This comprehensive SOCAR stock analysis delves into the recent market-moving news: SOQuali Co., Ltd., SOCAR’s largest shareholder, has significantly increased its stake. This action, coupled with SOCAR’s recent return to profitability in H1 2025, has sent ripples through the investment community. Is this a signal of strengthening management and a bullish future, or are there underlying risks investors should consider? We will explore the details of the shareholding change, dissect SOCAR’s financial performance, and evaluate the broader market environment to provide a clear investment perspective.

Understanding the nuances of this development is crucial for anyone considering a SOCAR investment. Let’s break down what this means for the company’s trajectory and its stock value.

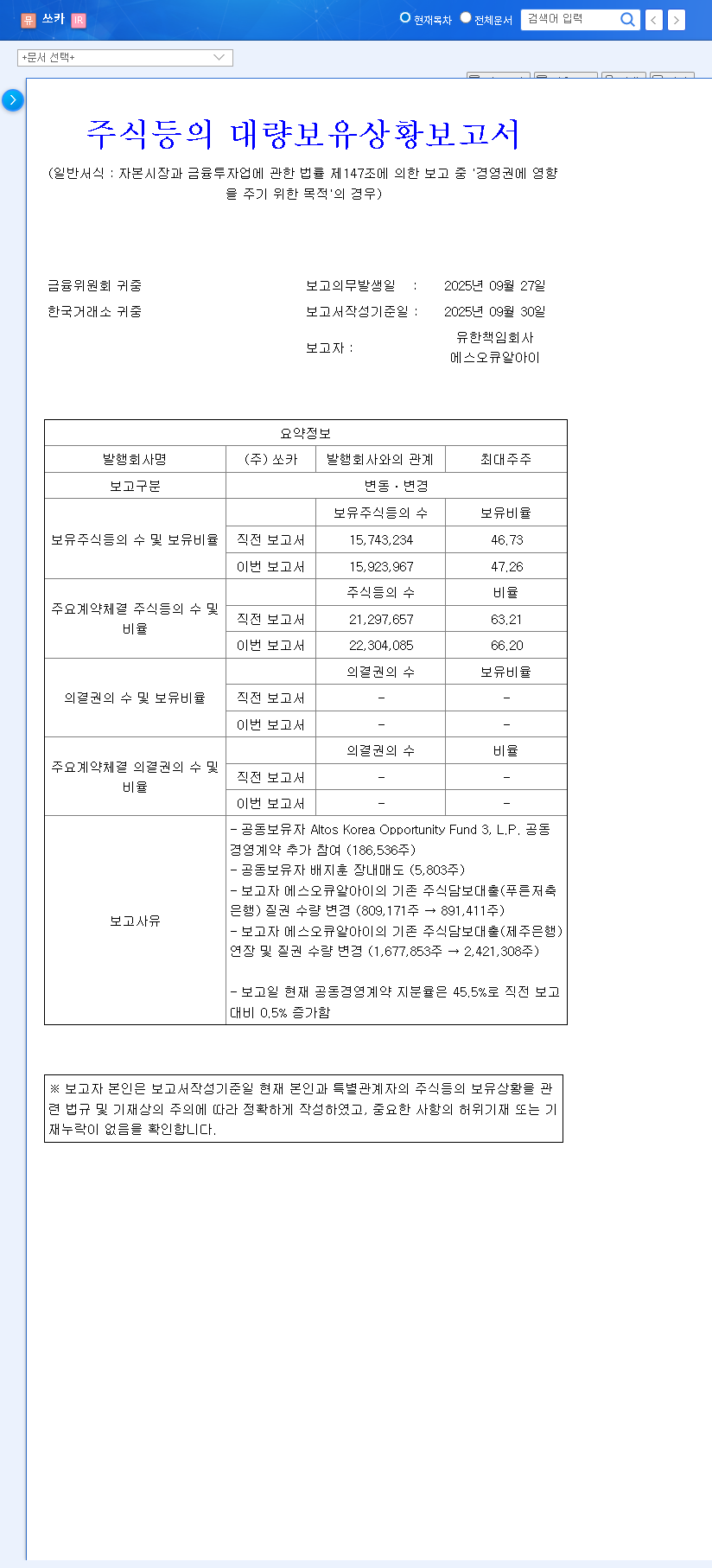

The Details: SOQuali Tightens Its Grip on SOCAR

On September 30, 2025, a significant filing revealed that SOQuali Co., Ltd. increased its ownership stake in SOCAR by 0.53 percentage points, moving from 46.73% to 47.26%. While a half-percent change may seem minor, the stated purpose was to enhance its influence over SOCAR’s management control. The full transaction details can be reviewed in the company’s public filing. (Source: Official Disclosure on DART).

This strategic move by SOQuali in SOCAR wasn’t a simple open-market purchase. It involved key adjustments to their co-management agreement, including the addition of another co-owner and minor share sales by another. This signals a deliberate consolidation of power, aimed at stabilizing governance and steering the company’s long-term strategy more directly.

SOCAR Financial Performance: A Look Under the Hood (H1 2025)

The timing of SOQuali’s move coincides with a positive turn in SOCAR’s financials. The first half of 2025 showed promising signs of recovery, but a deeper look reveals a mixed picture crucial for any SOCAR stock analysis.

Positive Momentum

- •Return to Profitability: The most significant highlight is the turnaround in operating profit, which went from a loss of 17.4 billion KRW to a profit of 3.2 billion KRW. This is a critical milestone for a growth-focused platform.

- •Strong Revenue Growth: Overall revenue climbed 19.7% year-over-year to 230.1 billion KRW, demonstrating continued market demand.

- •Improved Financial Health: The company’s debt-to-equity ratio improved from 244% to 209%, indicating progress in strengthening its balance sheet.

Underlying Areas for Concern

- •Core Business Decline: Revenue from the core Car Sharing and Platform segments actually decreased by 3.3% and 12.5%, respectively. The overall revenue growth was heavily skewed by a 3431.5% explosion in the ‘Other’ category, likely driven by one-off used car sales.

- •Drastic R&D Cuts: Research and development expenses were slashed by a staggering 74%. While this boosts short-term profitability, it raises serious questions about SOCAR’s long-term innovation pipeline and competitive edge.

- •Lingering Debt: Despite improvements, the debt level and accumulated deficit remain high, posing a financial risk. For more context, see our guide on analyzing tech company balance sheets.

While the headline profit is encouraging, investors must look deeper at the declining revenue in core segments and the sharp reduction in R&D spending to understand the sustainability of SOCAR’s growth.

Navigating the Headwinds: Market Factors Impacting SOCAR

SOCAR’s success is not determined in a vacuum. Several macroeconomic and competitive factors create a challenging environment:

- •Economic Sensitivity: As a business tied to travel and leisure, SOCAR is vulnerable to economic downturns that curb consumer spending.

- •Interest Rates & Oil Prices: Rising global interest rates, as tracked by sources like The World Bank, increase borrowing costs. Volatile oil prices directly impact vehicle operating expenses, squeezing margins.

- •Fierce Competition: The mobility market is intensely competitive, with major players like Kakao Mobility and TMAP Mobility constantly vying for market share, which puts pressure on pricing and growth.

Investment Outlook: A Strategic Guide to SOCAR Stock Analysis

The increased SOCAR shareholding by SOQuali is a vote of confidence in the company’s long-term potential and a move to ensure stable leadership. However, a prudent SOCAR investment decision must weigh this against the fundamental challenges.

Key takeaways for investors:

- •Focus on Core Fundamentals: Look beyond the headline profit. Monitor for a rebound in the core car-sharing and platform revenue streams. This is the true engine of sustainable growth.

- •Watch for R&D Reinvestment: Keep an eye on future earnings reports to see if the company resumes investment in technology and innovation. Long-term success depends on it.

- •Monitor the Macro Environment: Changes in interest rates, economic health, and competitive actions will continue to be major catalysts for stock price movement.

In conclusion, SOQuali’s increased stake is a positive signal for governance stability. When combined with the recent profitability, it creates a compelling narrative. However, the underlying operational weaknesses and external pressures demand a cautious, long-term approach. The ultimate success of a SOCAR investment will depend on the company’s ability to reignite growth in its core business while navigating a challenging economic landscape.