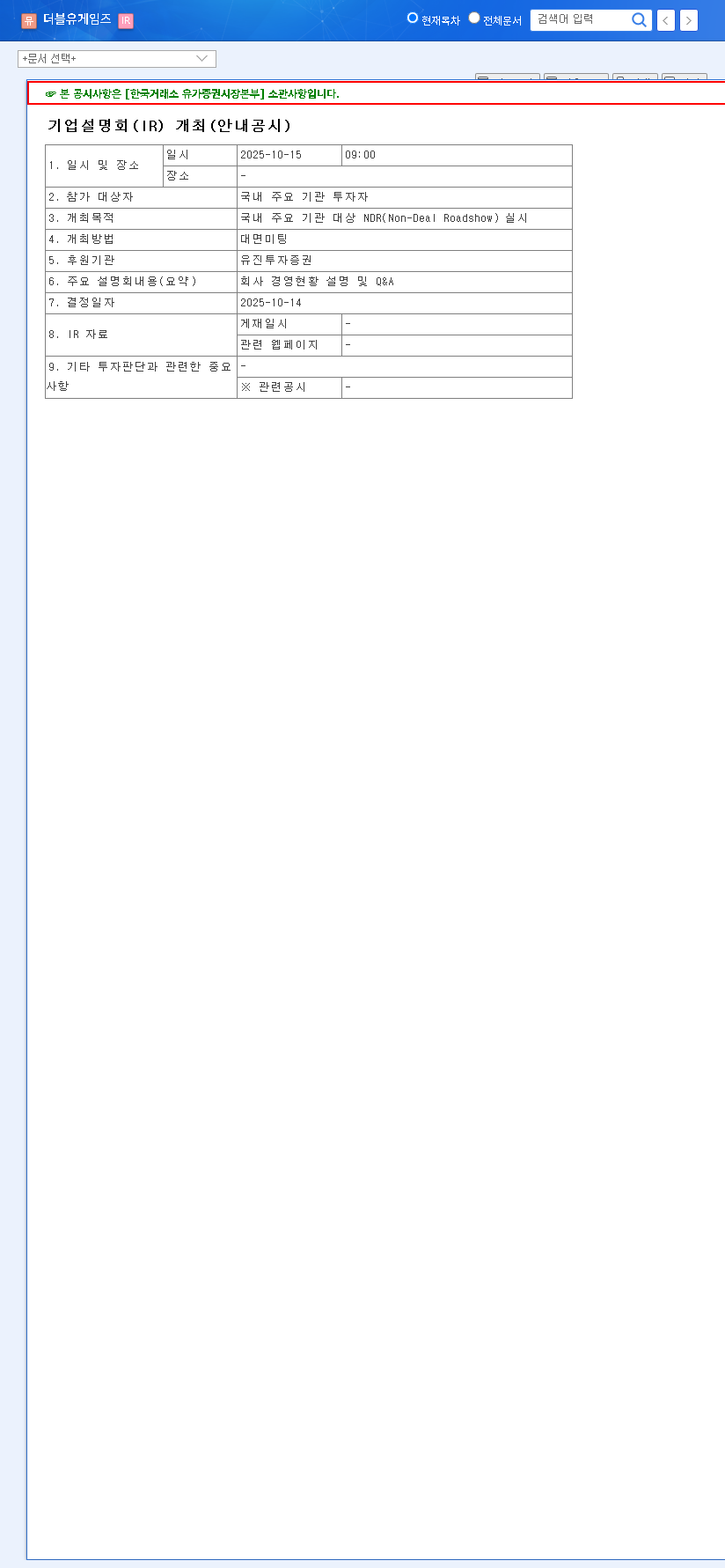

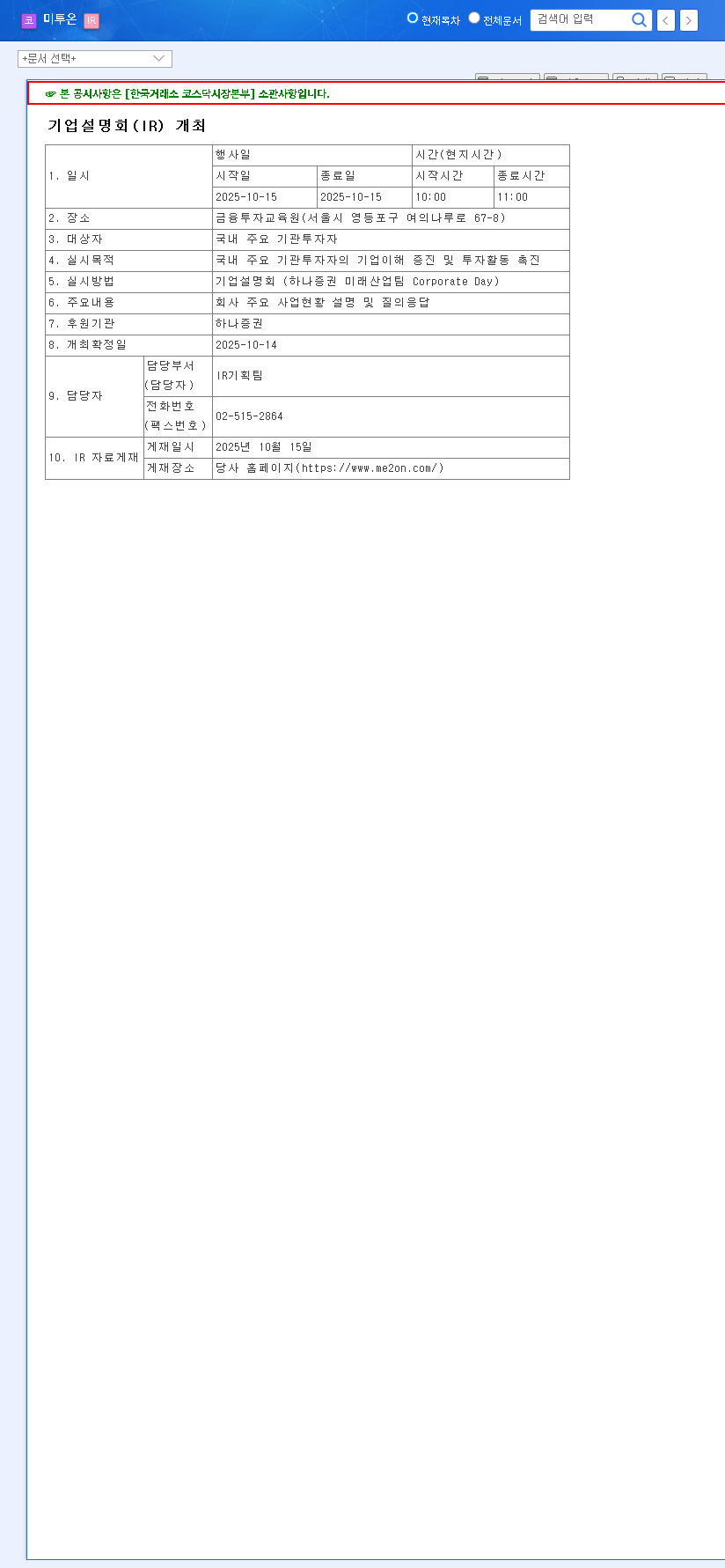

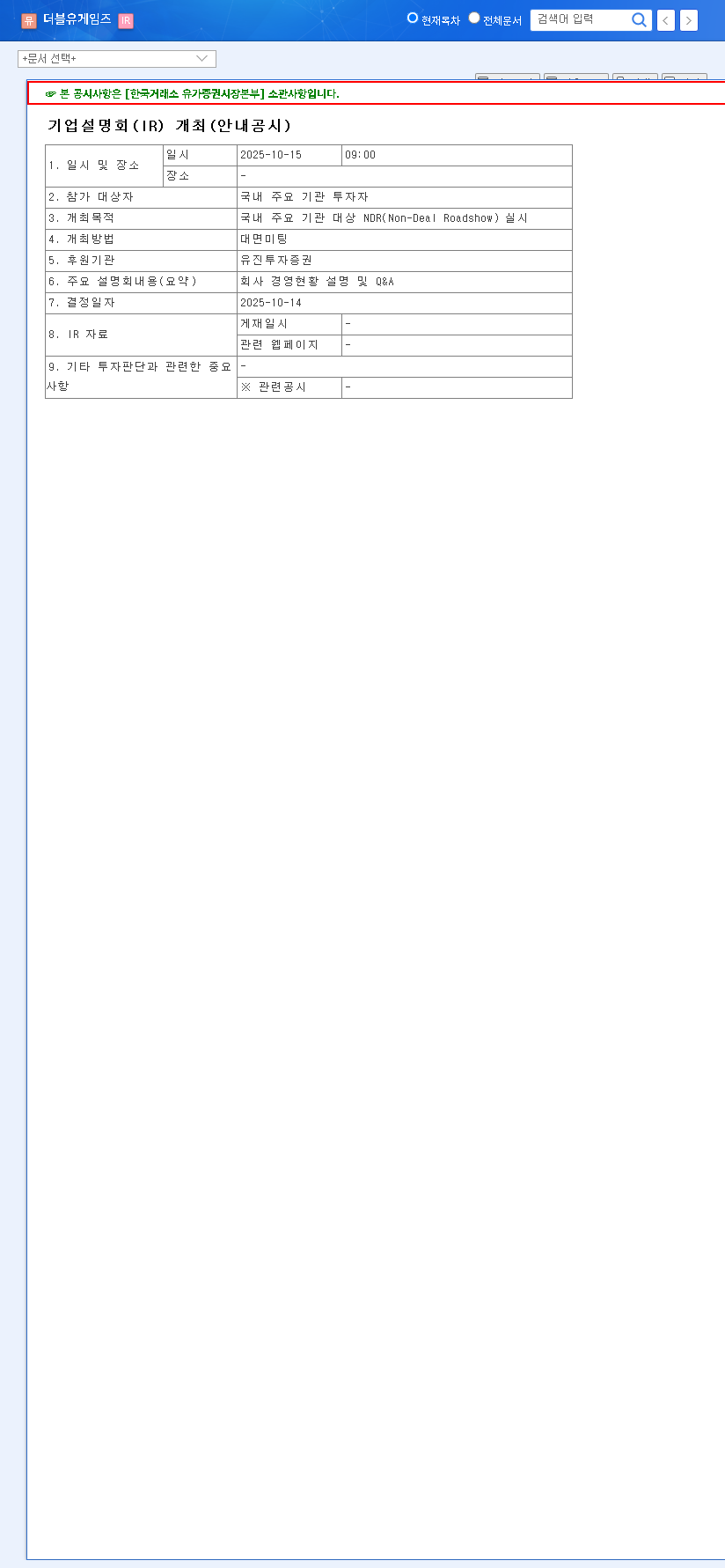

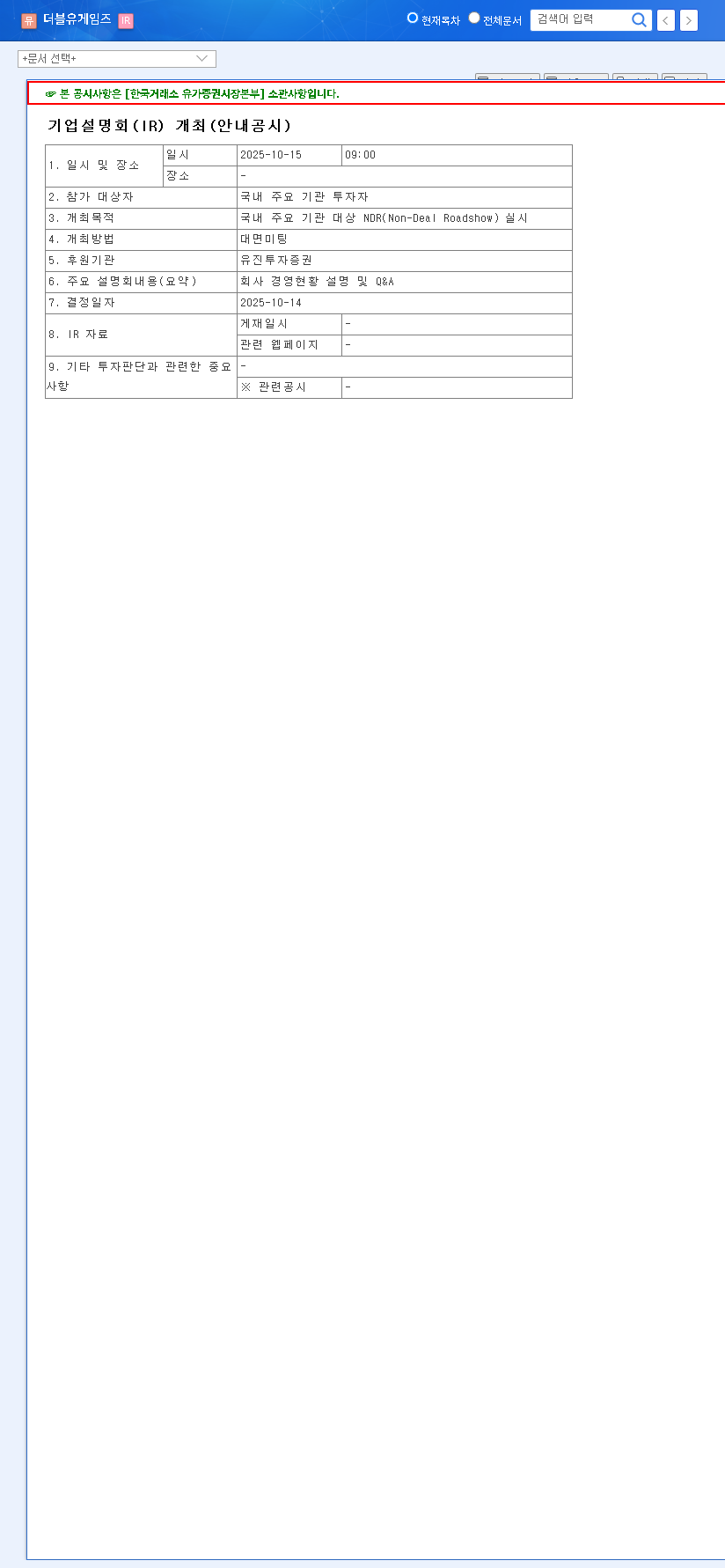

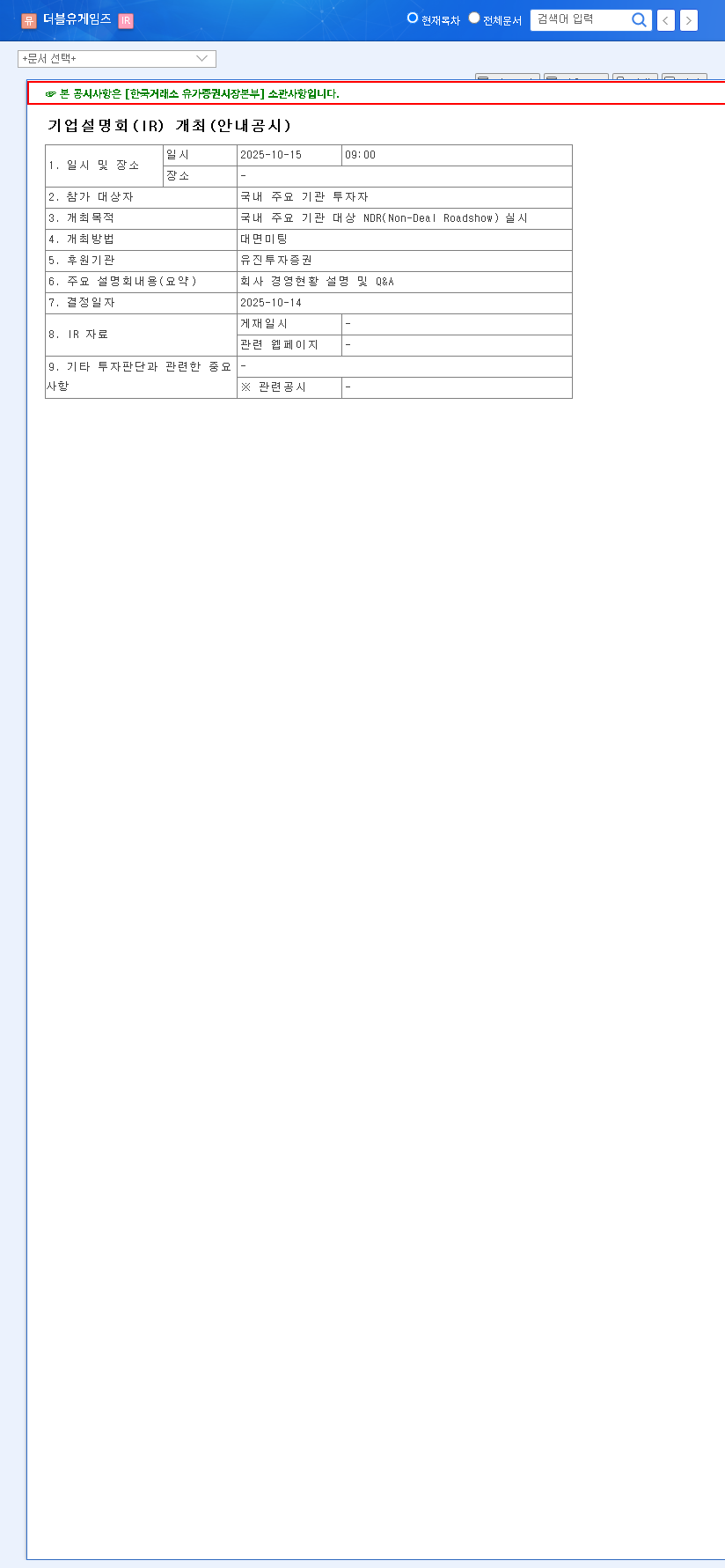

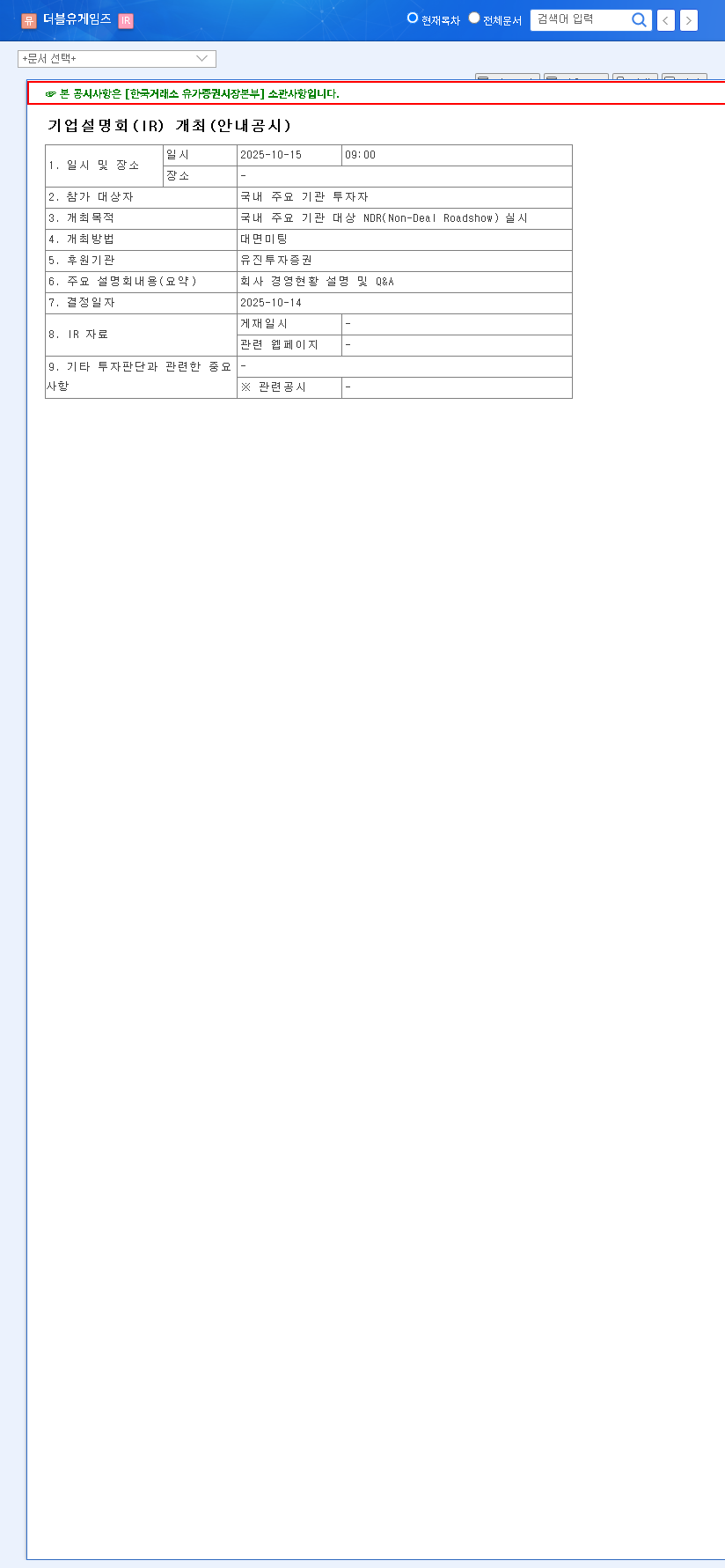

The upcoming DoubleUGames IR (Investor Relations) briefing is a pivotal event for investors tracking DoubleUGames Co., Ltd.. Scheduled for November 19, 2025, at 9:00 AM KST, this session will provide crucial insights into the Q3 2025 business results, shaping the narrative around the company’s future and the trajectory of DoubleUGames stock. This analysis offers a comprehensive guide for investors, dissecting the company’s fundamentals, growth drivers like its burgeoning iGaming segment, and the key factors to watch during the presentation.

The Q3 2025 Investor Relations Briefing: What’s at Stake?

This official Investor Relations event is more than just a financial report; it’s a platform for transparent communication with major domestic institutional investors. The company will unveil its Q3 2025 performance and field questions regarding its current status and strategic vision. This is a critical moment for re-evaluating the company’s intrinsic value and understanding its direction. The briefing is based on the company’s official filing. Source: Official Disclosure (DART).

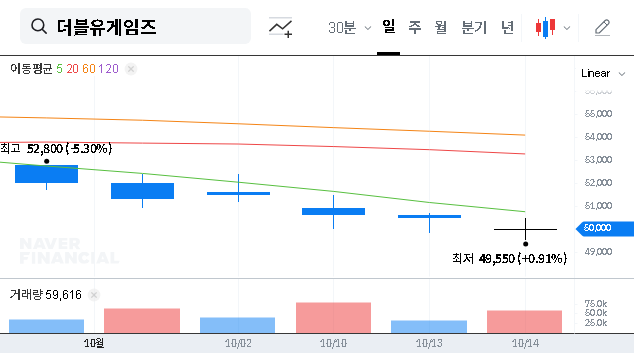

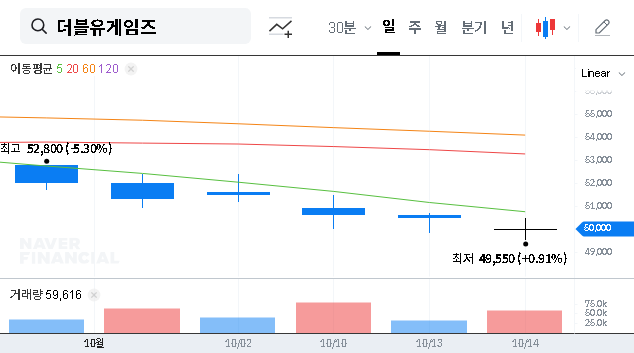

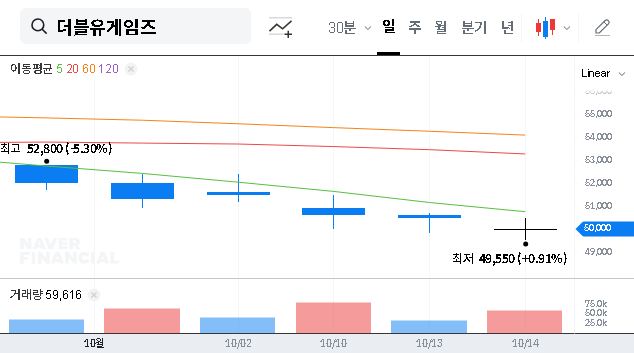

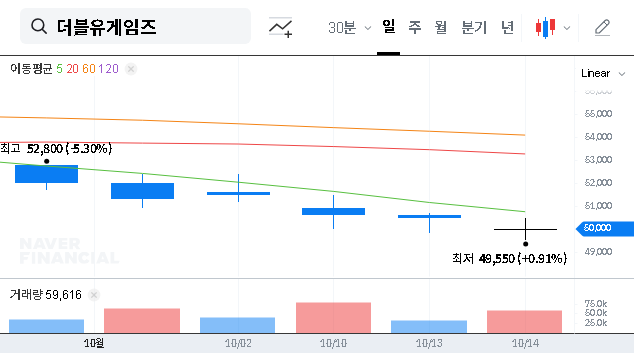

For investors, the DoubleUGames IR is the primary opportunity to gauge management’s confidence and to scrutinize the strategies that will drive future shareholder value.

Analyzing DoubleUGames’ Fundamentals and Growth Engines

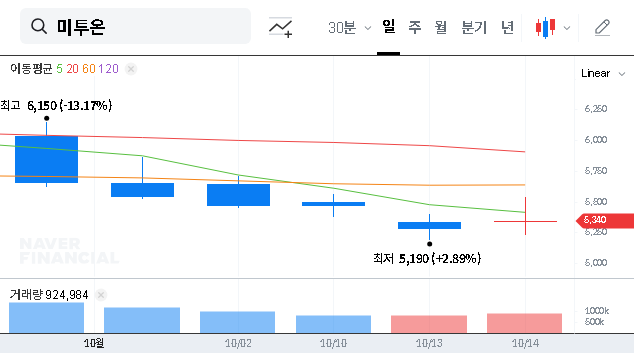

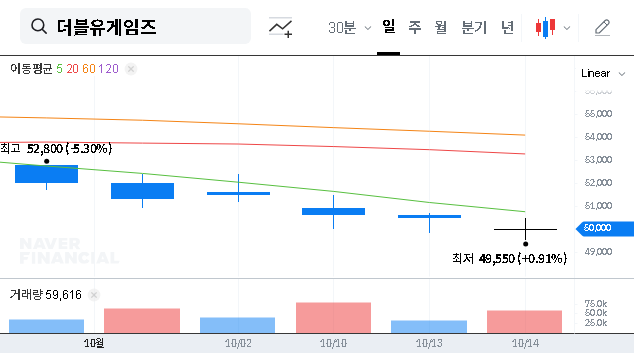

To understand the context of the Q3 report, we must first look at the company’s performance in the first half of 2025. While revenue saw a slight dip, the significant rise in operating profit tells a story of enhanced efficiency and strategic success.

H1 2025 Performance Snapshot

- •Revenue: KRW 333.9 billion (a decrease of 3.2% YoY).

- •Operating Profit: KRW 109.1 billion (a significant increase of 15.0% YoY).

This profitability improvement is not accidental. It is the direct result of strategic pillars that are expected to be key topics at the DoubleUGames IR event.

Key Growth Drivers to Watch

- •iGaming Segment Expansion: The acquisitions of SuprNation AB and Paxie Games have supercharged the company’s iGaming growth. This high-margin segment now constitutes 12.3% of total revenue and is the primary engine for profit expansion.

- •Strategic Portfolio Diversification: Beyond its core offerings, the company is actively developing new casual games and pursuing M&A to build a resilient, long-term growth foundation.

- •Robust Financial Health: With KRW 104.2 billion in operating cash flow and a low debt-to-equity ratio of 38.67%, the company’s financial stability is a major asset.

- •Commitment to Shareholder Returns: A planned KRW 35 billion treasury share buyback and cancellation is a clear, positive signal to the market about the management’s confidence in DoubleUGames stock value. For more, see our detailed guide on understanding shareholder return policies.

Market Risks and Potential Headwinds

Despite its strong position, DoubleUGames operates in a dynamic environment with inherent risks that investors must consider.

- •Intense Market Competition: The social casino market is fiercely competitive. While DoubleUGames holds a solid 5th place with a 6.1% market share, continuous innovation is necessary to defend and grow this position.

- •Macroeconomic Uncertainty: A global economic slowdown could reduce consumers’ disposable income, which may negatively impact spending on online gaming and entertainment.

- •Currency Fluctuations: As a global operator, the company is exposed to US dollar exchange rate volatility, which can impact reported financial results.

Investor Action Plan: Key Questions for the IR

Informed investors should listen closely during the Q&A for answers to several key questions that will determine the future of DoubleUGames stock.

Critical Focus Points for Investors

- •Deep Dive on Q3 Earnings: What specific factors drove revenue and profit changes? What was the precise growth contribution from the iGaming segment?

- •Future M&A and Expansion: What are the integration updates for Paxie Games? What are the company’s future M&A plans and long-term growth targets for iGaming and casual games?

- •Competitive Strategy: How does DoubleUGames plan to differentiate itself and gain market share in the crowded social casino space?

- •Shareholder Return Execution: What is the exact timeline for the announced treasury stock buyback and cancellation?

Ultimately, this DoubleUGames IR is a critical inflection point. The information presented and the clarity of management’s vision will directly influence investor confidence and could set the tone for the stock’s performance in the months to come. Careful analysis is paramount for making well-informed investment decisions.