The recent, sharp downturn in DAEJIN ADVANCED MATERIALS Inc. stock (KRX: 393970) has understandably sent shockwaves through the investor community. Following a period of fluctuation since its KOSDAQ listing, the sudden plunge, especially after November 6th, has raised urgent questions. This turbulence was not random; it was triggered by a significant move from a major institutional investor. This comprehensive analysis will dissect the massive stake sale by SJ Investment Partners, evaluate its true impact on the company’s trajectory, and provide a clear, actionable strategy for navigating the path forward.

The Catalyst: Unpacking the SJ Investment Partners Stake Sale

The primary driver behind the recent volatility in DAEJIN ADVANCED MATERIALS Inc. stock was the large-scale divestment by SJ Investment Partners and its associated funds. Such moves by venture capital or private equity firms are often part of their fund’s lifecycle, aimed at realizing returns for their limited partners. However, the sheer size and speed of this exit inevitably created significant market pressure.

Details of the Share Divestment

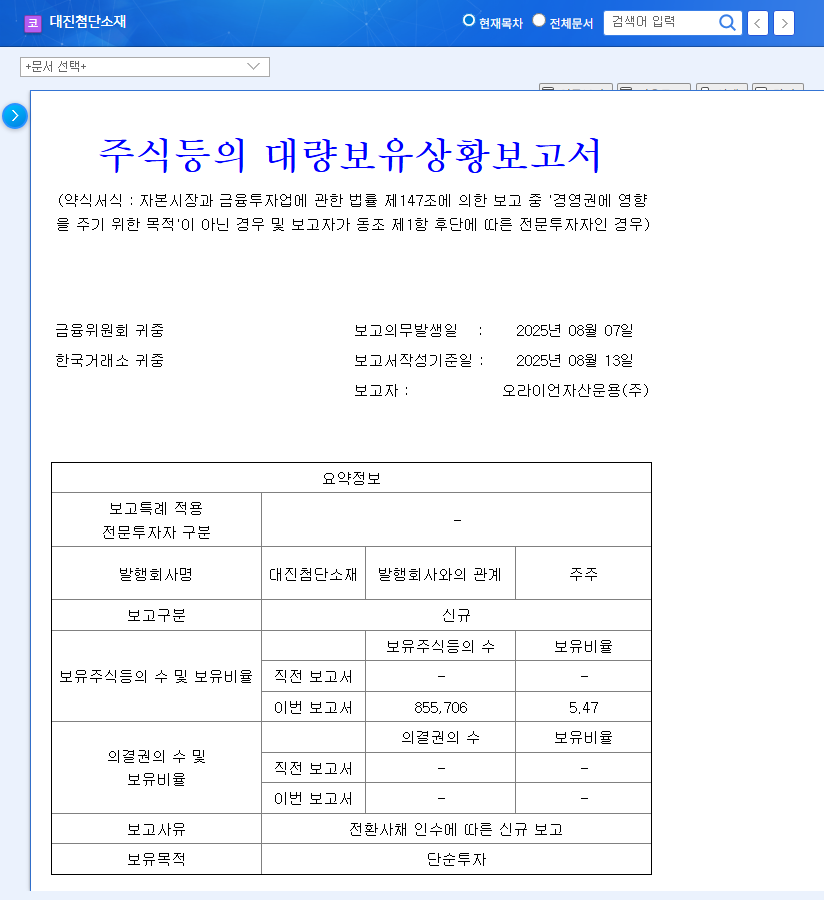

According to the official disclosure filed on November 13, 2025, the specifics of the sale paint a clear picture. You can view the full filing here: Official Disclosure (DART). The key takeaways from this SJ Investment Partners stake sale were:

- •Reporting Entities: SJ Investment Partners and four related funds.

- •Holding Purpose: Simple Investment (indicating no strategic or management control intent).

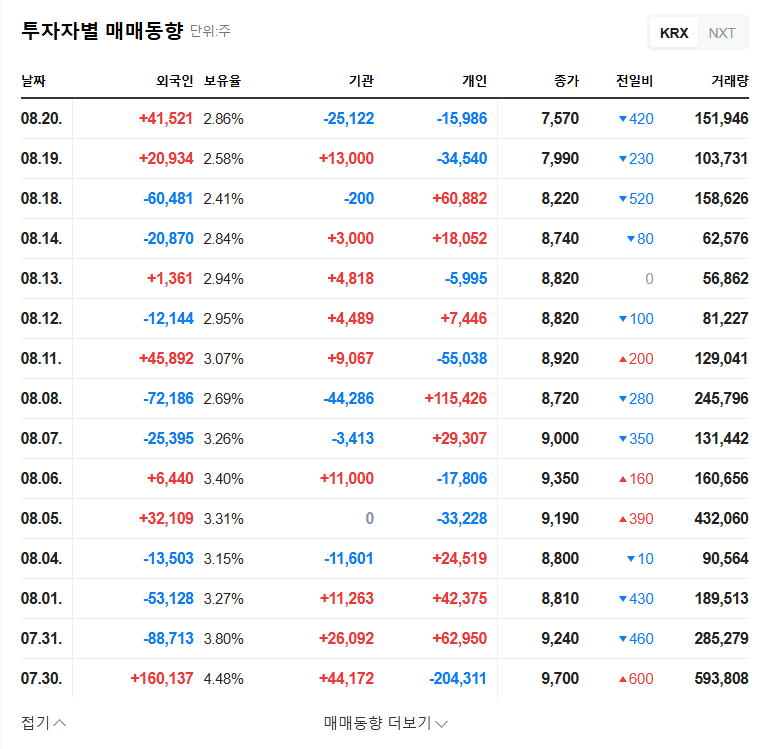

- •Shareholding Reduction: A dramatic drop from an 11.82% stake down to just 2.10%, liquidating 9.72% of the company’s total shares.

- •Primary Sale Date: A concentrated sale of 1,472,916 shares occurred on November 6, 2025, directly causing the market shock.

When an institutional investor of this size exits a position so rapidly, the market often interprets it as a strong negative signal, regardless of the underlying reason. This perception alone can fuel a cycle of panic selling among retail investors.

Analyzing the Impact on DAEJIN ADVANCED MATERIALS Inc. Stock

It is crucial for investors to separate the short-term market noise from the long-term fundamental reality. The impact of this sale must be viewed through these two distinct lenses.

Short-Term: Price Pressure and Weakened Sentiment

In the immediate term, the consequences are clear. A massive influx of shares for sale creates a supply/demand imbalance, driving the price down. This was exacerbated by the current macroeconomic climate of high interest rates and economic uncertainty, which has already dampened general market sentiment. As authoritative sources like Bloomberg often report, institutional movements are heavily scrutinized, and this exit has undoubtedly weakened investor confidence and created significant downward pressure on the stock.

Mid-to-Long-Term: Fundamentals Remain the Key

This is the most critical point for long-term investors: the stake sale does not alter the company’s intrinsic value. DAEJIN’s revenue streams, profit margins, technological assets, and core business strategy are unaffected. This was a shareholder portfolio adjustment, not a reflection of a sudden flaw in the company’s operations. In fact, the removal of this large ‘overhang’ of shares that the market knew would eventually be sold could be a long-term positive, establishing a more stable shareholder base.

Future performance will depend entirely on the company’s ability to execute on its core business, particularly its high-growth ventures like its Carbon Nanotube (CNT) business. For a deeper understanding of this technology, you can read our guide on the potential of advanced material science.

Investor Action Plan: Navigating the Volatility

Given this stock plunge analysis, a prudent and phased approach is recommended for investors considering their position in DAEJIN ADVANCED MATERIALS Inc. stock.

Short-Term Strategy (Next 1-3 Months)

- •Exercise Extreme Caution: Avoid making rash decisions. New investments should be considered high-risk until the price finds a stable support level.

- •Monitor for Capitulation: Watch for signs that selling pressure is exhausting. This may include high volume days with minimal price drops, which can indicate a bottom is forming.

- •For Existing Holders: Review your risk tolerance. Implementing a stop-loss order might be a prudent risk management strategy to protect against further significant declines.

Mid-to-Long-Term Strategy (3+ Months)

- •Focus on Fundamentals: Shift your focus from the stock chart to the company’s financial reports. Look for revenue growth, margin improvement, and positive cash flow in upcoming quarterly earnings.

- •Track Key Business Drivers: Monitor progress in the CNT division, updates on overseas subsidiary performance, and announcements of new partnerships or contracts.

- •Adopt an Observational Stance: Wait for clear, tangible evidence of business recovery and growth before committing significant new capital. Let the company prove that its fundamental value is increasing.

Frequently Asked Questions

Q1: What caused the recent sharp decline in DAEJIN ADVANCED MATERIALS Inc. stock?

The primary cause was the on-market sale of a 9.72% stake in the company by a major institutional holder, SJ Investment Partners, with a particularly large sale occurring on November 6, 2025.

Q2: Does this stake sale mean the company is in trouble?

No. This event does not directly impact the company’s core fundamentals like revenue, technology, or business operations. It is a change in shareholder structure, likely driven by the investment fund’s own strategy to realize profits.

Q3: What is the recommended investment strategy for DAEJIN ADVANCED MATERIALS Inc. stock now?

In the short term, a highly cautious and observational approach is advised due to potential continued volatility. In the long term, investment decisions should be based on a close monitoring of the company’s fundamental performance and business growth.