysis moves beyond the surface-level numbers to explore the fundamental value and future catalysts for Green Cross Medical Science Corporation.

GCMS Q3 2025 Earnings: The Official Numbers

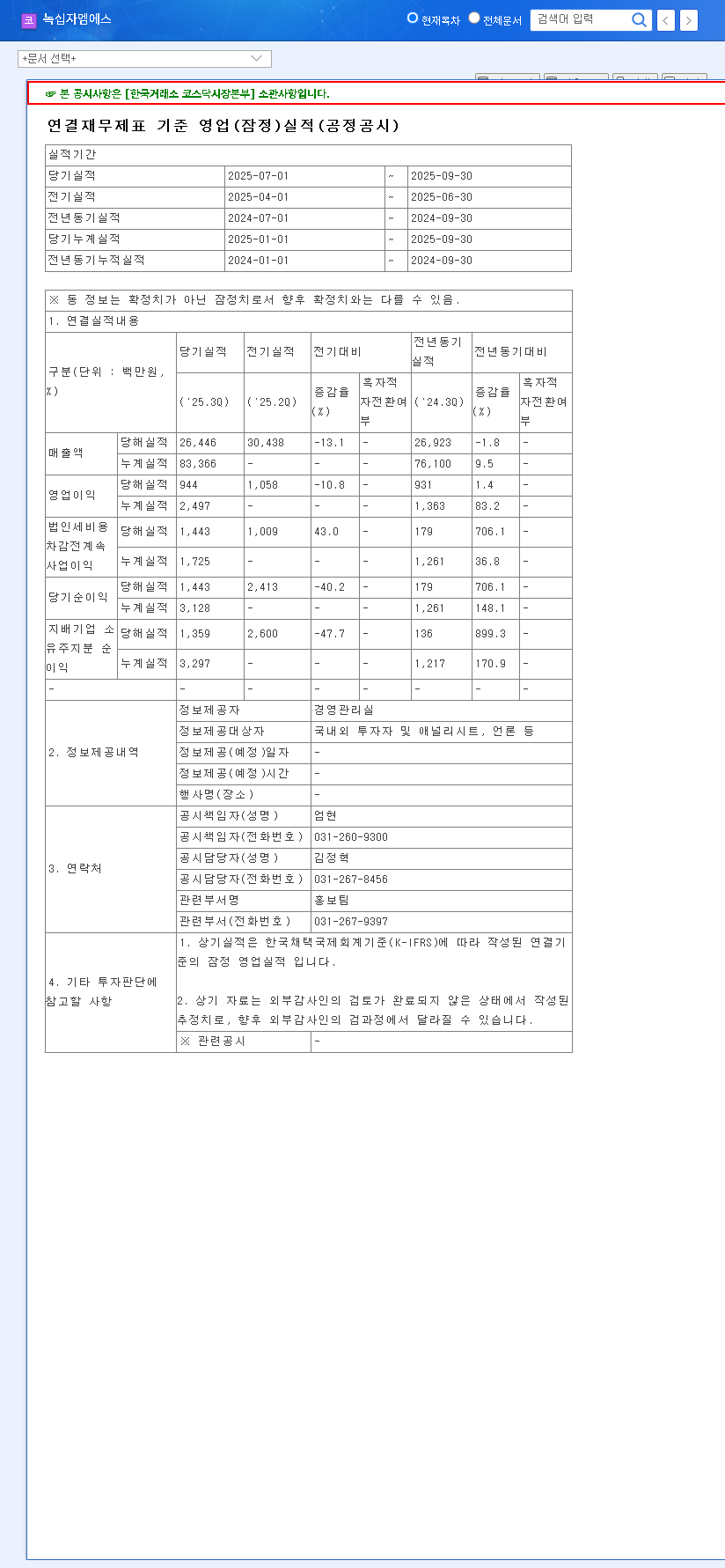

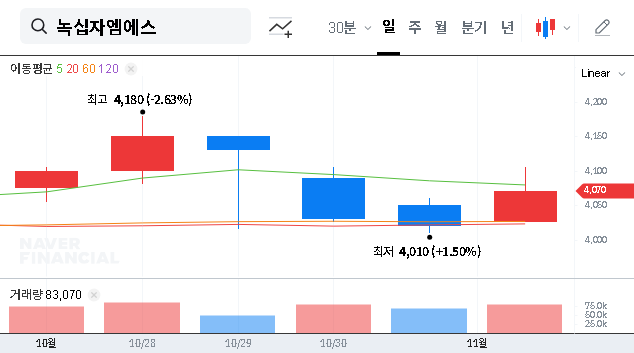

On November 3, 2025, Green Cross Medical Science Corporation released its preliminary consolidated financial results for the third quarter. The official disclosure can be found on DART, Korea’s electronic disclosure system. (Source: Official Disclosure).

The key performance indicators were as follows:

- •Revenue: KRW 26.4 billion

- •Operating Profit: KRW 0.9 billion

- •Net Profit: KRW 1.4 billion

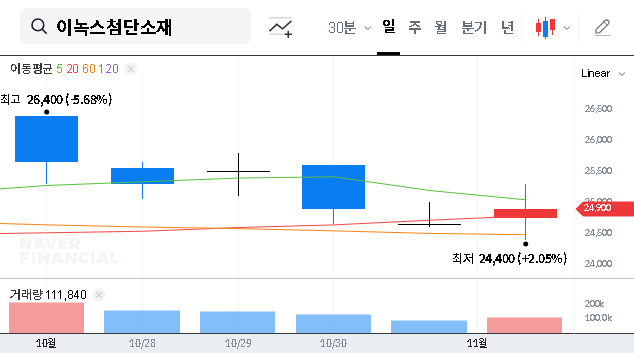

These results represent a noticeable downturn from Q2 2025, where revenue stood at KRW 30.4 billion and operating profit was KRW 1.1 billion. Compared to the same period last year (Q3 2024), revenue was nearly flat, and operating profit showed no improvement, signaling a potential stall in profitability momentum and falling short of market expectations.

Fundamental Analysis: A Mixed Financial Picture

Profitability vs. Financial Health

While the Q3 results are concerning, the company’s half-year 2025 performance painted a more optimistic picture. Half-year revenue grew an impressive 23.2% year-over-year, and operating profit surged by 258.1%. This suggests that underlying profitability improvements were taking hold earlier in the year. However, this progress is now overshadowed by the recent quarterly slowdown.

A deeper look into the balance sheet reveals a critical area for investor caution: financial health. As of mid-2025, total liabilities had increased by 32.9% from the previous year-end, driven by a rise in short-term borrowings. This pushed the company’s debt-to-equity ratio up to 130.56% from 102.57%. A higher ratio indicates greater financial leverage and risk, meaning the company relies more on debt to finance its assets, which can become a burden in a rising interest rate environment.

Deep Dive into Core Business Segments

The company’s future hinges on the performance of its primary business units. Here’s a breakdown of the key drivers for Green Cross Medical Science Corporation:

- •Diagnostic Reagent Business: This is the company’s largest segment (58.9% of revenue), which saw robust 21.0% year-over-year growth. The shift towards multi-diagnosis platforms and global partnerships presents a significant long-term opportunity beyond the COVID-19 era.

- •Hemodialysis Solution Business: Accounting for 27.7% of revenue, this division grew by 17.4%. With a rising number of domestic patients requiring treatment, this segment offers a stable and predictable revenue stream, further supported by planned capacity expansion.

- •Blood Glucose Business: While revenue in this area saw a slight dip, the growing global diabetes patient population provides a massive potential market. Achieving IVDR certification is a crucial step towards unlocking overseas expansion.

- •Research & Development (R&D): Ongoing investment in new diagnostic technologies, including Point-of-Care Testing (POCT), is vital for securing a competitive edge and fueling future growth pipelines.

Stock Price Outlook and Investment Strategy

The core challenge for investors is to balance the disappointing short-term profitability against the valid long-term growth potential of the company’s diagnostic and hemodialysis divisions.

Short-Term & Long-Term Impact

In the short term, the underwhelming GCMS Q3 2025 earnings are expected to create downward pressure on the stock price. The market may react negatively to the slowdown in profitability and the low 3.4% operating margin. However, the mid- to long-term outlook is buoyed by positive factors, including the strength of the diagnostic reagent business. Conversely, the deteriorating financial health and a high dependency on a few key customers remain significant risks that could temper future appreciation.

Investor Action Plan

A prudent investment strategy requires a nuanced approach:

- •For Short-Term Investors: A cautious, wait-and-see stance is recommended. Consider a staggered buying approach, initiating positions only after seeing evidence of financial stabilization (e.g., debt reduction) and a return to profit growth in subsequent quarterly reports.

- •For Long-Term Investors: The underlying growth story remains intact. However, it is essential to monitor key performance indicators closely. Investors should watch for progress in new product development, successful overseas expansion, and proactive measures to improve the balance sheet. For more on this, see our guide to analyzing biotech stocks.

Frequently Asked Questions (FAQ)

What were Green Cross Medical Science Corporation’s key Q3 2025 results?

For Q3 2025, Green Cross Medical Science Corporation reported revenue of KRW 26.4 billion and an operating profit of KRW 0.9 billion. This marked a decrease from the prior quarter, signaling a slowdown in performance.

What is the short-term stock price outlook for GCMS?

The short-term outlook is cautious. The decline in operating profit is likely to disappoint investors and could lead to downward pressure on the stock price until the company demonstrates a clear path back to improved profitability.

What are the company’s main long-term growth drivers?

The primary long-term growth drivers are the robust diagnostic reagent business, which is expanding globally, and the stable, in-demand hemodialysis solution business. Continued success in R&D is also critical for future growth.

What are the key risks for investors?

The main investment risks include the company’s rising debt levels (financial health), a high reliance on a concentrated number of customers, and potential negative impacts from macroeconomic factors like fluctuating interest rates.