The latest SK Innovation Q3 2025 earnings report has sent a complex but powerful signal to the market. While the company delivered a stunning operating profit that crushed expectations, a surprising net loss has raised critical questions about its costly but vital pivot towards a green energy transition. This comprehensive analysis will break down the key figures, explore the driving forces behind this dual-sided performance, and outline the strategic opportunities and challenges that lie ahead for investors monitoring SK Innovation stock.

Breaking Down the SK Innovation Q3 2025 Earnings Report

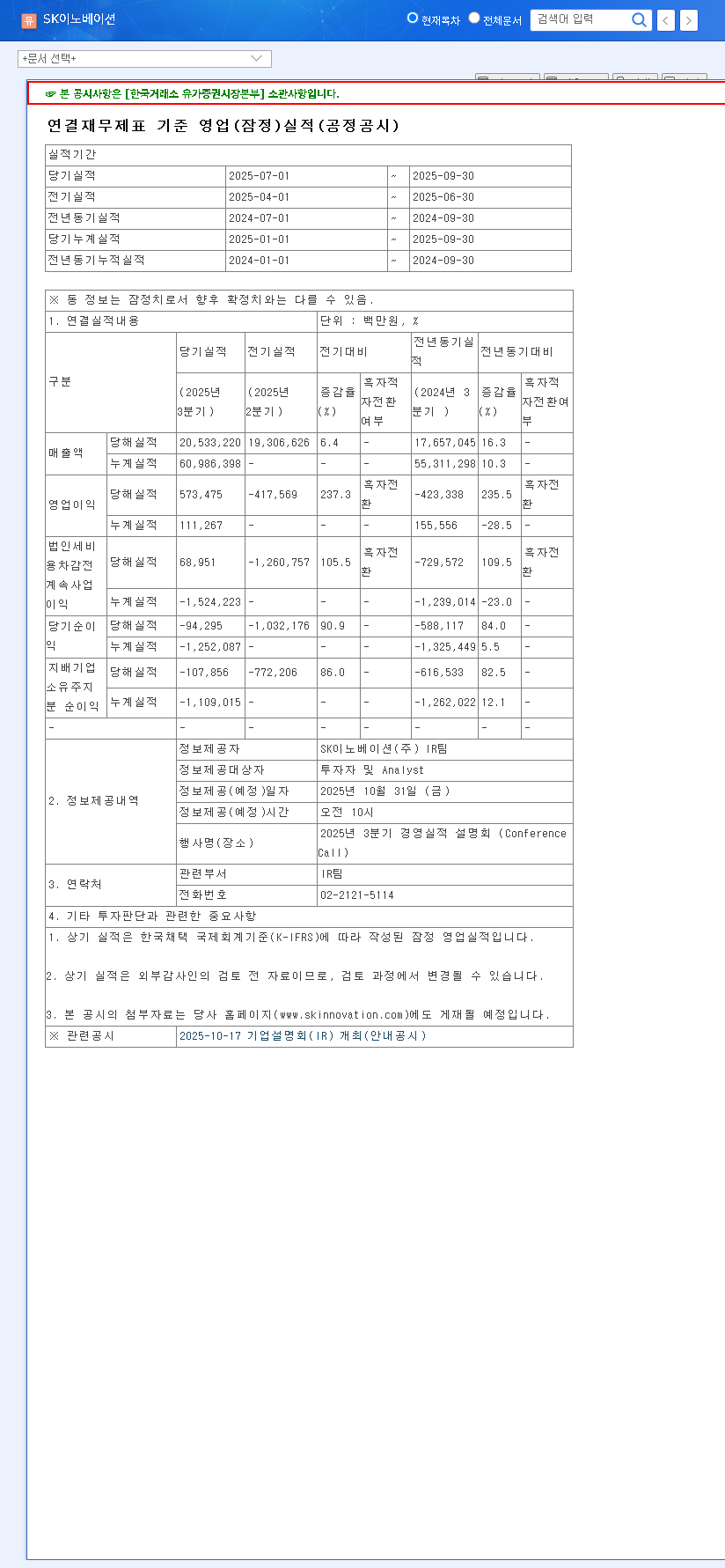

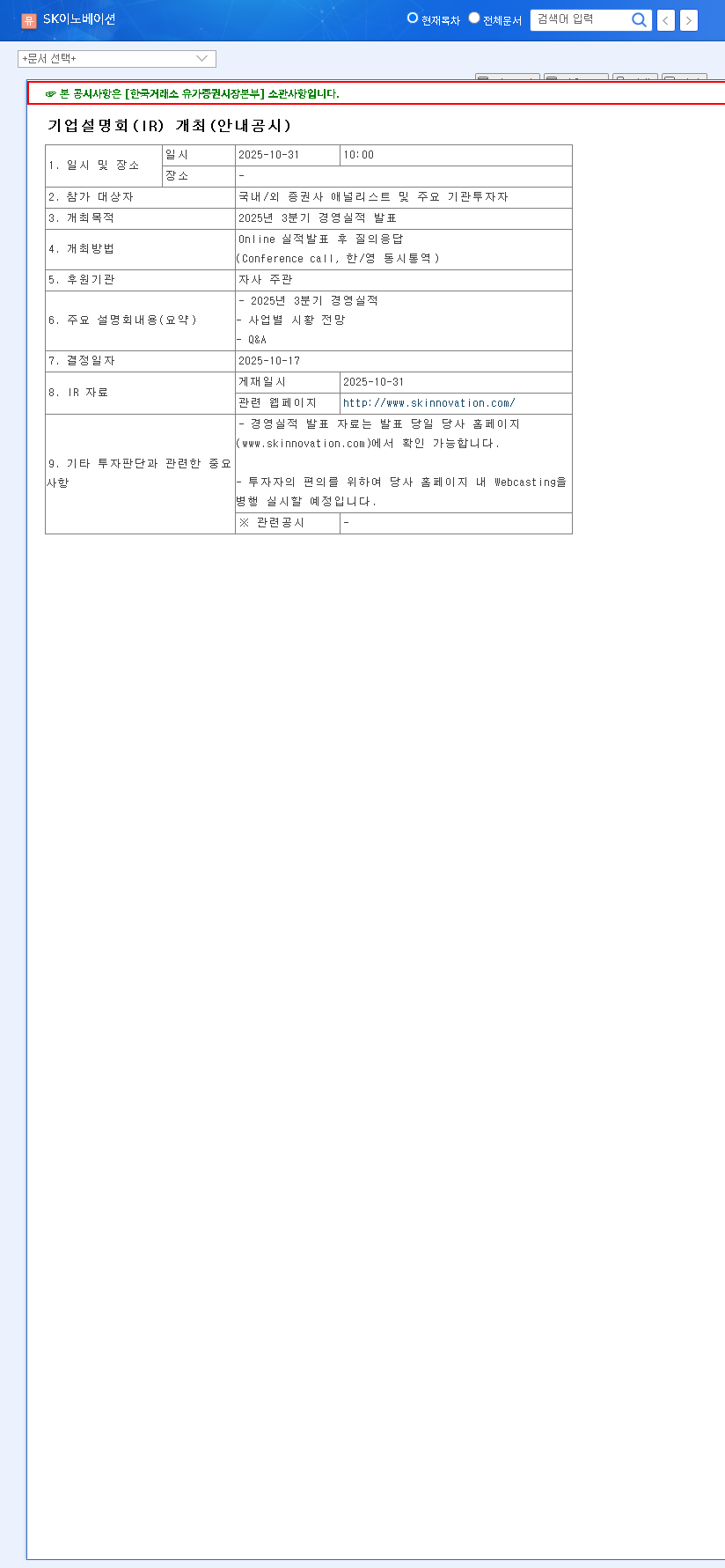

In its preliminary third-quarter announcement for 2025, SK Innovation revealed a financial narrative of contrasts. The synergy from its merger with SK E&S is clearly materializing, propelling the company’s core operations to new heights. According to the Official Disclosure, the key metrics are as follows:

- •Revenue: KRW 20.53 trillion, a robust figure that beat market consensus by a healthy 6%.

- •Operating Profit: KRW 573.5 billion, a massive earnings surprise that soared 127% above expectations, showcasing strong operational execution.

- •Net Profit: A deficit of KRW -107.9 billion, a stark shift into the red that fell significantly below forecasts.

This data paints a picture of a company with a powerful traditional energy engine that is funding a future-facing, but currently unprofitable, green technology portfolio. The core question is how long this balancing act can, or should, continue.

The Q3 results highlight a pivotal moment for SK Innovation: leveraging today’s fossil fuel profits to build tomorrow’s battery empire. The challenge is navigating the immense cash burn required for that transition without jeopardizing near-term financial stability.

Analysis: The Forces Shaping Performance

To understand the divergent paths of operating profit and net income, we must dissect the key contributors—both positive and negative.

Positive Catalysts: The Engine of the Earnings Surprise

The remarkable operating profit was not a fluke. It was driven by a confluence of strategic successes and favorable market conditions:

- •SK E&S Merger Synergies: The integration is bearing fruit, creating a diversified energy portfolio spanning LNG, hydrogen, and renewables. This has created a more stable and predictable revenue base, shielding the company from volatility in a single sector.

- •Strong Oil & Petrochemical Markets: Favorable international oil prices and robust petrochemical spreads provided a significant tailwind, boosting both revenue and margins in SK Innovation’s legacy businesses.

- •Operational Efficiency: Concerted efforts to improve efficiency and control costs, particularly within the nascent battery division, contributed positively to the overall operating profit beat.

Negative Pressures: The Drag of Future Investments

The net loss is almost entirely attributable to the aggressive, capital-intensive expansion of its battery subsidiary, SK On.

- •SK On’s Persistent Losses: The battery business is in a high-growth, high-investment phase. Accumulated operating losses and substantial depreciation costs from new plants are a primary driver of the net deficit. Improving SK On profitability is the company’s most critical short-term challenge.

- •Financial Headwinds: Beyond operational losses, external financial factors such as currency exchange rate fluctuations can impact the bottom line, offsetting some of the strong operational gains. For more on this, you can review market analysis from authoritative financial news sources.

Investor Outlook: Balancing Risk and Reward

For investors, the SK Innovation Q3 2025 earnings demand a nuanced, long-term perspective. The company is successfully funding its future growth, but this path is not without significant hurdles.

Key Growth Drivers to Watch

The long-term bull case rests on the successful execution of its green strategy. SK On’s expanding production capacity and diversification into new areas like Battery-as-a-Service (BaaS) are crucial. Furthermore, investments in battery recycling and carbon capture enhance its ESG profile and position it to capitalize on a circular economy. To better understand this sector, learn more about the global EV battery market and its key players.

Critical Risks to Monitor

Several challenges remain. The path to consistent SK On profitability is paramount. Additionally, a high debt ratio of over 200% poses a financial risk in a rising interest rate environment. Investors must also remain vigilant about macroeconomic volatility, geopolitical tensions affecting oil prices, and evolving regulations like the U.S. Inflation Reduction Act (IRA), which directly impacts battery supply chains.

Frequently Asked Questions

What caused SK Innovation’s massive operating profit surprise in Q3 2025?

The 127% beat on operating profit was driven by strong performance in its legacy oil and chemical businesses, which benefited from high global oil prices, as well as emerging synergies from its merger with SK E&S.

Why did the company post a net loss despite the strong operating profit?

The net loss was primarily due to the heavy capital expenditures and ongoing operating losses from its battery subsidiary, SK On, which is in a rapid global expansion phase. High depreciation costs associated with new factories were a major factor.

What is the strategic outlook for SK Innovation?

SK Innovation is pursuing a long-term energy transition strategy, using profits from its traditional businesses to fund its future in EV batteries and green energy. Success hinges on achieving profitability in the battery segment while managing its high debt load and navigating macroeconomic risks.