As Hyosung TNC Corporation prepares for its Q3 2025 performance announcement, the investment community is watching closely. This upcoming Investor Relations (IR) event is more than a routine update; it’s a critical moment for any potential Hyosung TNC investment. This comprehensive analysis will explore the company’s robust fundamentals, dissect its powerful new growth drivers, and outline the potential impacts on its stock price, providing a clear roadmap for investors.

We will delve into the details of the upcoming IR, examine the key financial and operational metrics from the first half of 2025, and provide a strategic outlook based on the opportunities and risks that lie ahead.

Hyosung TNC’s Q3 2025 IR: What Investors Need to Know

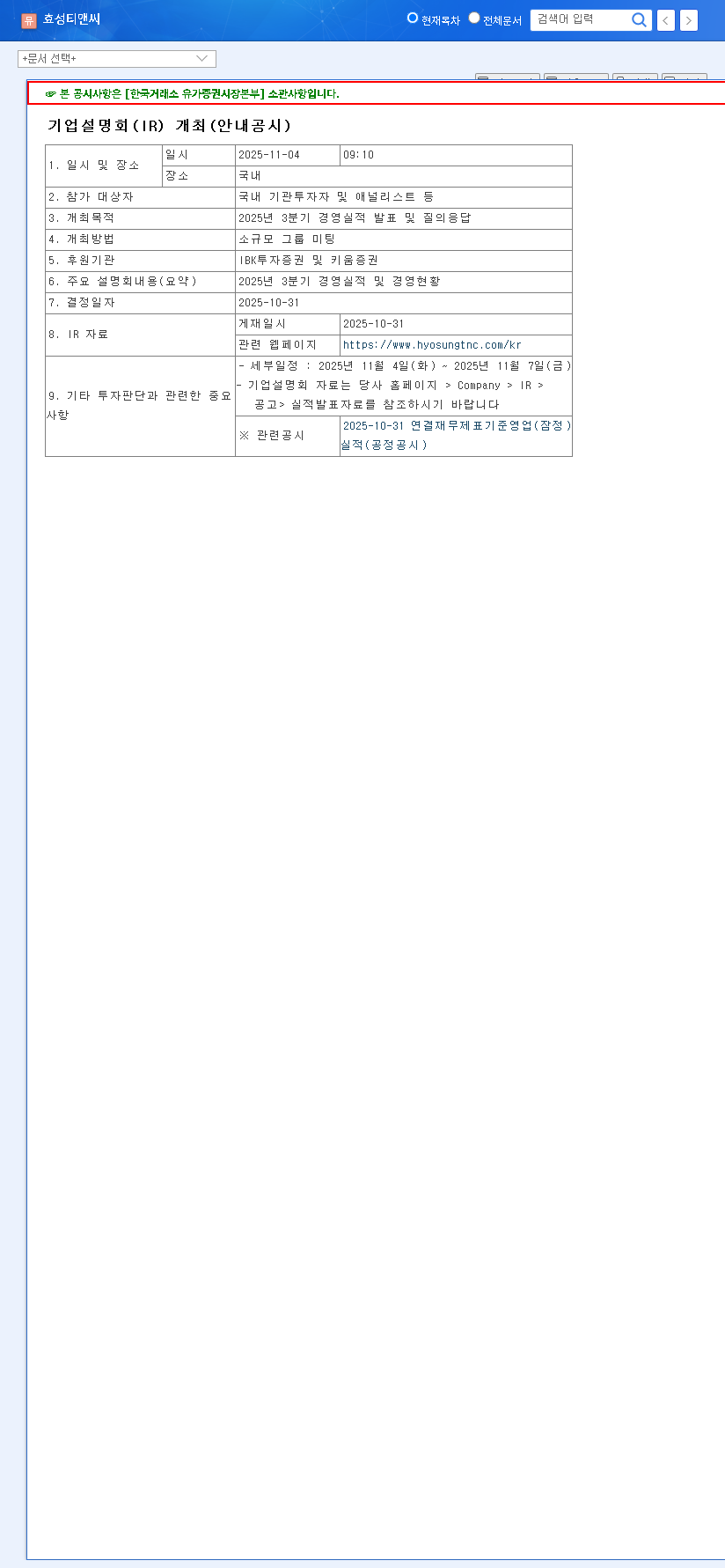

Mark your calendars: Hyosung TNC will host its much-anticipated Q3 2025 IR event on November 4, 2025, at 9:10 AM. The session is designed to offer a transparent look at the company’s third-quarter performance and current management status, followed by a Q&A with investors. This event serves as a vital communication channel, directly influencing market perception and the viability of a Hyosung TNC investment.

A Fundamental Look: Is Hyosung TNC Built to Last?

A solid Hyosung TNC stock analysis begins with its fundamentals. The 2025 semi-annual report paints a picture of a company with a strong foundation and a clear vision for the future. In the first half of 2025, the company reported sales of KRW 3.8419 trillion, with a healthy operating profit of KRW 150.7 billion. This stability across its core textile and trading divisions is a testament to its market leadership. Financially, Hyosung TNC maintains a sound position with a stable debt-to-asset ratio and a diversified borrowing structure, which helps mitigate financial risks even as it increases capital expenditure for new ventures.

Hyosung TNC’s strategy is clear: fortify its dominant position in core markets while aggressively expanding into high-growth, high-margin sectors like specialty gas and sustainable materials.

The Twin Engines of Growth: Specialty Gas & Eco-Innovation

The most exciting aspect of the Hyosung TNC IR preview revolves around its new growth drivers. The company is making bold moves that promise to reshape its future profitability and market position.

Pioneering the Specialty Gas Market

A game-changing development was the acquisition of Hyosung Chemical’s specialty gas division. This strategic maneuver instantly positioned Hyosung TNC as the world’s second-largest producer of Nitrogen trifluoride (NF3), a critical gas used in manufacturing semiconductors and flat-panel displays. As the demand for advanced electronics continues to surge, this business segment is poised for substantial growth, providing both business diversification and a high-profit revenue stream. This move significantly enhances the long-term prospects of a Hyosung TNC investment. For more on the semiconductor industry’s trajectory, you can read expert analysis from sources like Bloomberg.

Leading the Charge in Eco-Friendly Materials

While maintaining its #1 position in the global spandex market with its ‘creora’ brand, Hyosung TNC is also doubling down on sustainability. The company is expanding investments in innovative, eco-friendly materials like ‘regen ocean nylon’ (made from recycled fishing nets) and ‘creora bio-based’ spandex. Furthermore, the construction of a Bio-BDO production plant underscores its commitment to a green future. This aligns perfectly with the global shift toward sustainable consumption and ESG investing, appealing to a broader, more conscious investor base. You can learn more about sustainable fashion trends in our related article.

Q3 IR Impact: Catalysts and Risks for Investors

The upcoming IR could be a major turning point. Here’s what to watch for:

- •Positive Catalysts: If Q3 earnings beat market expectations and the company provides a concrete, data-backed growth story for its specialty gas and eco-friendly ventures, we could see a positive re-evaluation from the market. Enhanced transparency builds trust and could act as a strong momentum for stock price appreciation.

- •Potential Risks: Conversely, if Q3 results miss the mark or the management outlook is cautious, it could create downward pressure. Investors will also be keen to hear how the company is navigating macroeconomic headwinds like raw material volatility and geopolitical risks. Any perceived weakness in strategy could negatively impact sentiment.

Strategic Outlook & Investment Recommendation

Hyosung TNC has successfully diversified its portfolio with compelling new growth drivers. The Hyosung TNC Q3 2025 IR is the company’s platform to showcase these strengths. Our current recommendation is a ‘Hold’, pending the results of the IR call. Investors should analyze the specific performance outlook and growth strategies presented before making a decision. For complete due diligence, investors are encouraged to review the company’s Official Disclosure filed with DART.

If the company demonstrates strong execution in its new businesses and a resilient core performance, the argument for a long-term Hyosung TNC investment becomes significantly more compelling. A conservative approach is warranted if uncertainties surrounding the macroeconomic environment or new investment burdens are not adequately addressed.