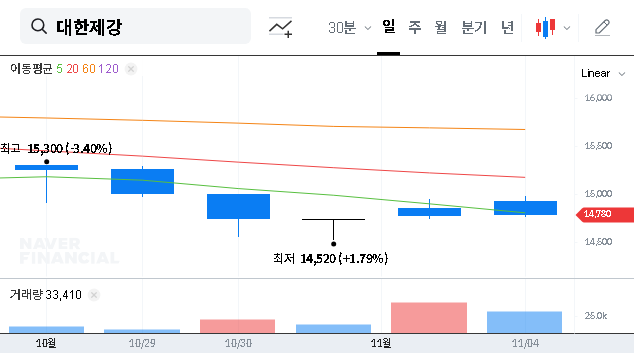

The future of MANHO ROPE & WIRE LTD (만호제강) has been cast into a new light following a significant corporate maneuver that has captured the attention of the investment community. MH Group Holdings (‘MH Group’) recently acquired over one million shares, securing a formidable 24.82% stake. This move signals a potential change in management control and a pivotal turning point for a company that has grappled with financial credibility issues and challenging macroeconomic headwinds. This analysis will explore the profound implications of the MH Group acquisition on Manho Rope & Wire’s fundamentals, market sentiment, and long-term stock value.

For investors seeking to re-evaluate their position on MANHO ROPE & WIRE LTD amidst market uncertainty, understanding the nuances of this development is crucial. We will dissect the potential upsides and inherent risks to provide a comprehensive outlook.

The Landmark Acquisition: A New Chapter for MANHO ROPE & WIRE LTD

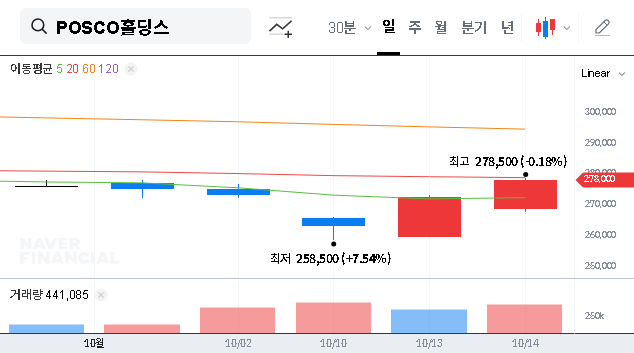

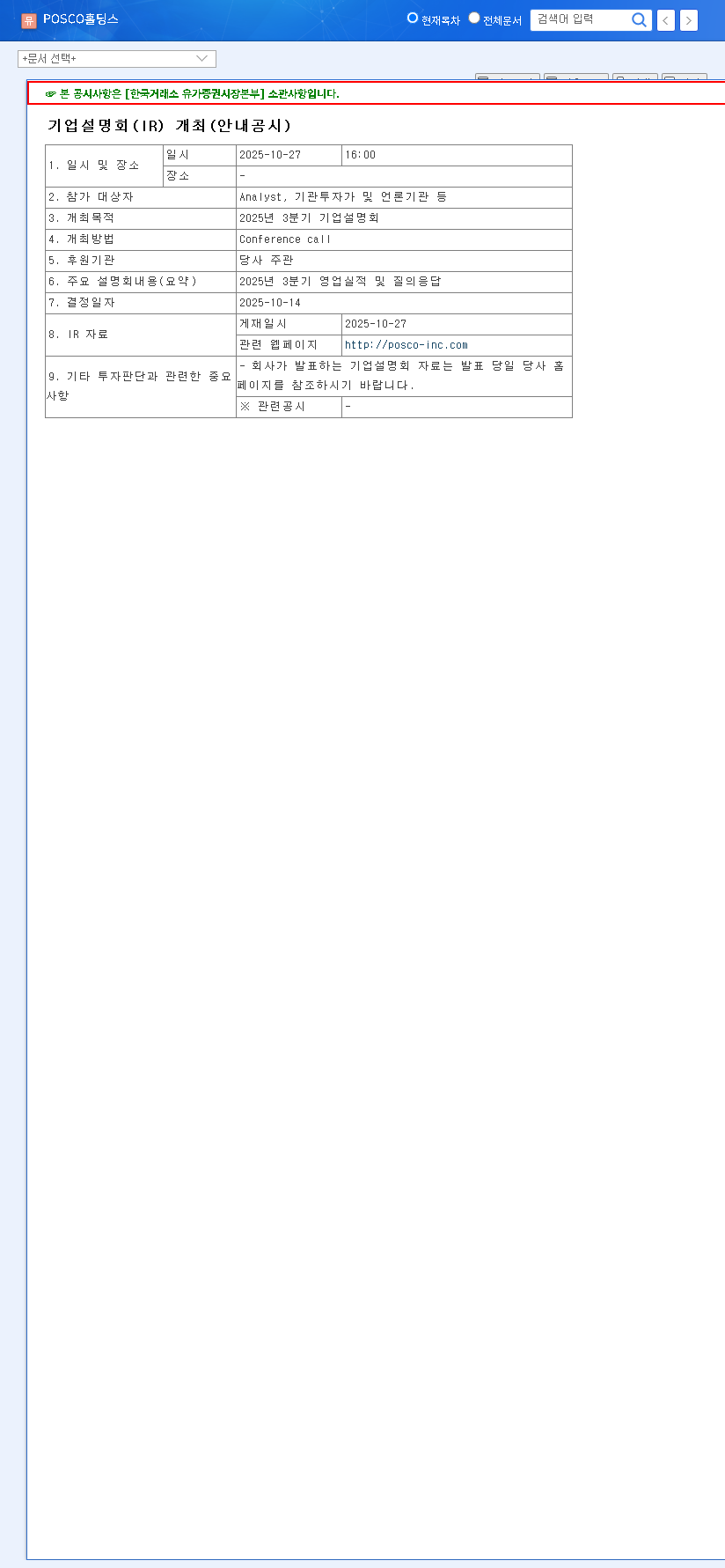

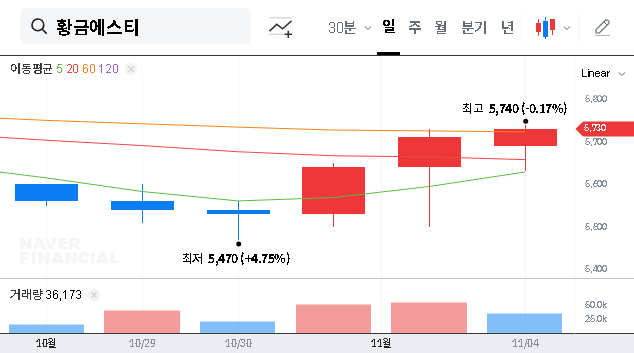

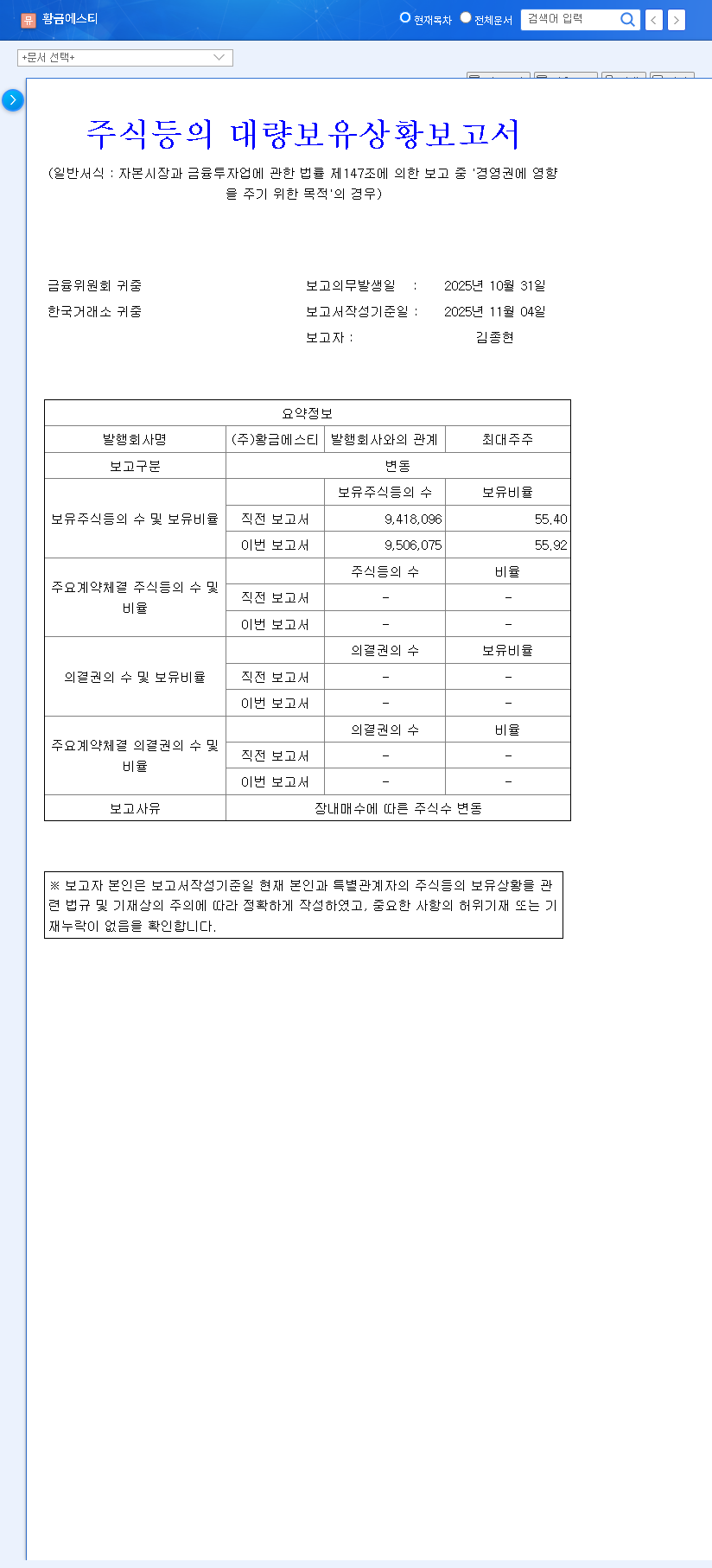

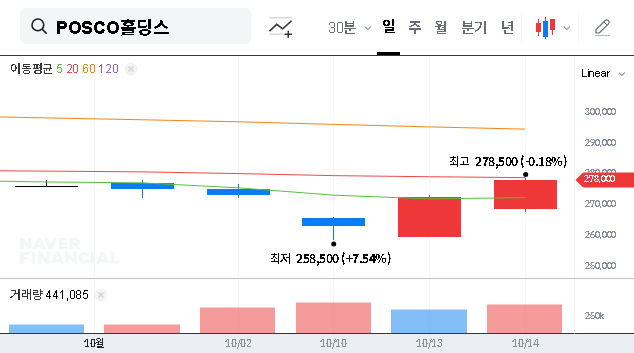

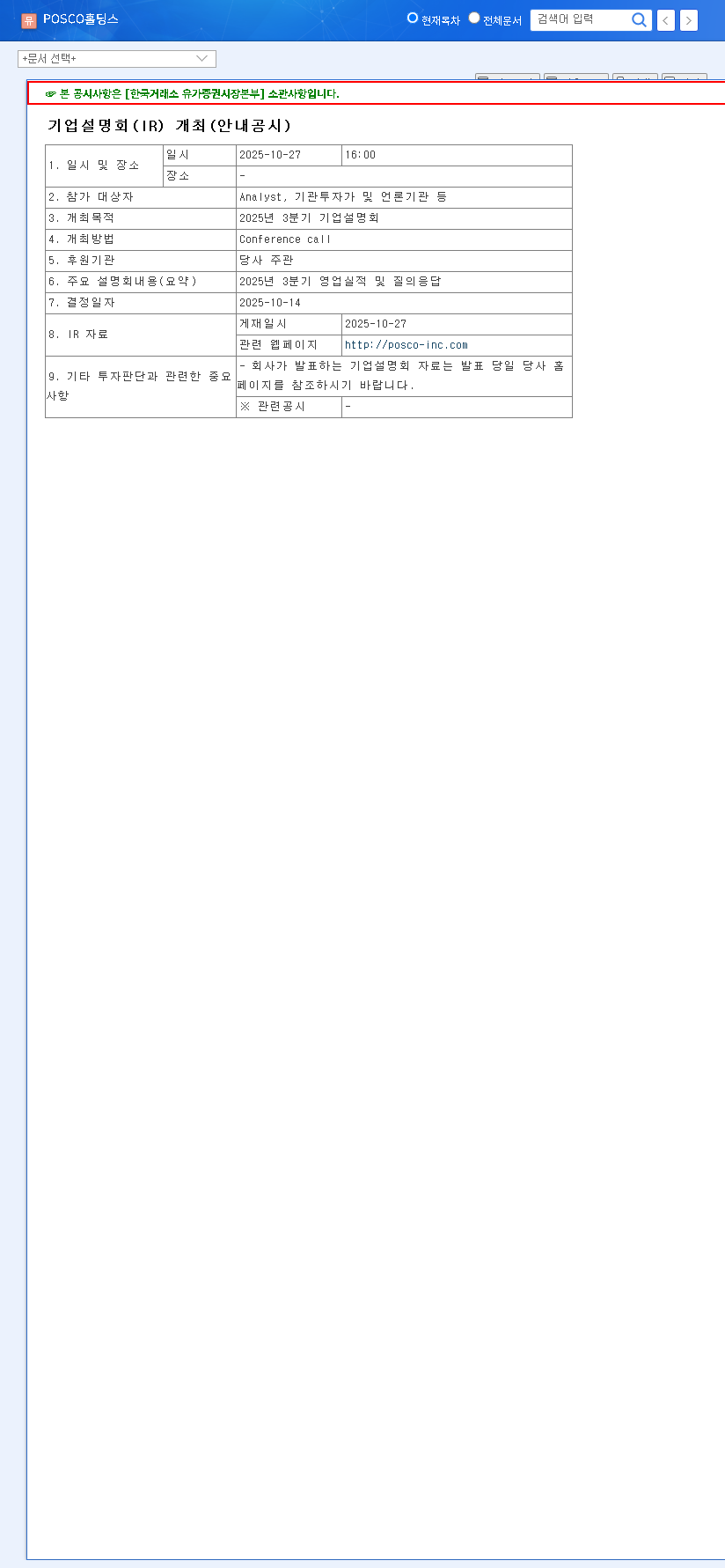

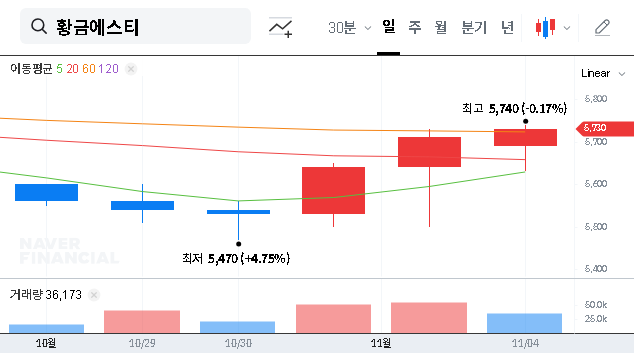

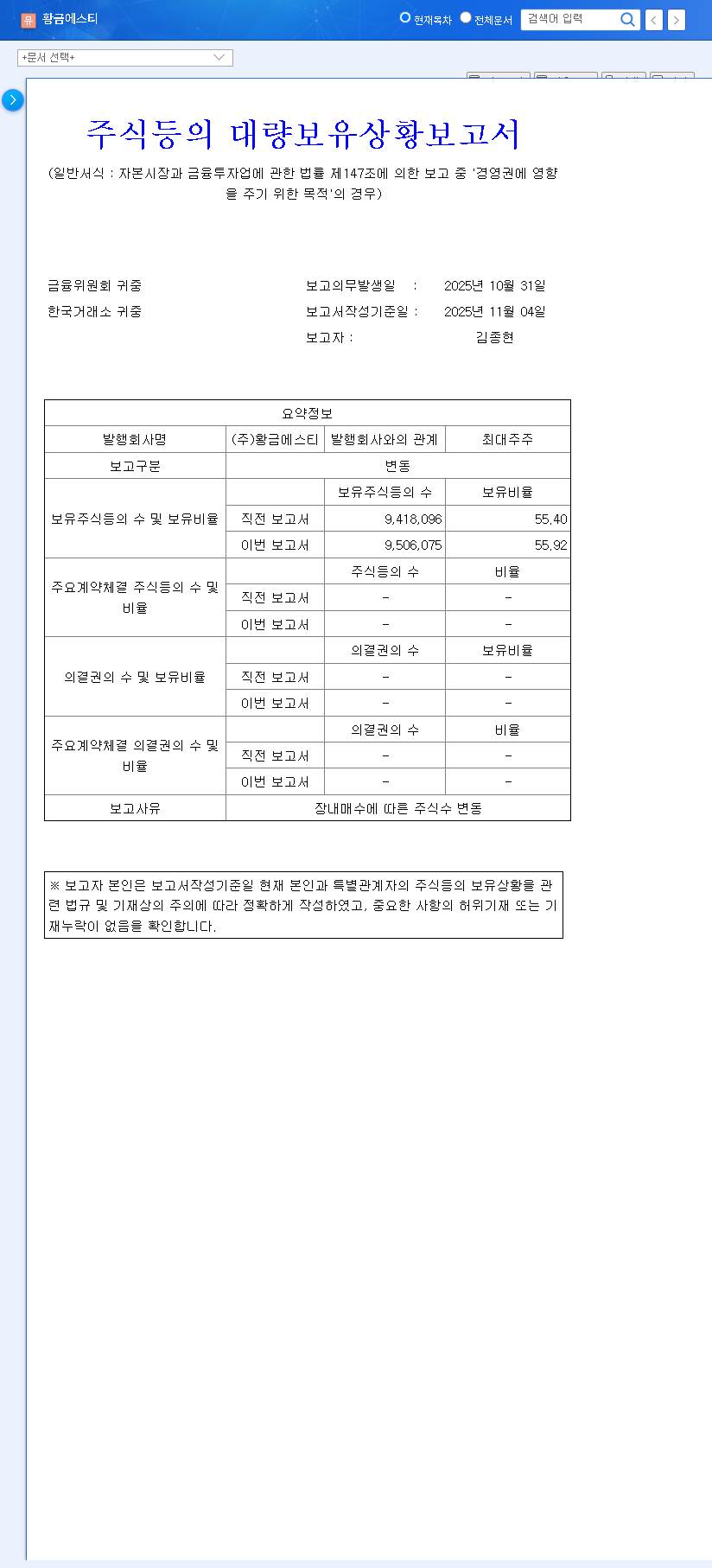

On November 12, 2025, a landmark share purchase agreement was announced, confirming MH Group Holdings’ acquisition of 1,029,992 shares of MANHO ROPE & WIRE LTD. This transaction, detailed in the Official Disclosure, unequivocally signals MH Group’s strategic intent to either seize management control or exert substantial influence over the company’s direction. For a company that once faced the severe repercussion of an auditor’s disclaimer of opinion, the arrival of a new, powerful shareholder is a transformative event that could rewrite its corporate destiny.

A Look Back: Manho’s Pre-Acquisition Financial Health

Prior to this major shake-up, the Manho Rope & Wire stock was burdened by several fundamental weaknesses that undermined investor confidence. Understanding this context is vital to appreciating the scale of the challenge and opportunity ahead.

1. Severe Financial Reporting Issues

The company’s financial credibility was severely tarnished. Widespread errors were identified and corrected in its financial statements, spanning critical areas like revenue recognition, inventory valuation, and tax expenses. The most damaging event was receiving an ‘auditor’s disclaimer of opinion’ for its 71st fiscal year. This is one of the worst possible outcomes of an audit, indicating the auditor could not obtain sufficient evidence to form an opinion on the financial statements, raising major red flags about their reliability.

2. Deteriorating Financial Indicators

The accounting issues translated into stark numbers. Total capital plummeted by approximately 34.5 billion KRW, retained earnings fell by 35.5 billion KRW, and net profit decreased by 4.14 billion KRW at the end of the 71st fiscal year. In the subsequent 72nd fiscal year, revenue dropped by nearly 18% year-over-year, and the operating loss widened significantly, painting a grim picture of the company’s operational performance.

The combination of unreliable financial reporting and worsening performance created a perfect storm of uncertainty, making the entry of a new major shareholder both a risk and a potential lifeline.

The Double-Edged Sword: Future Under MH Group’s Influence

The MH Group acquisition presents both a beacon of hope and a cloud of uncertainty for MANHO ROPE & WIRE LTD. The outcome will depend entirely on the new management’s strategy and execution.

Potential Positive Impacts

- •Improved Governance: A new controlling shareholder has the power and incentive to overhaul management, enforce transparency, and resolve the lingering financial reporting issues to restore trust.

- •Strategic Restructuring: MH Group could inject fresh capital, divest underperforming assets, and pivot the business towards new growth engines, revitalizing a company that has struggled to adapt.

- •Financial Stabilization: Active financial support from a major shareholder can lead to improved liquidity and a healthier balance sheet, providing the stability needed for a long-term turnaround.

Inherent Risks and Uncertainties

However, the path to recovery is not guaranteed. The management transition process itself can create short-term volatility and operational disruptions. It remains to be seen if the new leadership can effectively navigate the deep-seated legacy issues and persistent macroeconomic pressures from global conflicts and rising costs. For more on this, you can learn about risks in corporate takeovers from authoritative financial sources like Bloomberg.

Investor’s Playbook: Strategy for Manho Rope & Wire Stock

For current and prospective investors, this event demands a cautious yet watchful approach. The Manho Rope & Wire stock price will likely experience heightened volatility in the short term as the market digests the news and awaits clarity on MH Group’s plans. Investors should not make rash decisions based on speculation. Instead, a strategic, long-term perspective is essential. For those interested in similar situations, we have an internal guide on how to analyze M&A deals.

Key Actionable Steps for Investors

- •Monitor MH Group’s Actions: Pay close attention to official announcements regarding their management improvement strategies, financial support plans, and board appointments.

- •Watch for Key Turnaround Indicators: The most critical signal of recovery will be the attainment of an ‘unqualified audit opinion’ in future reports. This, combined with a verifiable turnaround in operating profit, will be the true test of the new management.

- •Prepare for Volatility: Acknowledge that the stock price may be unpredictable in the near term. A cautious, long-term investment horizon is paramount until a clear, positive trajectory is established.

In conclusion, the acquisition of a major stake in MANHO ROPE & WIRE LTD by MH Group is a neutral turning point, laden with both immense potential and significant risk. The coming months will be critical in revealing whether this is the beginning of a successful corporate turnaround or another chapter of uncertainty.