The recent announcement of the Greenresource palm mixture contract has sent ripples through the investment community. Valued at a substantial ₩8.5 billion, this deal with Miracle Energy Co., Ltd. represents a significant portion of Greenresource’s projected revenue. For investors, this news raises a critical question: is this a temporary lifeline for a company facing performance challenges, or the first step in a bold new strategic direction? This comprehensive Greenresource investment analysis will dissect the contract’s implications, evaluate the company’s underlying fundamentals, and provide an actionable strategy for navigating the opportunities and risks tied to Greenresource stock.

Deconstructing the Greenresource Palm Mixture Contract

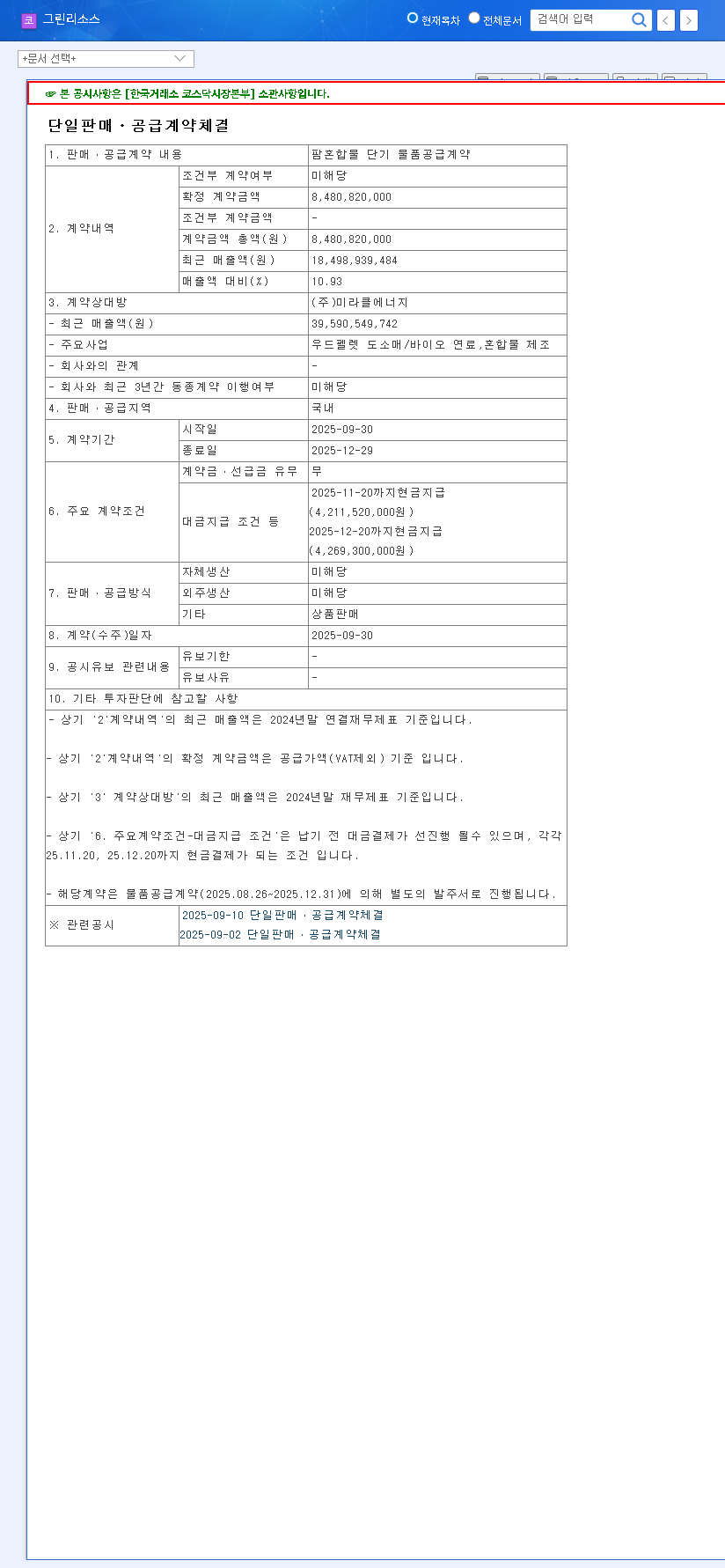

On the surface, the deal is a clear positive. It injects significant, guaranteed revenue into the company over a short period. However, the nature of the product—’palm mixture’—is what creates uncertainty, as it seemingly lies outside Greenresource’s established expertise in high-tech coatings and equipment. The full details of the agreement can be reviewed in the Official Disclosure filed with DART.

Key Contract Details at a Glance

- •Counterparty: Miracle Energy Co., Ltd.

- •Contract Value: ₩8.5 Billion (approx. 10.93% of estimated 2024 revenue)

- •Product: Short-term supply of ‘palm mixture’

- •Contract Period: September 30, 2025 – December 29, 2025

This contract provides a much-needed short-term revenue boost. The critical task for investors now is to determine if ‘palm mixture’ is a profitable, sustainable diversification or a high-risk, low-synergy distraction from the core business.

Short-Term Gains vs. Long-Term Uncertainty

Immediate Financial Impact

The ₩8.5 billion deal, concentrated within a single quarter, will lead to rapid revenue recognition. This influx of cash is expected to significantly improve Greenresource’s short-term liquidity and cash flow, providing operational stability and potentially boosting investor sentiment. It serves as a welcome counter-narrative to the company’s recent performance slump and could positively influence the Greenresource stock price in the near term.

The ‘Palm Mixture’ Enigma: A New Growth Engine?

The core of the uncertainty lies with the product itself. ‘Palm mixture’ is not related to Greenresource’s primary operations in semiconductor/display coating technology or superconducting wire equipment. This suggests a strategic pivot towards business diversification. While diversification can reduce dependency on a single market, it also introduces execution risk. Investors must question the company’s expertise in this new commodity market, the stability of its supply chain, and the ultimate profitability of the venture. This is a pivotal point in any Greenresource investment analysis.

Fundamental Health Check: Opportunities and Threats

Current Strengths and Future Drivers

- •Improved Financial Structure: A recent ₩20 billion fundraising via convertible bonds has fortified the company’s balance sheet for new investments.

- •Expanded Production Capacity: The new headquarters, completed in March 2024, is set to increase future production capabilities for core products.

- •Long-Term Growth Potential: The company remains positioned to benefit from wider EUV process adoption in semiconductors and the growth of the superconducting wire market.

Significant Risk Factors to Monitor

- •Performance and Profitability: 2024 has seen revenues fall below forecasts and operating margins shrink due to rising costs and expenses.

- •Customer Concentration: A heavy reliance on a single major client (‘Company A’) creates significant revenue risk if that relationship falters.

- •Supply Chain Dependency: The company’s reliance on China for key raw materials like yttrium oxide powder exposes it to geopolitical and price volatility risks.

Action Plan for Investors

Given the mix of positive momentum from the Greenresource palm mixture contract and underlying fundamental risks, a prudent approach is required. Macroeconomic trends, such as exchange rate volatility, could either benefit exports or increase the cost of imported raw materials for the new venture, a factor that leading financial outlets like Reuters continually monitor.

Investors should consider the following steps:

- •Demand More Clarity: Seek additional information from company IR disclosures and news reports about the specifics of the palm mixture business, including sourcing, margins, and long-term strategy.

- •Analyze Profitability: Go beyond the headline revenue number. A thorough analysis must estimate the costs associated with this new supply chain to determine its actual contribution to net profit.

- •Monitor Core Business Health: The long-term value of Greenresource stock still hinges on its primary tech segments. For more on this, see our guide to semiconductor industry investments.

In conclusion, the ₩8.5 billion contract offers a compelling, positive catalyst. However, it also introduces significant uncertainty. The medium-to-long-term trajectory of Greenresource will be defined by its ability to execute on this new venture profitably while simultaneously reviving its core technology business. Cautious optimism, backed by rigorous due diligence, is the most sensible path forward.