A recent disclosure regarding an ILJIN HOLDINGS stake change has captured the attention of the market. On October 15, 2025, a report detailed a shift in the equity held by representative reporter Hur Jung-suk and related parties. While the change appears minor on the surface, such moves by key insiders can be powerful signals about a company’s future trajectory and stability. This analysis delves deep into the disclosure, exploring the potential market impact and providing a strategic guide for current and prospective investors.

When major shareholders adjust their positions, even slightly, it warrants a closer look. Is it a routine financial decision, or does it signal a deeper strategic shift within ILJIN HOLDINGS? Understanding the context is key to smart investment.

Deconstructing the Disclosure: What Exactly Happened?

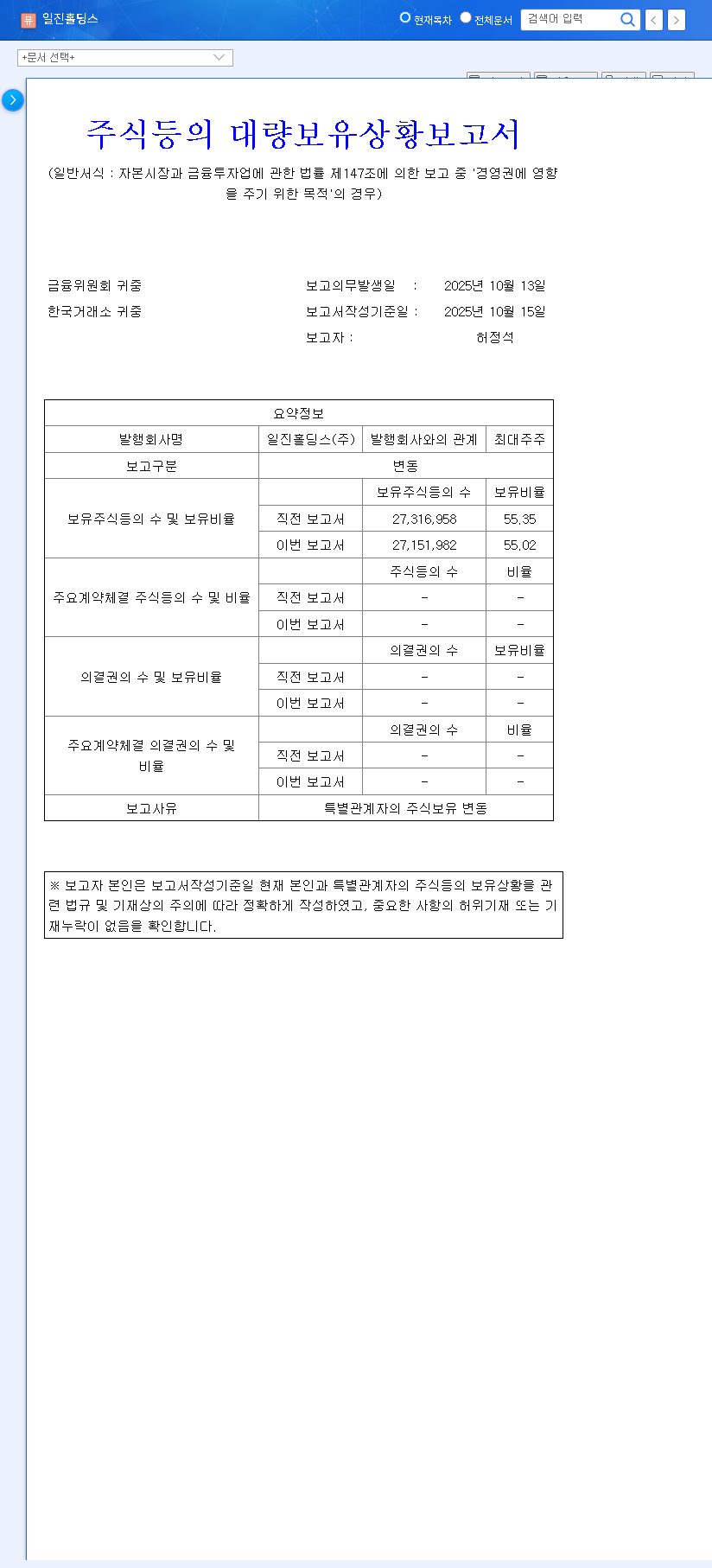

The catalyst for this analysis is the official ‘Report on the Status of Large Shareholdings’ filed on October 15, 2025. This document is a mandatory disclosure in many jurisdictions, designed to provide transparency about the ownership structure of publicly traded companies. Here are the crucial details from the report:

- •Reporting Party: Hur Jung-suk & Related Parties

- •Holding Purpose: Influence over management

- •Shareholding Before Change: 55.35%

- •Shareholding After Change: 55.02%

- •Net Change: -0.33%

- •Reason: Open-market sale by a related party (Hur Se-kyung)

The sales were executed in several transactions between September and October 2025. The full details can be verified in the Official Disclosure (Source: DART). While the 0.33% reduction is not substantial enough to threaten control, the nature of an open-market sale by an insider often prompts investor questions.

Analyzing the Potential Market Impact

Investors must consider both the immediate sentiment-driven effects and the longer-term strategic implications of this ILJIN HOLDINGS stake change.

Short-Term: Investor Sentiment and Stock Volatility

In the short term, any sale by a major shareholder can be perceived negatively. The market may interpret it as a lack of confidence, leading to temporary downward pressure on the stock price. This can create uncertainty and a ‘wait-and-see’ attitude among retail and institutional investors. However, the impact here may be limited because the total holding remains robustly above the 50% threshold, ensuring stable management control. The relatively small volume of shares sold is unlikely to cause significant, sustained selling pressure.

Mid-to-Long-Term: Management Stability and Future Strategy

From a long-term perspective, a 55.02% controlling stake is exceptionally strong, meaning management stability is not at risk from this specific transaction. The more critical question is whether this sale is an isolated event or the beginning of a trend. Continuous, future sales could signal a more significant strategic shift, a plan for succession, or a move to raise capital for other ventures. Investors should monitor subsequent corporate disclosures carefully for any signs of a developing pattern.

A Strategic Guide for Informed Investors

Given the limited information, a proactive approach is necessary. Drawing conclusions from a single data point is risky. To build a comprehensive view of the ILJIN HOLDINGS shareholder report and its implications, investors should take the following steps:

- •Analyze Company Fundamentals: Look beyond this single report. Dive into ILJIN HOLDINGS’ recent quarterly earnings reports, balance sheets, and cash flow statements. Strong financial health can easily outweigh the negative sentiment from a minor insider sale.

- •Review Analyst and Brokerage Reports: Assess the consensus view from market analysts. Their research often includes insights into management strategy and industry trends that can provide crucial context. Reputable sources like Bloomberg or Reuters offer extensive market data.

- •Monitor IR and Management Communications: Pay close attention to the company’s investor relations channel. Any official statements, interviews, or presentations from management following this disclosure can offer direct insight into their perspective and future plans.

- •Contextualize the Sale: Remember that insider sales can occur for many reasons unrelated to company performance, such as for personal liquidity, tax planning, or portfolio diversification. Without further information, it’s prudent not to assume the worst.

Conclusion: Prudence Over Panic

In summary, the recent ILJIN HOLDINGS stake change is a noteworthy event that calls for vigilance, not alarm. The sale is minor and does not compromise the controlling majority’s firm grip on management. For investors, the wisest course of action is to treat this as a prompt for deeper due diligence. By focusing on the company’s fundamental performance and monitoring for further ownership changes, you can make an informed decision based on a complete picture rather than a single, ambiguous signal.