In a significant strategic pivot, telecommunications leader Solid, Inc. has announced a major move that has the market buzzing. The Solid Inc Darwin Friction acquisition, a ₩10 billion deal for a majority stake in an aircraft parts manufacturer, signals a bold leap into the Solid Inc defense sector ambitions. This move aims to diversify revenue streams and secure new growth engines beyond its core telecom business. But what does this mean for the company’s future, and how should investors interpret this development for their stock analysis?

This comprehensive analysis will delve into the specifics of the acquisition, evaluate Solid’s underlying financial health, and explore the potential synergies and inherent risks. We’ll provide a clear-eyed view of both the promising opportunities and the significant challenges that lie ahead for Solid, Inc. following this transformative investment.

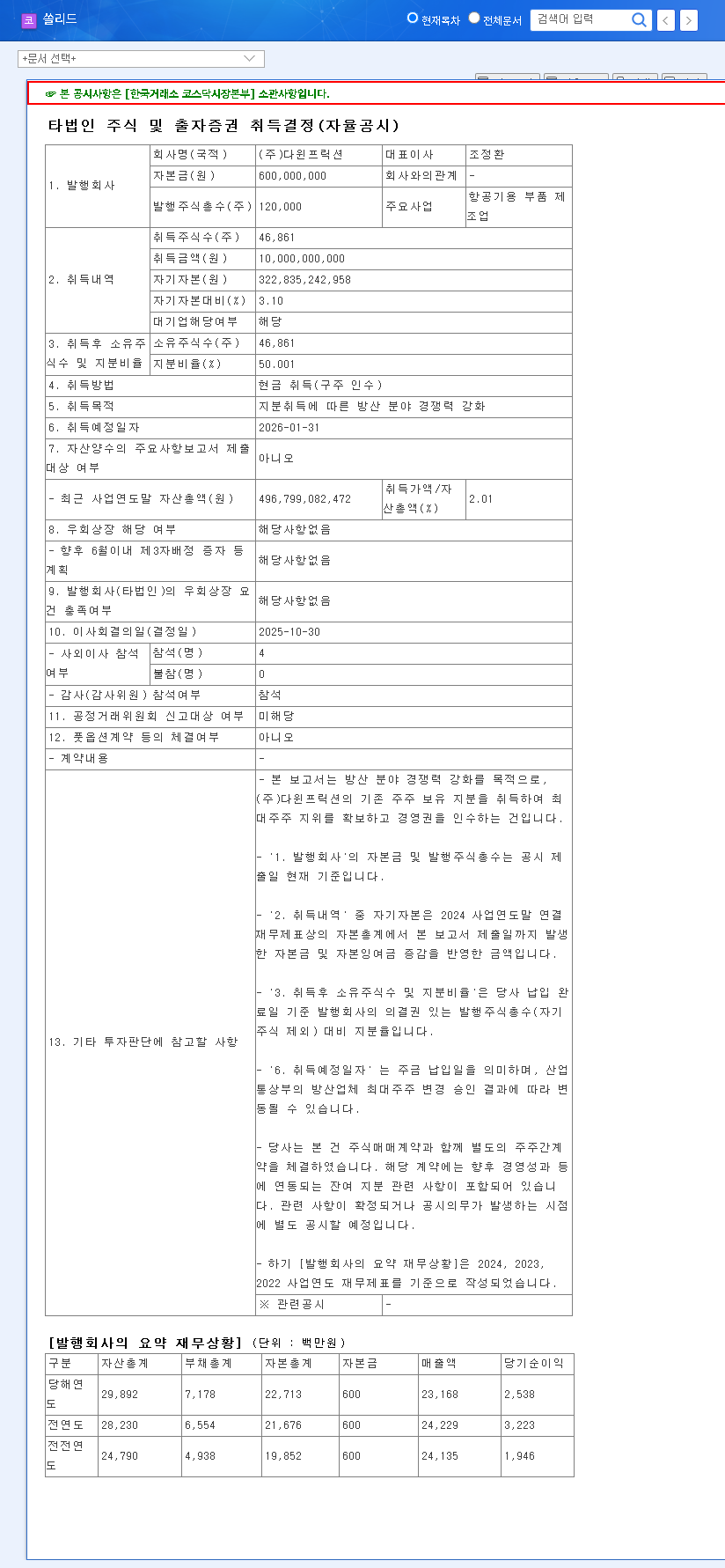

The Details of the Deal: Solid Inc’s Acquisition of Darwin Friction

On October 30, 2025, Solid, Inc. confirmed its strategic investment via a public announcement. The company is set to acquire a controlling 50.001% stake in Darwin Friction for ₩10 billion, with the cash transaction scheduled to be completed by January 31, 2026. This investment represents 3.10% of Solid’s total capital. The full details of the transaction were confirmed in an Official Disclosure filed with the Financial Supervisory Service (DART).

Darwin Friction is a specialized manufacturer of high-performance friction materials, primarily for braking systems in military and commercial aircraft. The explicit goal of this acquisition is to significantly bolster Solid’s competitiveness within the burgeoning Solid Inc defense sector and strategically diversify its business portfolio for long-term, sustainable growth.

Strategic Rationale: Why This Pivot to Defense?

To understand the logic behind the Darwin Friction acquisition, it’s essential to examine Solid’s current business landscape and financial standing. This move isn’t happening in a vacuum; it’s a calculated decision based on internal strengths and external market opportunities.

Solid’s Strong Financial Foundation

Solid, Inc. enters this deal from a position of improving financial strength. After turning a deficit in 2023, the company has demonstrated a strong recovery, posting a net profit of ₩4 billion in the first half of 2025. Its financial health is robust, with a debt-to-equity ratio improving to 49.38% and a healthy liquidity ratio of 111.97%. This stability provides the necessary capital and confidence to pursue strategic acquisitions like that of Darwin Friction without over-leveraging the company.

Core Business and Market Tailwinds

While diversifying, Solid’s core business in 5G and Open RAN telecommunications equipment continues to benefit from a positive market environment. For more on this technology, you can read our guide on understanding the Open RAN ecosystem. Concurrently, its existing defense communications subsidiary, Solidwintech, provides a stable foundation and a logical entry point for deeper integration into the defense supply chain. With a high export dependency (73.8% of revenue), favorable exchange rates and declining global logistics costs also create a positive macroeconomic backdrop for this expansion.

This acquisition is a clear signal of Solid’s intent to evolve from a pure-play telecom provider into a diversified technology powerhouse with a significant footprint in the high-margin defense industry.

Impact Analysis: Opportunities vs. Risks

The Solid Inc Darwin Friction acquisition presents a duality of compelling opportunities and notable risks that investors must weigh carefully.

The Upside: Potential Synergies and Growth

- •Defense Sector Synergy: The most significant opportunity lies in combining Solidwintech’s defense communication systems with Darwin Friction’s critical aircraft components. This could lead to integrated, higher-value solutions for defense clients and unlock cross-selling opportunities.

- •Portfolio Diversification: The deal reduces Solid’s reliance on the cyclical telecom market and its high sensitivity to North American and European demand, creating more stable, diversified revenue streams.

- •Long-Term Value Creation: By securing a foothold in the resilient defense industry, Solid is positioning itself for long-term growth. As noted by industry analysts at authoritative sources like Bloomberg, the global defense market is projected to see steady growth.

The Downside: Potential Challenges and Concerns

- •Integration Complexity: Merging the cultures and operations of a telecom equipment firm and an aerospace parts manufacturer is a significant challenge. The risk of execution failure or a lack of meaningful synergy is real and could turn the acquisition into a financial drain.

- •Financial Strain: While Solid’s finances are healthy, the ₩10 billion cash outlay is substantial. This could temporarily strain cash flow and limit capital available for R&D in its core telecom business if returns from Darwin Friction are not realized promptly.

- •Market Volatility: The defense market is subject to geopolitical tensions and shifts in government spending priorities. This introduces a new layer of risk and volatility that Solid’s management must learn to navigate.

Conclusion: A Calculated Gamble for Future Growth

Solid, Inc.’s acquisition of Darwin Friction is a bold, strategic gamble. It has the clear potential to unlock significant long-term value by establishing a strong new pillar in the defense sector. The success of this venture will hinge entirely on management’s ability to execute a seamless integration and realize the promised synergies between these two disparate business units.

For investors, the short-term Solid Inc stock analysis will likely show volatility as the market digests the news. However, the long-term trajectory will be determined by tangible results. Close monitoring of integration milestones and the performance of the newly formed defense division will be critical in assessing whether this strategic leap will ultimately pay off.