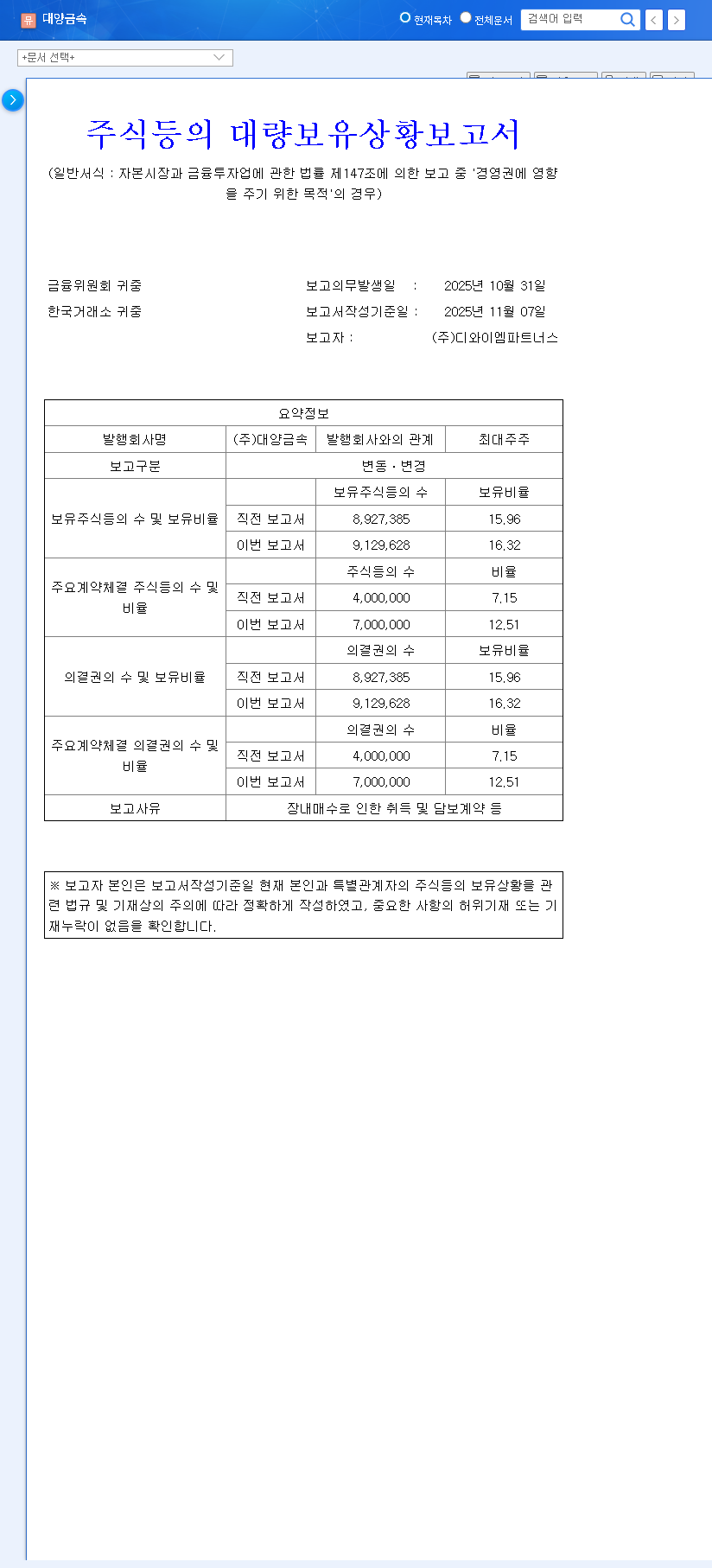

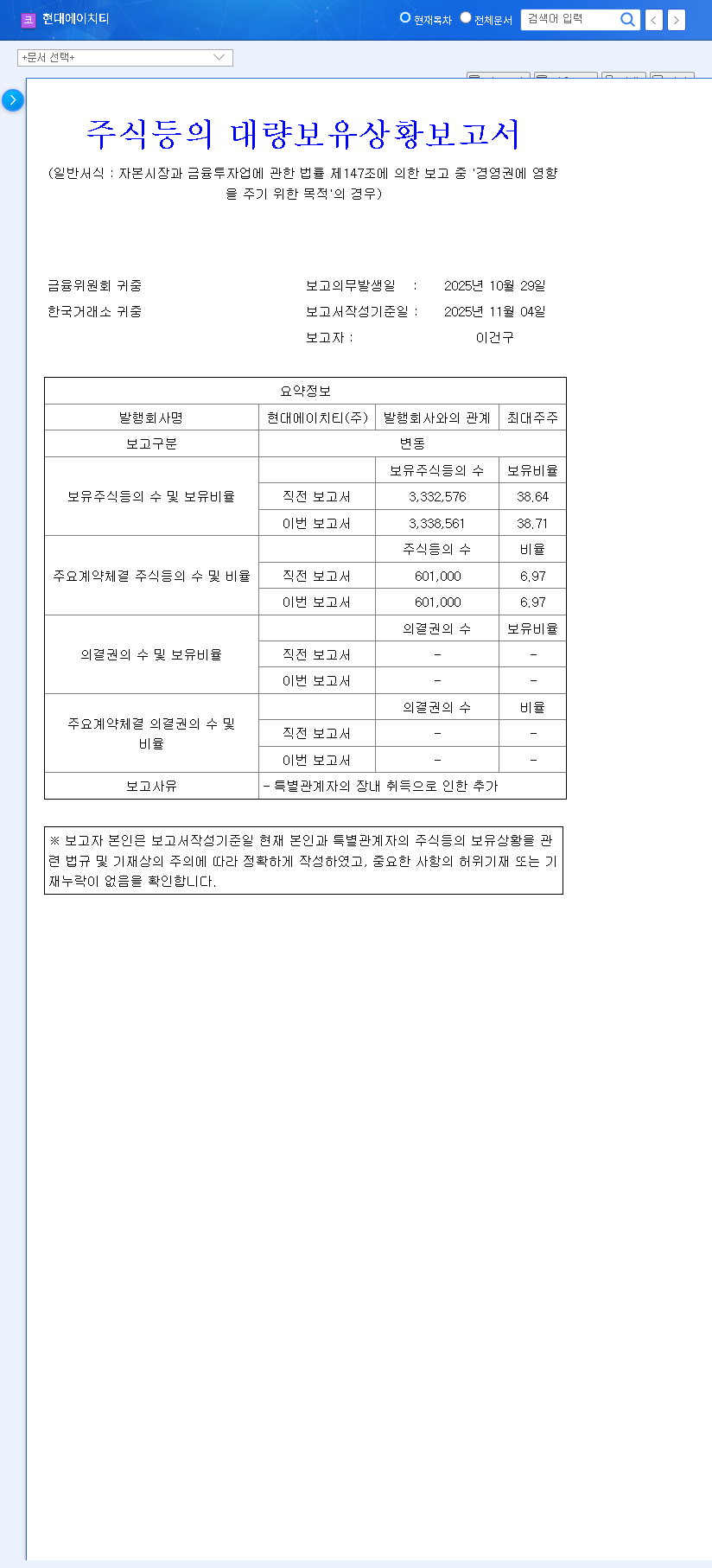

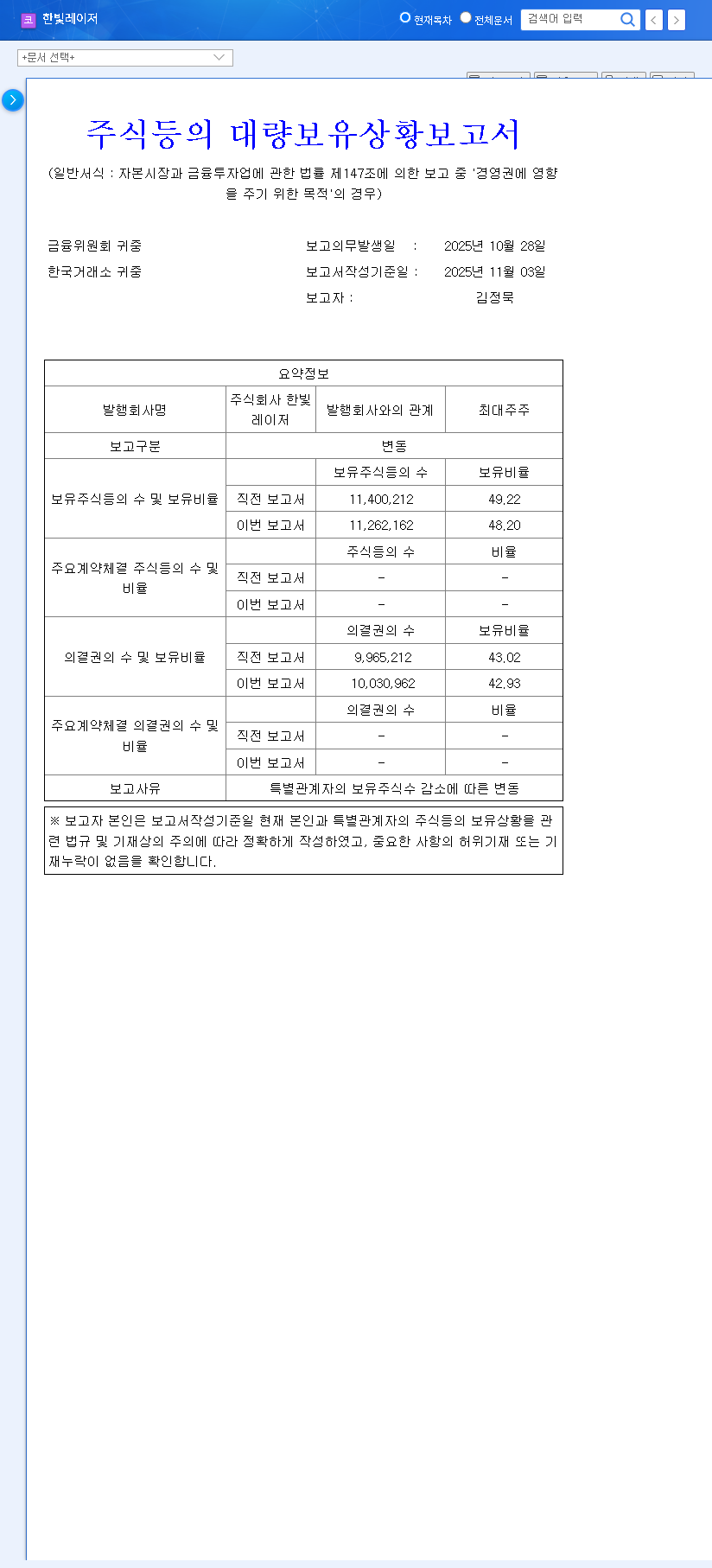

The latest disclosure from HC BoKwang Industry Co.,Ltd (보광산업) has sent mixed signals across the market. On one hand, the company’s largest shareholder, HC Homesenta, has increased its stake—a move typically seen as a vote of confidence. On the other, the company is grappling with a severe financial downturn, marked by plummeting revenue and a worrying shift to operating losses in the first half of 2025. This raises a critical question for investors: Is this a sign of a coming turnaround or a minor positive in a sea of red flags?

This comprehensive investment analysis delves into the nuances of HC BoKwang Industry’s current situation. We’ll dissect the shareholder filing, scrutinize the alarming financial performance, and explore the profound impact of the ongoing construction market downturn to provide a clear, actionable outlook on the company’s stock and future prospects.

The Shareholder Stake Increase: A Closer Look

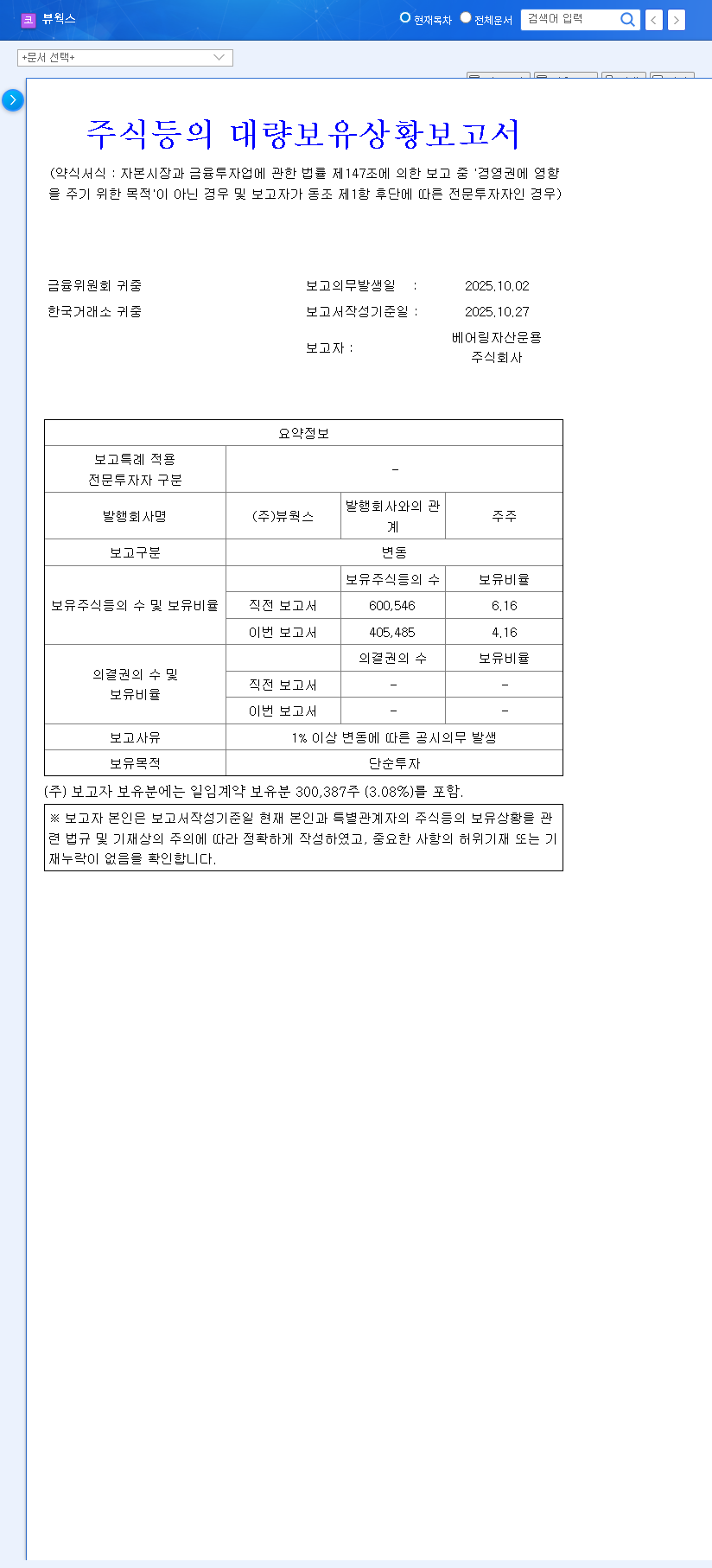

On November 13, 2025, a public disclosure revealed a change in the equity held by HC BoKwang Industry’s primary shareholder, HC Homesenta. According to the Official Disclosure (DART), the stake saw a minor increase.

Key Details of the Change

- •Previous Stake: 68.48%

- •New Stake: 68.58%

- •Net Change: +0.10%

This adjustment was the result of on-market purchases, inheritance, and modifications to stock collateral agreements. Typically, an increase in a major shareholder’s position is a bullish signal, suggesting insider confidence and a commitment to long-term management stability. However, the fractional nature of this increase mutes its impact, especially when viewed against the company’s daunting financial performance.

Analyzing the HC BoKwang Industry Financial Crisis: H1 2025

The positive sentiment from the shareholder news is immediately overshadowed by the stark reality of HC BoKwang Industry’s first-half performance in 2025. The numbers paint a picture of a company under immense pressure, primarily due to a severe contraction in its core markets.

The fundamentals are deeply concerning. A near 50% drop in revenue and a swing to a significant operating loss indicate that the company’s core business model is currently unprofitable amidst the market headwinds.

Performance Breakdown

- •Revenue Collapse: The company reported revenue of just KRW 18.428 billion, a staggering 47.66% decrease compared to the previous year.

- •Operating Loss: HC BoKwang Industry transitioned from profit to an operating loss of KRW 1.681 billion.

- •Aggregates Business Crisis: The aggregates segment, a core pillar, saw its utilization rate plummet to a mere 16.49%, contributing a massive KRW 2.608 billion operating loss.

- •Worsening Debt Profile: The debt-to-equity ratio rose to 79.79%, and a KRW 20 billion convertible bond issuance looms, adding significant pressure to its balance sheet and short-term liquidity.

The Root Cause: A Crippling Construction Market Downturn

The struggles of HC BoKwang Industry are not happening in a vacuum. They are a direct symptom of a broader, systemic construction market downturn. Factors such as high interest rates, inflated material costs, and stalled real estate projects have decimated demand for essential construction materials like ready-mixed concrete, aggregates, and asphalt—the company’s primary products.

As major construction projects are delayed or cancelled, demand for these materials evaporates, leaving suppliers with idle factories and mounting fixed costs. This is evident in HC BoKwang’s extremely low production capacity utilization across all segments. For a deeper understanding of market dynamics, investors can review analyses from authoritative sources like global economic reports from Reuters.

Investment Outlook and Strategy

Given the circumstances, what is the prudent investment strategy for the HC BoKwang Industry stock? While the shareholder confidence is a minor positive, it is far outweighed by severe fundamental weaknesses.

Key Factors to Monitor

- •Macroeconomic Recovery: The company’s fate is inextricably linked to a rebound in the construction sector. Watch for signs of interest rate stabilization and renewed project funding.

- •Management’s Turnaround Plan: The company must demonstrate aggressive and effective strategies for cost reduction, business restructuring, and profitability enhancement.

- •Debt Management: How the company handles the financial burden from its debt and the KRW 20 billion convertible bond will be critical for its survival and recovery.

In conclusion, a highly conservative and cautious approach is warranted. The shareholder stake change is not enough to offset the deep-seated operational and financial challenges. Investors should remain on the sidelines, closely monitoring for tangible signs of improvement in both the company’s performance and the wider market. To learn more about evaluating companies in this sector, you can read our guide on how to analyze construction sector stocks.