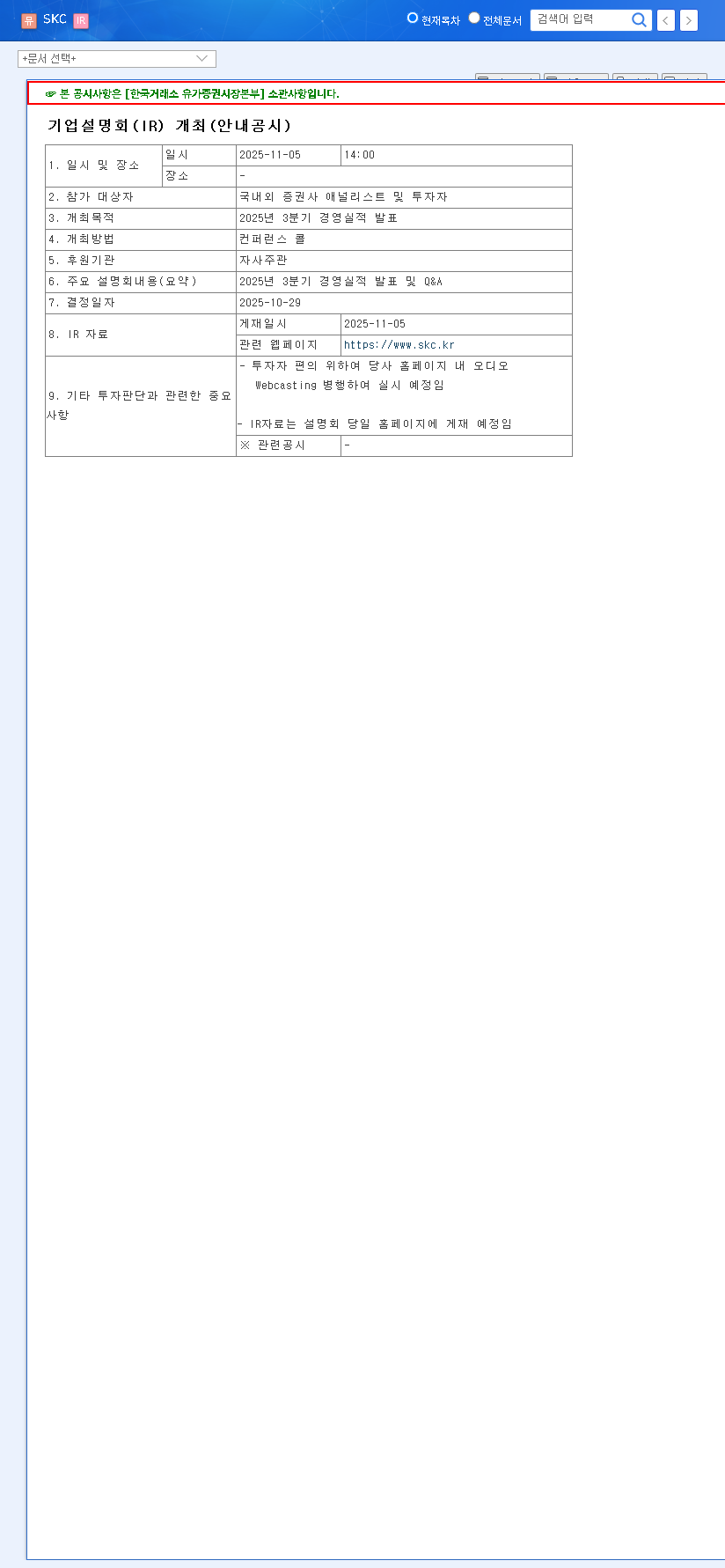

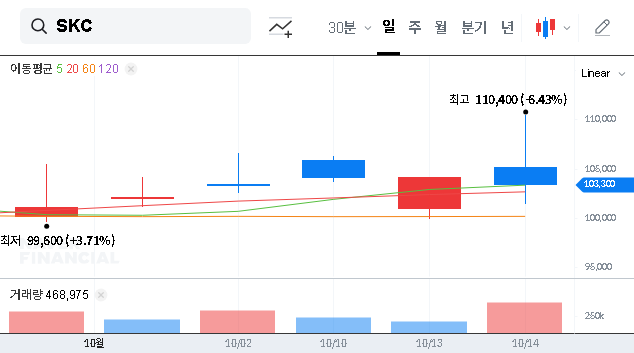

As the November 5, 2025, conference approaches, the market is keenly anticipating the SKC LTD Q3 2025 earnings announcement. This Investor Relations (IR) event is far more than a routine financial report; it represents a critical opportunity for investors to gauge the momentum of SKC’s ambitious growth strategy, particularly in its battery and semiconductor materials divisions. This comprehensive analysis provides a forward-looking SKC LTD investment outlook, dissecting each business segment, evaluating financial health, and outlining potential market impacts to help you formulate a smart investment strategy.

We will explore how SKC LTD’s unique competitive advantages are positioned against global economic volatility and what key metrics investors should be monitoring. From the high-growth trajectory of its copper foil business to the strategic strengthening of its semiconductor portfolio, this article offers a complete picture of what to expect.

Deep Dive into SKC LTD’s Core Business Segments

SKC LTD’s growth engine is powered by three primary business segments, each with distinct strengths and challenges. Understanding these is fundamental to a complete SKC LTD stock analysis.

Battery Materials (SK Nexilis): The EV Powerhouse

The crown jewel of SKC’s portfolio is its battery materials division, led by SK Nexilis. This segment’s phenomenal growth is directly tied to the booming global electric vehicle (EV) market, which drives immense demand for its core product: copper foil. SK Nexilis possesses world-class technology, including the mass production of ultra-thin 4㎛ copper foil, a critical component for high-density EV batteries. The ongoing capacity expansion with new plants in Malaysia and Poland is set to solidify its global leadership. However, this aggressive expansion comes with significant initial investment costs and exposes the company to intense competition and the volatility of raw material prices.

Chemical Business (SK picglobal): Stable and Eco-Friendly

While not as high-growth as battery materials, the chemical business provides a bedrock of stable profitability. As the sole domestic producer of Propylene Glycol (PG), SK picglobal holds a strong market position. A key competitive advantage is its eco-friendly HPPO manufacturing process, which appeals to an increasingly environmentally conscious market. The primary risk for this segment lies in its sensitivity to fluctuations in downstream industries, which can impact demand and pricing.

Semiconductor Materials (ISC & SK Enpulse): Riding the AI Wave

The strategic acquisition of ISC has significantly bolstered SKC’s semiconductor materials portfolio. ISC’s dominant position in the test socket market is a massive asset, especially with the explosive growth of the AI semiconductor industry. This synergy, combined with SK Enpulse’s strengths in Blank Masks and CMP Slurry, creates a formidable presence. Investors looking for insights should read our complete guide to the semiconductor supply chain. The main challenge remains the cyclical nature of the semiconductor industry and the constant threat of new competitors entering the market.

Financial Health: Analyzing the Numbers

The H1 2025 report revealed a nuanced financial picture. A 6.2% year-over-year revenue decrease was primarily due to a strategic restructuring of the chemical business, while the battery materials segment showed robust growth. The consolidated operating loss of KRW 144.6 billion can be interpreted as a temporary consequence of the massive capital expenditures required to build out future capacity. These investments are essential for long-term dominance.

The company’s debt-to-equity ratio stood at a manageable 188.5%, indicating a sound underlying financial structure. Proactive measures, like issuing exchangeable bonds, demonstrate a commitment to shoring up the balance sheet. While operating cash flow was negative, overall cash reserves increased, reflecting a necessary phase of investment for securing long-term growth. For a detailed breakdown, please review the Official Disclosure: Click to view DART report.

SKC LTD is at a pivotal crossroads, balancing aggressive, large-scale investments in future growth sectors with the need to manage near-term financial pressures. The Q3 2025 earnings report will be a key indicator of how well they are navigating this balance.

Market Outlook: Post-IR Opportunities and Risks

The SKC LTD Q3 2025 earnings call will likely act as a major catalyst for the stock. Here are the potential positive and negative impacts investors should anticipate.

- •Positive Catalysts: Stronger-than-expected performance from SK Nexilis, driven by its expanded capacity, could significantly boost revenue and investor confidence. Furthermore, any concrete updates on new ventures, such as the timeline for Absolics’ semiconductor glass substrates, could ignite positive sentiment by providing clear visibility into future growth drivers.

- •Risk Factors: Macroeconomic headwinds, including a global economic slowdown or persistent high interest rates, could dampen demand in the EV and semiconductor markets. Intensifying competition in the battery materials space could pressure margins, while the financial burden of new investments remains a key variable. Finally, if the results or management’s guidance fall short of market expectations, it could trigger a negative stock price reaction.

Strategic Investment Thesis and Conclusion

Our overall SKC LTD investment outlook remains positive (BUY), predicated on the company’s strengthening global leadership in essential, high-growth industries. The upcoming SKC LTD IR will be a crucial event to confirm this thesis.

Long-term investors should focus on the operational progress of the new manufacturing facilities and the development pipeline for next-generation materials. Short-term traders should pay close attention to the profitability trends in the battery segment and any forward-looking guidance from management. Key areas to monitor during the call include the profitability improvement of SK Nexilis, the growth acceleration in semiconductor materials, and specific updates on new business ventures. By carefully analyzing these factors, investors can make an informed decision on how to position themselves for SKC LTD’s evolving growth story.