For investors closely watching SK hynix Inc., the recent announcement of a SK hynix treasury stock disposition has raised important questions. On October 29, 2025, the semiconductor giant disclosed a plan to dispose of treasury shares for employee performance incentives. This move, while seemingly standard, offers a window into management’s confidence and the company’s future trajectory. This in-depth analysis will dissect the decision, examine its short and long-term implications, and provide a clear perspective for your investment strategy in the AI era.

Deconstructing the Treasury Stock Disposition

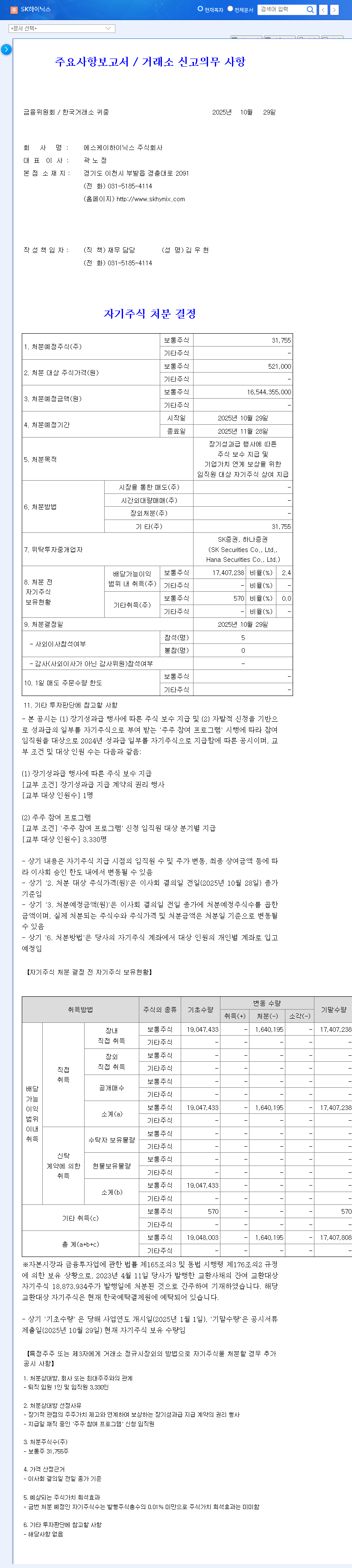

According to the Official Disclosure, SK hynix Inc. will dispose of 31,755 shares of treasury stock, valued at approximately 16.5 billion KRW. The stated purpose is strategic and forward-looking, aimed at reinforcing the company’s human capital—its most valuable asset.

Primary Objectives:

- •Long-Term Performance Incentives: Rewarding employees for achieving key milestones and fostering a culture of high performance.

- •Aligning Employee and Shareholder Interests: By providing stock-based bonuses, the company ensures that its team is directly invested in driving long-term corporate value and growth.

Context is King: SK hynix’s Unwavering Market Leadership

To fully grasp the implications of the SK hynix treasury stock disposition, we must view it against the backdrop of the company’s formidable market position. The explosive growth of the AI market has catapulted demand for high-performance memory, and SK hynix is at the epicenter of this revolution. The company’s fundamentals are a testament to its technological prowess and financial stability.

- •Dominance in AI Memory: As a leader in High Bandwidth Memory (HBM), including the world’s first mass production of HBM3E, SK hynix is a primary beneficiary of the AI boom. For more details, you can explore our deep dive into SK hynix’s HBM technology.

- •Record-Breaking Financials: The company recently posted its highest-ever quarterly revenue and operating profit, with a robust debt-to-equity ratio of 48.13%.

- •Strategic Expansion: With the completion of the Icheon M16 fab and plans for the Cheongju M15X DRAM base, the company is proactively expanding capacity to meet future demand.

Investor Impact Analysis: Stock Price & Corporate Value

Short-Term Impact: A Bullish Signal

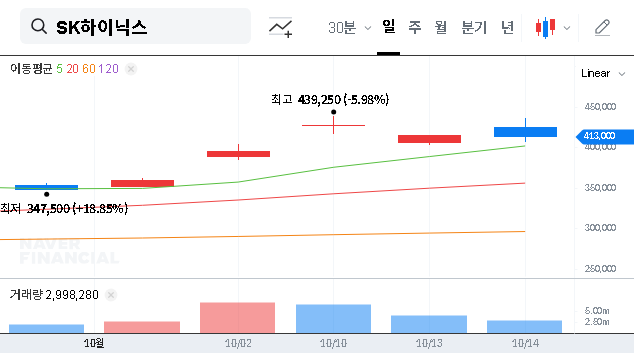

From a supply and demand perspective, the disposition of 31,755 shares is minuscule compared to the approximately 730 million outstanding shares. Therefore, its direct impact on stock price dilution or supply pressure is negligible. The real story lies in the signal it sends to the market.

The announced disposition price of approximately KRW 519,655 per share is significantly higher than the current market price. This isn’t a typo; it’s a powerful statement. It suggests that the compensation is based on a valuation reflecting strong confidence in the company’s anticipated future growth and intrinsic value, a profoundly positive indicator for investors.

Long-Term Impact: Securing Future Competitiveness

In the hyper-competitive semiconductor industry, attracting and retaining elite talent is paramount. This treasury stock disposition is a strategic investment in human capital. A well-structured, transparent employee compensation system directly contributes to long-term value by boosting morale, spurring innovation, and reducing talent churn. This ultimately strengthens SK hynix’s competitive moat and ensures it remains at the forefront of technological advancement.

External Factors & Macroeconomic Headwinds

While the company-specific news is positive, a prudent SK hynix stock analysis must account for external variables. Investors should continue to monitor the broader economic landscape, as outlined in authoritative reports like the latest semiconductor market forecast from industry analysts.

- •Currency Fluctuations: High volatility in the KRW/USD exchange rate can impact earnings and profitability.

- •Interest Rate Environment: Global monetary policy shifts can affect financing costs and overall market sentiment.

- •Commodity Prices: Trends in raw material and energy prices can influence production costs and signal broader economic trends.

Conclusion: A Confident Step Forward

The 2025 SK hynix treasury stock disposition should be viewed by investors not as a risk, but as a reaffirmation of the company’s strategy and a signal of management’s deep confidence in its long-term value. Backed by industry-leading technology and robust financial health, SK hynix is well-positioned to continue its growth trajectory. While macroeconomic vigilance is always necessary, this internal move reinforces the positive investment thesis for the company.

Disclaimer: This report is prepared based on the information provided and does not assume any responsibility for investment decisions. Investment decisions should be made through individual judgment and further analysis.