The recent news surrounding the LG Energy Solution stock has been dominated by a significant move from its parent company, LG Chem. The announcement of an off-market sale of a 2.46% stake has sent ripples through the investment community, raising critical questions. Why did LG Chem reduce its holding, and what does this mean for the future of LGES stock price and its long-term strategy? This comprehensive analysis unpacks the details behind the stake sale, evaluates the potential impact, and provides actionable insights for current and prospective investors.

The Event: LG Chem Reduces Its Stake

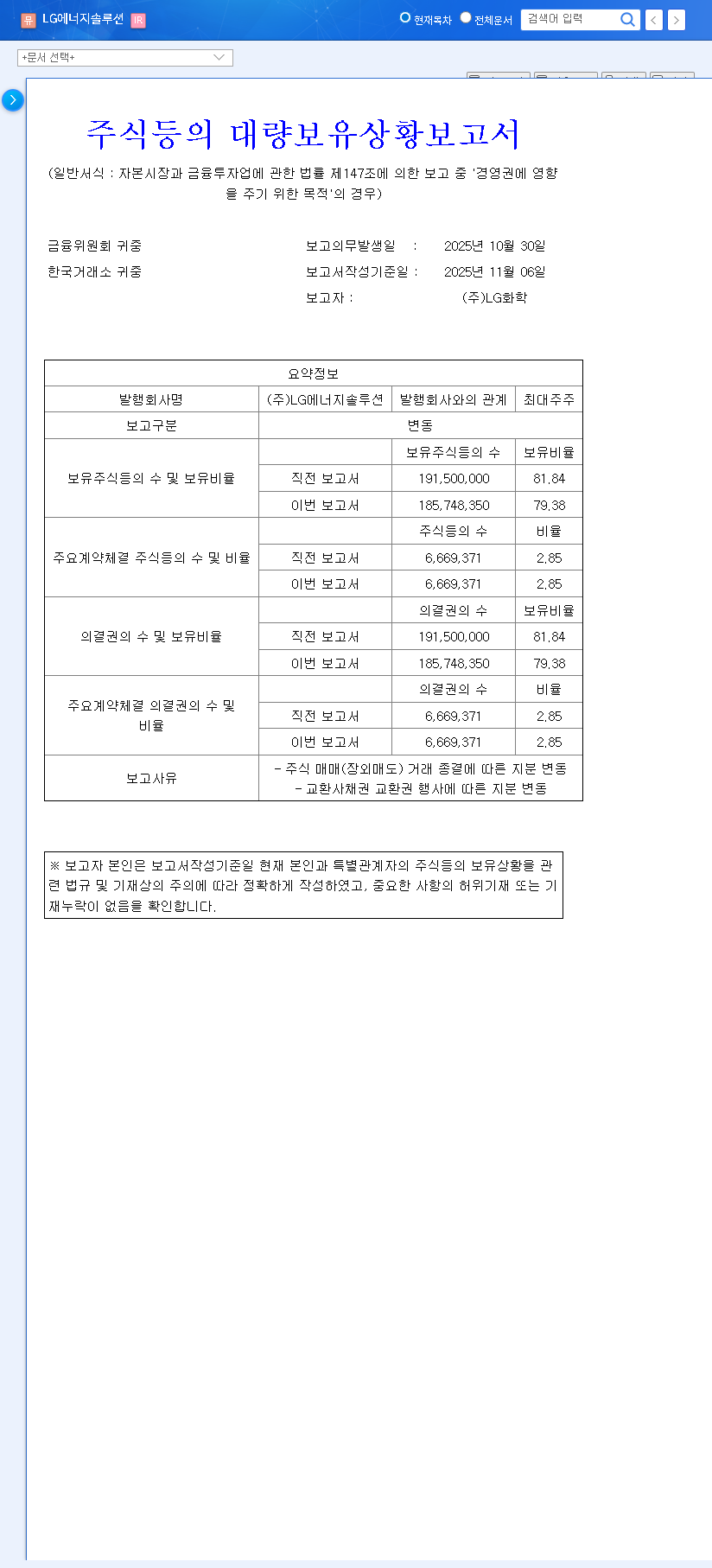

On October 30, 2025, LG Chem executed an off-market sale of 5,750,000 common shares in LG Energy Solution. According to the Official Disclosure (Source: DART), this transaction reduced LG Chem’s ownership from 81.84% to 79.38%. While a 2.46% change may seem minor, a block sale of this magnitude is a significant event that warrants close examination. The stated reasons included general stock trading and the exercise of exchange rights for exchangeable bonds, but the underlying strategic motivations are what truly matter to investors.

Despite the sale, LG Chem retains a commanding 79.38% stake, ensuring that management control over LG Energy Solution remains firmly intact and undisputed.

Analyzing the ‘Why’: Potential Motives Behind the Sale

While LG Chem’s official holding purpose remains ‘influence over management,’ such a large divestment is typically driven by strategic financial goals. Here are the most likely reasons behind the decision:

- •Capital for New Investments: The proceeds could be earmarked to fund LG Chem’s expansion into other high-growth sectors, such as advanced battery materials (e.g., cathodes, anodes), which are critical for the entire EV supply chain.

- •Strengthening Financial Health: The sale provides a significant cash infusion that can be used to pay down debt, improve the balance sheet, and enhance LG Chem’s overall financial resilience in a volatile economic climate.

- •Strategic Portfolio Realignment: This move might be part of a broader strategy by the LG Group to rebalance its portfolio, unlocking value from its mature assets to reinvest in next-generation technologies and businesses.

It’s crucial to understand this was likely a strategic financial maneuver by the parent company rather than a signal of lost confidence in LG Energy Solution’s future.

Impact Analysis for LG Energy Solution Investors

Short-Term Market Reaction and Stock Volatility

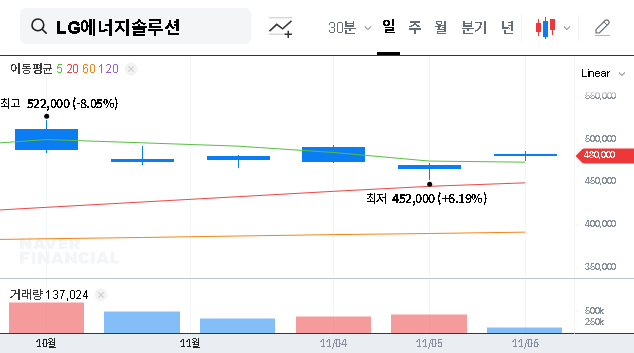

In the short term, a large block sale like this can create what’s known as ‘stock overhang.’ This puts downward pressure on the LGES stock price as the market works to absorb the new supply of shares. Investor sentiment may temporarily weaken, leading to increased price volatility. However, such movements are often disconnected from the company’s underlying operational performance. For a detailed view of market trends, investors often consult authoritative sources like Bloomberg’s market analysis.

Long-Term Outlook: Fundamentals Remain Strong

Looking beyond the immediate market noise, the fundamental case for an LG Energy Solution investment remains compelling. The company is a global leader in the rapidly expanding electric vehicle (EV) battery market. Key strengths include:

- •Technological Leadership: LGES continues to innovate in battery chemistry and design, securing major contracts with leading automakers worldwide.

- •Aggressive Investment: With plans for KRW 5.8 trillion in new investments and a significant increase in R&D spending, the company is positioning itself for future dominance.

- •Market Growth: The global shift to electrification provides a powerful tailwind. You can learn more in our deep dive into the EV battery market.

Therefore, this stake sale does not alter the company’s long-term growth trajectory or its competitive position in the industry.

Actionable Investment Strategy & Outlook

How should investors react to this development concerning their LG Energy Solution stock position?

For the Cautious Short-Term Trader

A prudent approach is to monitor the stock for signs of stabilization. Watch for the trading volume to normalize as the sold shares are absorbed by the market. Increased volatility presents risks, but also potential entry points for those with a high risk tolerance. A wait-and-see approach is advisable until the near-term selling pressure subsides.

For the Fundamental Long-Term Investor

For those focused on the company’s intrinsic value, any price dip resulting from this sale could represent a strategic buying opportunity. The long-term growth story of the EV and battery storage markets is unchanged. This event is external to LGES’s operations and, if it leads to a lower stock price, may offer a more attractive entry point for accumulating a long-term position.

Conclusion: A Strategic Move, Not a Red Flag

In conclusion, LG Chem’s sale of a minority stake in LG Energy Solution appears to be a calculated financial decision to unlock capital for its own strategic priorities. It does not compromise control over LGES or signal a lack of faith in its future. While the LG Energy Solution stock may experience short-term turbulence, the company’s robust fundamentals, market leadership, and the secular growth trend of electrification remain firmly in place. Investors should view this event through a strategic lens, separating short-term market sentiment from long-term business potential.