The recent ANIPLUS INC. acquisition of exhibition agency Media & Art marks a pivotal moment for the animation content specialist. In a rapidly evolving content market, this strategic KRW 7 billion investment signals a clear ambition to move beyond distribution and into experiential IP monetization. While the company faces challenging financial headwinds, this move could unlock significant long-term value. This analysis will dissect the acquisition’s strategic rationale, potential synergies, financial implications, and the critical factors investors should monitor for the future of ANIPLUS INC.

We will explore how this deal fits into the broader ANIPLUS growth strategy and what it means for its extensive intellectual property portfolio, providing a comprehensive outlook for stakeholders.

The Deal: A 100% Acquisition of Media & Art

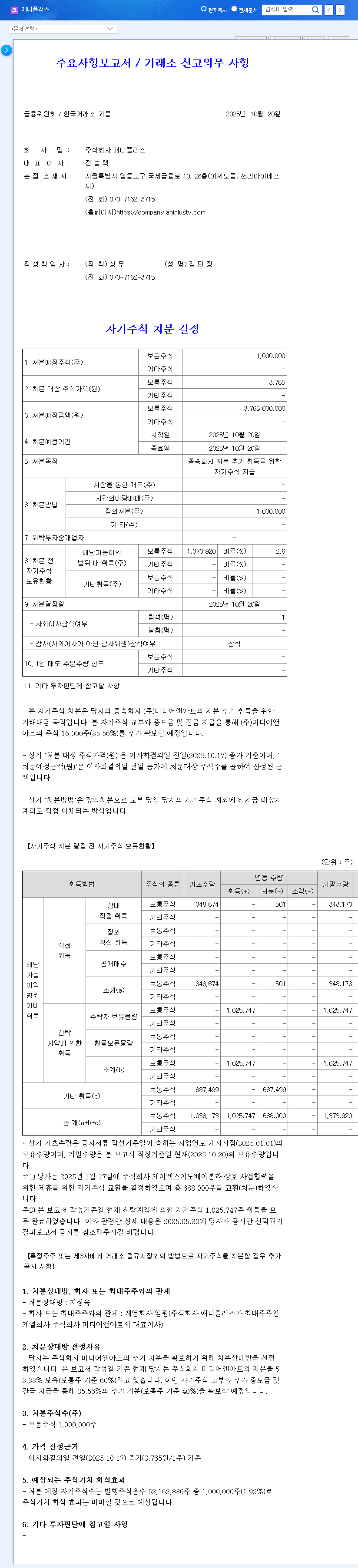

On October 30, 2025 (scheduled), ANIPLUS INC. (KRX: 310200) finalized its decision to acquire the remaining 5.65% stake in Media & Art, an agency specializing in exhibition and event management. This cash payment of KRW 7 billion elevates ANIPLUS’s ownership to 100%, transforming Media & Art into a wholly-owned subsidiary. According to the Official Disclosure, the stated objective is to “enhance corporate value through the full acquisition of the subsidiary’s shares,” paving the way for streamlined operations and a unified strategic vision.

Financial Context: Navigating a Performance Dip

This acquisition comes at a challenging time. The 2025 half-year report for ANIPLUS INC. revealed a consolidated revenue of KRW 57.98 billion (a 55.7% decrease year-on-year) and an operating profit of KRW 8.30 billion (a 66.9% decrease). This downturn is largely attributed to a slump in the core ‘content’ segment. However, a closer look shows a 28.1% increase in separate net profit, suggesting that the consolidated results were weighed down by underperformance in other subsidiaries or complex accounting adjustments.

Despite this, the company’s financial foundation remains solid. With total assets of KRW 262.33 billion against total equity of KRW 138.60 billion, the balance sheet is healthy. A significant increase in intangible assets to KRW 145.55 billion underscores a continued, aggressive investment in securing valuable IP—the very fuel for the company’s future growth engines.

While the ANIPLUS INC. acquisition presents clear short-term financial hurdles, its long-term success hinges on the company’s ability to transform its vast IP library into tangible, real-world experiences.

Strategic Analysis of the Media & Art Acquisition

Unlocking Synergy and IP Expansion

The primary benefit of this deal lies in synergy. Media & Art’s expertise in creating physical events provides ANIPLUS with the perfect vehicle for ANIPLUS IP expansion. This moves beyond simple merchandise sales into creating immersive fan experiences like pop-up stores, themed exhibitions, and character-centric events. By controlling the entire process from content licensing to physical execution, ANIPLUS can ensure quality, capture more revenue, and build deeper brand loyalty. This is a critical step in evolving from a distributor to a comprehensive entertainment powerhouse. You can learn more by reading about successful IP monetization strategies in today’s market.

Potential Risks and Macroeconomic Pressures

The KRW 7 billion cash outlay represents a notable short-term financial burden. While not critical given the company’s equity, it does reduce liquidity at a time when performance is already under scrutiny. Furthermore, the global economy currently faces challenges from rising interest rates and currency volatility. As a major licensor of Japanese animation, a weakening Korean Won against the Japanese Yen could significantly inflate content acquisition costs, squeezing profit margins. The success of the ANIPLUS INC. acquisition will partly depend on how effectively management navigates these external economic pressures.

Investor Outlook: Key Observation Points

The full acquisition of Media & Art is a forward-looking, strategic play. Its success is not guaranteed and requires flawless execution. For investors, the investment thesis is neutral for now, pending tangible results. The following points will be critical to monitor:

- •Synergy Execution: Watch for the announcement and performance of new IP-driven exhibitions and events. Are they driving meaningful revenue and fan engagement?

- •Performance Recovery: A return to growth in the core content and merchandise segments in H2 2025 and 2026 is essential to reassure the market.

- •Laftel’s Global Growth: Track the global expansion and subscriber growth of its OTT platform, Laftel, a key digital growth engine.

- •Macroeconomic Management: Monitor how the company addresses exchange rate fluctuations and rising interest costs in its financial reports.

Frequently Asked Questions

Q1: What is the primary purpose of the ANIPLUS INC. acquisition of Media & Art?

A1: The primary goals are to enhance management efficiency by securing 100% control and to execute a robust ANIPLUS IP expansion strategy by leveraging Media & Art’s event expertise to create offline, experiential content.

Q2: How will this acquisition impact ANIPLUS’s finances?

A2: It will create a short-term KRW 7 billion cash outflow, potentially straining liquidity. However, given ANIPLUS’s sound financial base, it is not expected to cause severe long-term financial deterioration.

Q3: What specific business synergies are expected?

A3: Key synergies include creating pop-up stores, special exhibitions, and fan events based on ANIPLUS’s strong animation IP. This strengthens the offline content business, creates new revenue streams, and increases overall IP value.