SECERN AI Co., Ltd. (stock code: 340810) has made a significant financial move, announcing the issuance of a ₩3 billion private placement SECERN AI convertible bond. This news has sent ripples through the investment community, presenting both a potential catalyst for growth and the looming risk of stock dilution. For current and prospective shareholders, understanding the nuances of this financial instrument is critical for making informed decisions. Is this a sign of strength or a necessary measure that could harm shareholder value down the line?

This comprehensive analysis will dissect the SECERN AI convertible bond issuance from every angle. We’ll explore the strategic reasons behind the move, break down the potential impact on the SECERN AI stock price, and provide a clear action plan for investors navigating this pivotal event.

Unpacking the Details of the ₩3 Billion Issuance

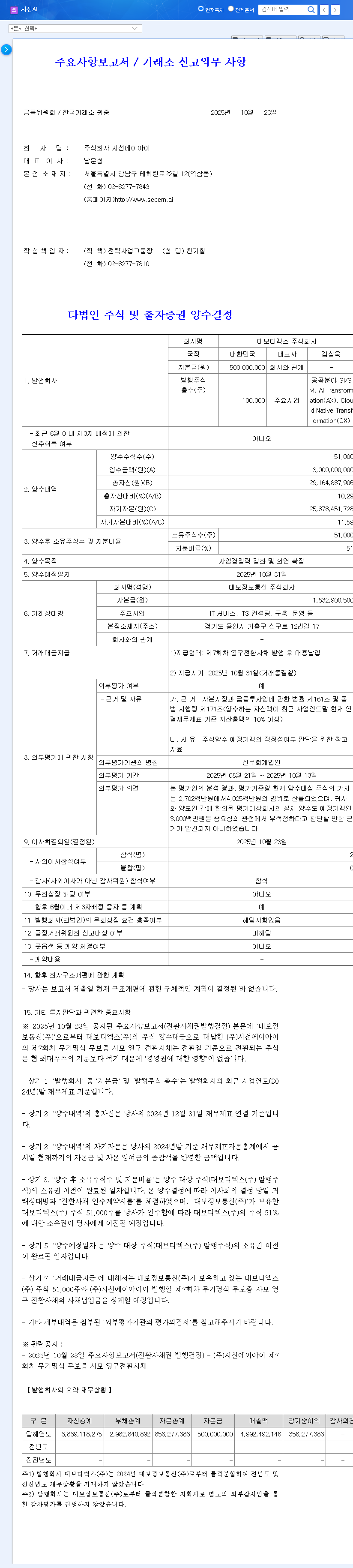

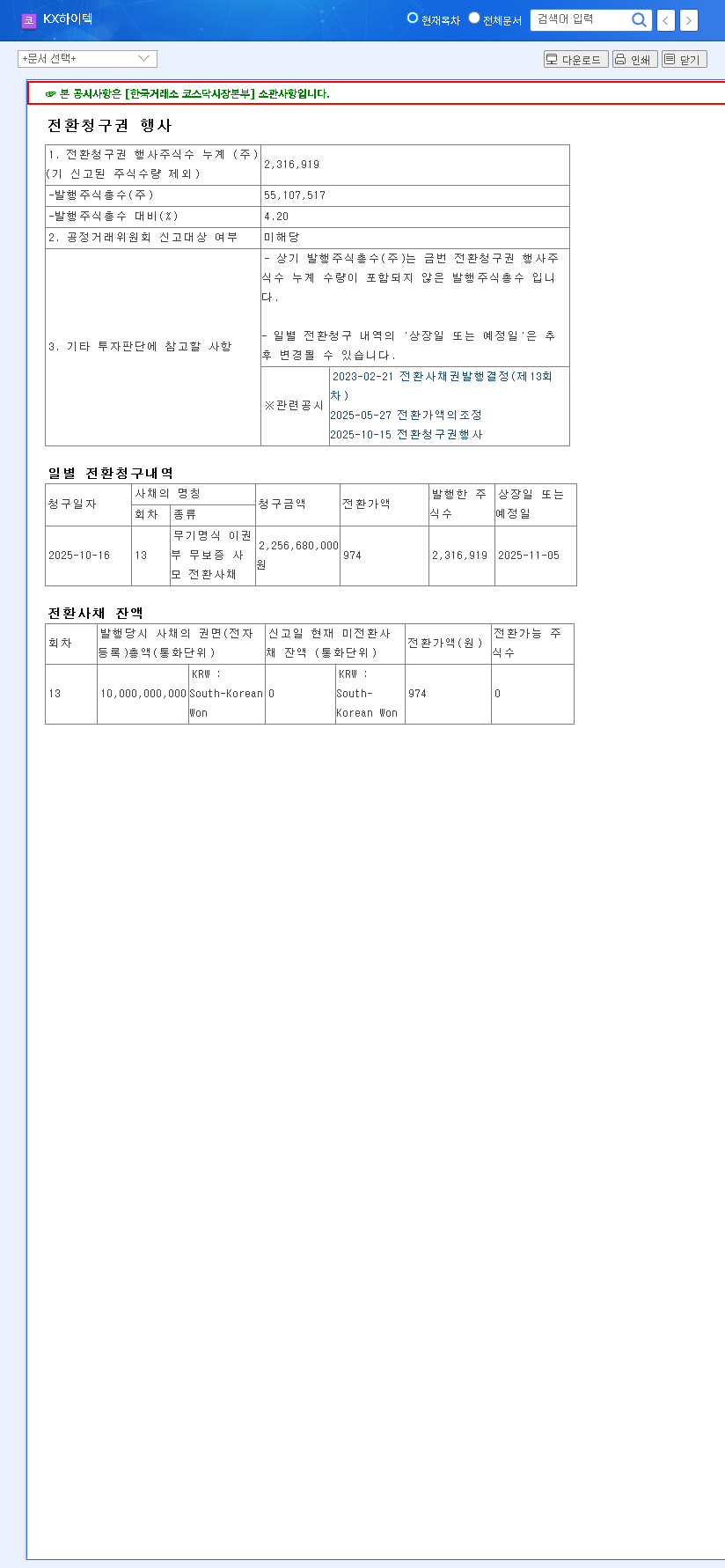

On October 23, 2025, SECERN AI formally announced its decision through a public filing. A convertible bond is a hybrid security that acts like a loan but gives the bondholder the option to convert their debt into a predefined number of the company’s common stock shares. For a full breakdown, you can review the Official Disclosure (DART Source). Here are the crucial terms of this deal:

- •Total Issuance Amount: ₩3 billion, a significant capital injection for the company.

- •Issuance Method: A private placement to specific investors, including DAEBO Information & Communications.

- •Conversion Price: ₩3,648 per share. This is the price at which bondholders can convert their debt into equity.

- •Coupon Rate: 0%. SECERN AI will not pay regular interest on this debt, preserving cash flow.

- •Yield to Maturity: 3%. If the bonds are not converted, bondholders will receive a 3% annualized return at maturity.

- •Conversion Period: Begins one year after issuance, from October 31, 2026.

The Strategic Rationale: Why Raise Capital Now?

A company like SECERN AI doesn’t raise ₩3 billion without a clear purpose. The primary driver is to secure operating funds to fuel growth and strategic initiatives. This capital can be deployed in several high-impact areas, such as accelerating research and development in its core AI technologies, expanding into new markets, or strengthening its financial position against competitors. The 0% coupon rate is particularly advantageous, as it allows the company to access significant funds without the immediate pressure of interest payments, a major benefit for its short-term financial health.

This fundraising signals ambition. The participation of a strategic investor like DAEBO Information & Communications can be seen as a strong vote of confidence in SECERN AI’s long-term vision and technological roadmap.

Analyzing the Impact: Opportunity vs. Risk

The issuance of a SECERN AI convertible bond creates a classic duality for investors. The potential outcomes depend heavily on how effectively the company utilizes the new capital and how the market reacts.

The Bull Case: Fueling Growth and Investor Confidence

On the positive side, this ₩3 billion infusion can be a powerful growth catalyst. If used to successfully develop and launch new products, it could lead to substantial revenue growth and a higher SECERN AI stock price. The fact that an established entity like DAEBO is investing sends a strong positive signal to the market about SECERN AI’s perceived value and potential. This can attract further institutional investment and improve overall market sentiment.

The Bear Case: The Inevitable Risk of Stock Dilution

The most significant risk for existing shareholders is stock dilution. If the stock price rises above the ₩3,648 conversion price, bondholders will be incentivized to convert their debt into stock. This increases the total number of shares outstanding, which dilutes the ownership stake of each existing shareholder. For a deeper understanding of this financial concept, resources like Investopedia provide excellent explanations. Essentially, each existing share represents a smaller piece of the company pie. Furthermore, if the funds are not used efficiently, the company is left with a future debt obligation (the 3% yield to maturity) without the corresponding business growth, creating a financial drag.

An Action Plan for Smart Investors

Navigating this event requires vigilance. Investors should not react impulsively but rather adopt a strategic, monitoring approach.

- •Monitor Fund Utilization Plans: Pay close attention to company announcements, press releases, and earnings calls. Look for specific details on how the ₩3 billion will be deployed. Concrete plans for R&D or expansion are positive signs.

- •Track the Stock Price vs. Conversion Price: The ₩3,648 conversion price is now a key technical level. As the stock price approaches or surpasses this benchmark, the probability of conversion and subsequent dilution increases.

- •Re-evaluate Company Fundamentals: This event should be analyzed in the context of the company’s overall health. Continue to review financial statements and market performance. For more context, you can read our Deep Dive into SECERN AI’s Q3 Earnings.

In conclusion, the SECERN AI convertible bond issuance is a pivotal moment. While it secures vital capital for growth, it introduces a tangible risk of stock dilution. The ultimate impact will be determined by management’s execution and the market’s response, making continuous, informed monitoring the best strategy for any investor.