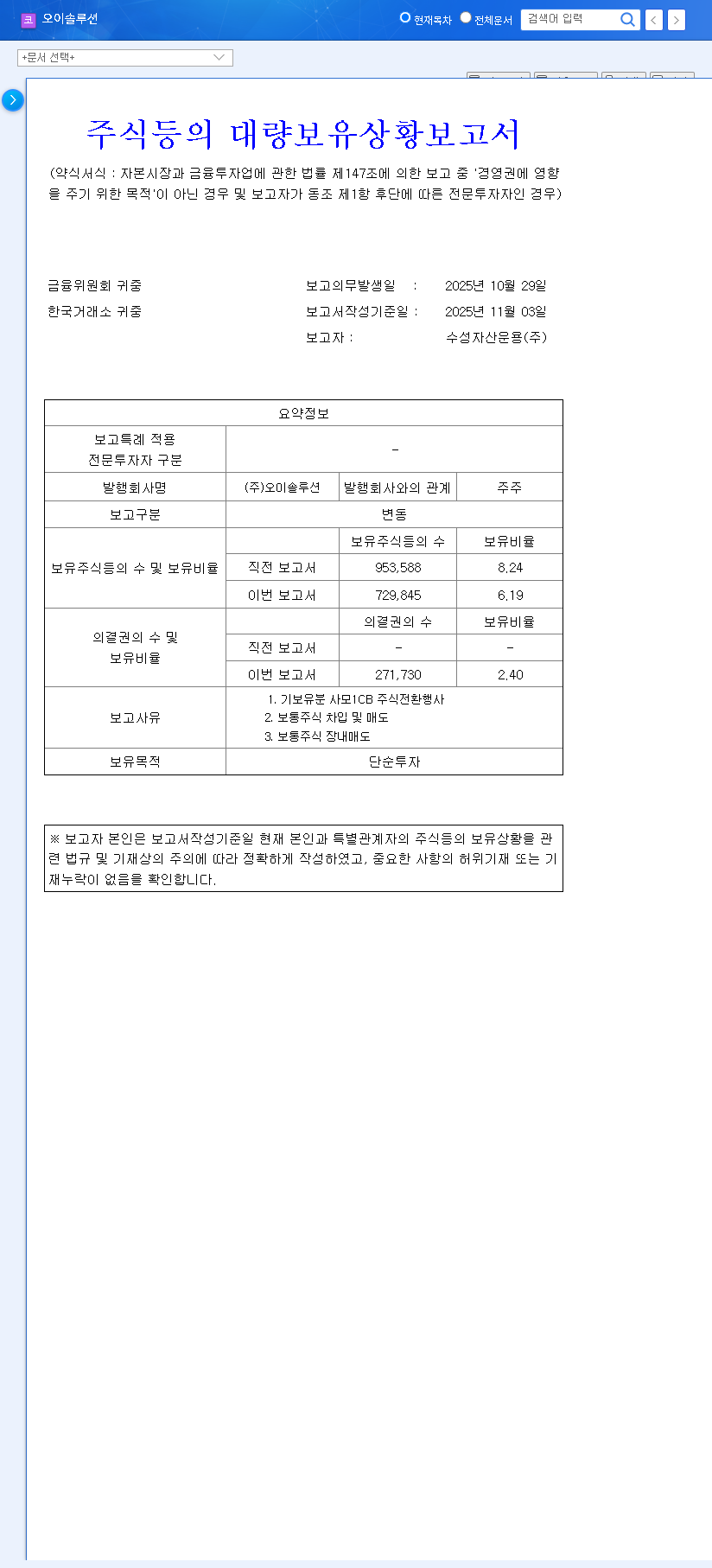

The recent OE Solutions stake reduction by major shareholder Soosung Asset Management has sent ripples through the investment community, prompting a necessary re-evaluation of the company’s stock and future prospects. This significant move, which saw the asset manager decrease its holding from 8.24% to 6.19%, is more than a simple portfolio adjustment; it’s a critical signal that warrants a thorough investigation. For current and prospective investors, understanding the context behind this divestment is paramount.

This comprehensive analysis unpacks the implications of Soosung’s move. We will dissect OE Solutions’ current fundamentals, explore the potential impact on investor sentiment and stock price, and outline a strategic framework to help you navigate this period of uncertainty. Is this a warning sign of deeper issues, or a buying opportunity in disguise? Let’s find out.

The Catalyst: Unpacking Soosung Asset Management’s Divestment

On November 4, 2025, the market took note as Soosung Asset Management formally disclosed a sale of approximately 2.05 percentage points of its shares in OE Solutions. According to the Official Disclosure (DART), this reduction was achieved through a combination of strategies, including exercising conversion rights on convertible bonds (CBs) and direct market sales. While the stated purpose was for investment, a large-scale divestment by an institutional investor is often interpreted as a bearish signal, reflecting a potential lack of confidence in the company’s near-term growth or valuation.

Institutional investors are often considered the “smart money,” and their actions can heavily influence market psychology. A significant sell-off can trigger a cascade of selling from retail investors, creating short-term downward pressure on the OE Solutions stock price. Understanding this dynamic is the first step in a sound OE Solutions investor analysis.

A Tale of Two Halves: OE Solutions’ Current Fundamentals

To understand the context of the OE Solutions stake reduction, we must examine the company’s financial health and strategic direction as of its H1 2025 report. The picture is complex, with impressive top-line growth overshadowed by persistent profitability challenges.

The core dilemma for OE Solutions is clear: Revenue is soaring on the back of market diversification and innovation, but the bottom line remains elusive due to heavy investment in future growth and high operational costs.

Positive Momentum: Growth and Innovation

- •Impressive Revenue Growth: H1 2025 revenue surged to KRW 29.9 billion, a remarkable 92.1% year-over-year increase. This is a direct result of successful market diversification beyond 5G into high-demand sectors like FTTH (Fiber to the Home), CATV, and Datacenters.

- •Investing in the Future: OE Solutions is aggressively pursuing next-generation technologies. Key projects include ELSFP for Co-Packaged Optics (CPO), 100Gbps DCO optical modules, and cutting-edge 400G coherent transceivers. These are critical components for the future of data transmission. For more on this technology, you can read our guide on The Future of Optical Transceivers.

- •New Ventures & Integration: The company is expanding into new markets like LiDAR light sources for autonomous driving and strengthening its supply chain through the vertical integration of core optical components.

Concerning Headwinds: Profitability and Financial Health

- •Persistent Losses: Despite the revenue boom, H1 2025 saw an operating loss of KRW 9.7 billion and a net loss of KRW 10.7 billion. This indicates that the cost of growth—high R&D spending and SG&A expenses—is currently outweighing income.

- •Financial Strain: The company’s debt-to-equity ratio is on the rise, primarily due to the issuance of convertible bonds to fund operations and R&D. Continuous losses raise valid concerns about long-term financial soundness.

- •Uncertain Monetization Timeline: While the R&D pipeline is exciting, these advanced technologies require lengthy development and customer approval cycles. The timeline for them to generate meaningful profit remains uncertain.

Investment Strategy: Navigating the Uncertainty

Given the conflicting signals, a nuanced investment strategy is required. The market’s reaction to the OE Solutions stake reduction creates short-term risks but also highlights long-term performance indicators to monitor.

Short-Term Outlook: Caution is Key

In the immediate future, investors should brace for increased volatility. The overhang from Soosung’s sale, combined with the potential for further CB conversions, creates significant selling pressure. A cautious, wait-and-see approach is advisable until the market absorbs this new supply of shares. According to market behavior studies from Reuters, institutional sell-offs can depress a stock for several quarters.

Mid-to-Long-Term Outlook: Focus on Execution

The long-term success of OE Solutions hinges on its ability to convert its technological prowess into profit. Investors should shift their focus from short-term stock movements to a few key performance indicators:

- •Path to Profitability: Watch for sequential improvements in operating margins in upcoming quarterly reports. Is the company gaining control over its costs?

- •Commercialization Milestones: Look for announcements of customer acquisitions or design wins for their next-generation products (CPO, 400G modules, LiDAR).

- •Financial De-risking: Monitor the company’s efforts to manage its debt and improve its financial structure.

Conclusion: A Critical Juncture for OE Solutions

Soosung Asset Management’s stake reduction serves as a potent reminder of the challenges facing OE Solutions. While the company’s innovation and revenue growth are undeniable strengths, the lack of profitability and financial pressures are significant risks that cannot be ignored. For investors, this is a time for diligence, not panic. The key is to monitor the company’s progress on its path to profitability and its ability to execute its ambitious technology roadmap. The coming quarters will be pivotal in determining whether OE Solutions can translate its vision into sustainable value for shareholders.