The HD Hyundai Heavy Industries merger with its affiliate, HD Hyundai Mipo, represents a pivotal moment for the global shipbuilding industry. A recent, crucial milestone has all but guaranteed the merger’s smooth progression: the results from the exercise of stock appraisal rights by dissenting shareholders were remarkably low. This development signals overwhelming market confidence and sets the stage for the creation of a more streamlined, competitive, and powerful entity.

This in-depth analysis unpacks the significance of this event, explores the powerful synergies expected from the merger, and evaluates the long-term shipbuilding investment opportunity. For investors looking at HD Hyundai Heavy Industries stock, understanding these dynamics is essential for making informed decisions.

A Resounding Vote of Confidence: The Stock Appraisal Rights Outcome

On November 13, 2025, the results of the stock appraisal rights exercise were officially announced. Shareholders opposing the merger had the right to sell their shares back to the company at a predetermined price. The results were telling:

- •HD Hyundai Heavy Industries: Approximately KRW 940 million (2,128 shares) were claimed.

- •HD Hyundai Mipo: Approximately KRW 710 million (3,850 shares) were claimed.

The total request of ~KRW 1.65 billion is a fraction of the KRW 1.5 trillion cap that could have potentially derailed the merger. This overwhelmingly positive outcome confirms the merger will proceed, with an effective date of December 1, 2025. The full details were released in an Official Disclosure (DART), cementing market certainty.

The negligible exercise of appraisal rights is the market’s strongest endorsement of the merger’s strategic rationale, effectively removing the final procedural hurdle and unlocking future value.

Analyzing the Post-Merger Powerhouse

The true value of the HD Hyundai Heavy Industries merger lies in the long-term synergies and strengthened market position it creates. This goes far beyond simple consolidation; it’s a strategic move to dominate the next era of shipbuilding.

Unlocking Operational and Technological Synergies

Combining operations allows for significant efficiencies. We anticipate major gains from economies of scale in procurement, streamlined R&D for next-generation eco-friendly vessels (like ammonia and hydrogen carriers), and optimized production schedules across yards. This unified approach will not only cut costs but also accelerate innovation, solidifying their leadership in high-value-added shipbuilding—a key trend highlighted by organizations like the World Shipping Council.

Building on Solid Financial Fundamentals

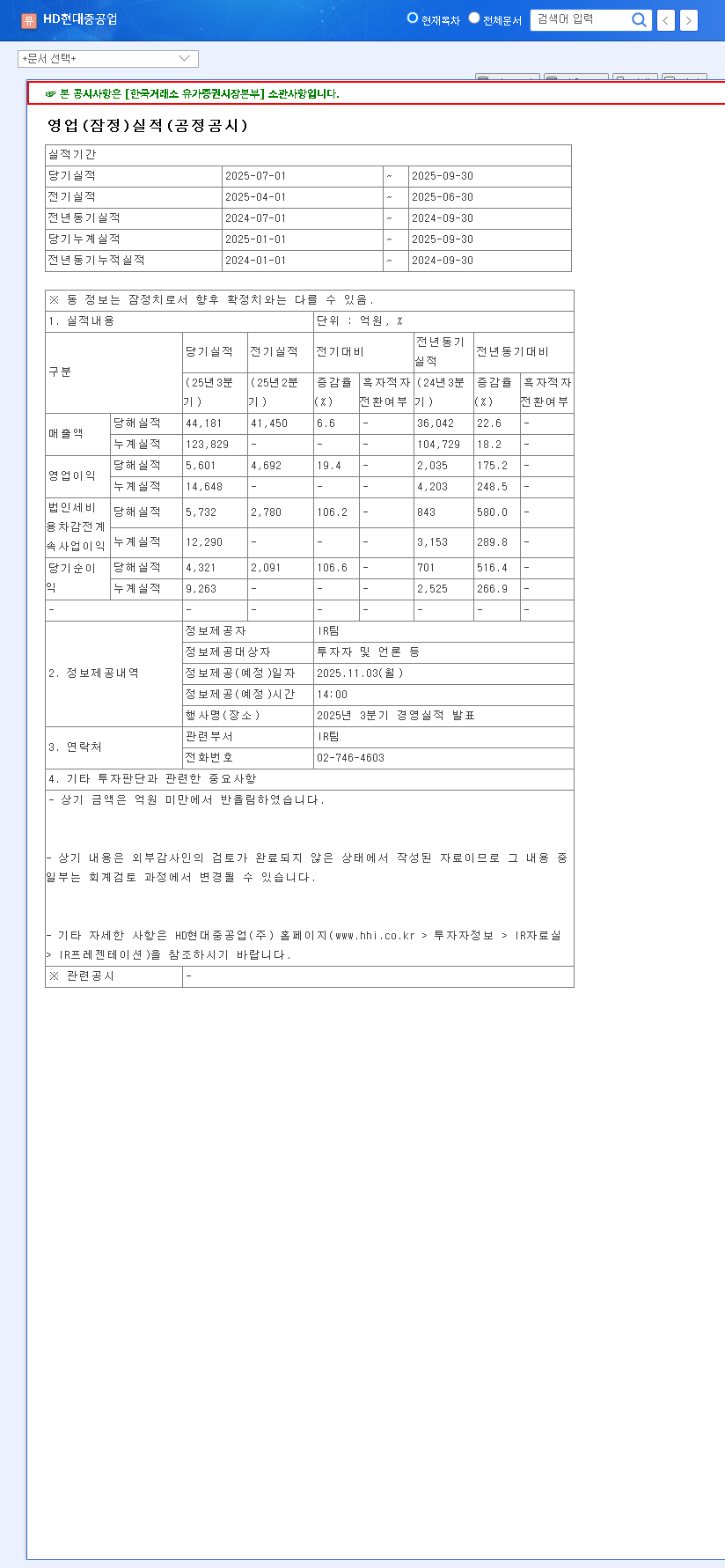

HD Hyundai Heavy Industries already boasts a strong foundation. Despite revenue fluctuations, its 2025 half-year report showed marked improvement in operating and net profit. This is driven by a focus on high-margin vessels and cost control. The company’s massive order backlog of KRW 46.34 trillion provides unparalleled revenue visibility for years to come, securing its growth trajectory. For those seeking a deeper understanding of market dynamics, consider our complete guide to investing in the shipbuilding sector.

Investment Thesis: A Clear ‘BUY’ Recommendation

The combination of a smooth merger process, strong underlying fundamentals, and significant future synergies makes a compelling case for a ‘BUY’ rating on HD Hyundai Heavy Industries stock.

Key Rationale for a ‘BUY’ Rating:

- •De-Risking Event: The successful passing of the stock appraisal rights phase removes the primary uncertainty surrounding the merger.

- •Synergy Potential: The merger is poised to unlock significant operational efficiencies and bolster competitiveness in the global market.

- •Strong Fundamentals: A robust order backlog and a leading position in the green vessel market provide a stable foundation for long-term growth.

Potential Risks to Monitor

While the outlook is positive, investors should monitor the Post-Merger Integration (PMI) process for challenges in cultural and systems alignment. Furthermore, the entire shipbuilding industry is subject to macroeconomic factors like global trade volumes, steel prices, and geopolitical risks, which could impact order flows and profitability.

Frequently Asked Questions (FAQ)

What does the HD Hyundai Heavy Industries merger mean for investors?

For investors, this merger signals the creation of a more efficient, competitive, and technologically advanced shipbuilding leader. It reduces internal competition and focuses resources on dominating high-growth areas, potentially leading to enhanced long-term shareholder value.

Why is the low exercise of stock appraisal rights so important?

A low exercise rate is a powerful indicator of shareholder approval. It shows that the vast majority of investors believe they will get more value from the merged company than from cashing out their shares. It removes a major financial and procedural obstacle, clearing the path for the merger to complete smoothly.

What are the main risks associated with this shipbuilding investment?

The primary risks include potential difficulties in the post-merger integration of two large organizations. Externally, the company is exposed to global economic slowdowns, fluctuations in raw material costs (like steel), and intense competition from other major shipbuilding nations.