In the high-stakes world of biotechnology, a single supply contract can signal a major shift in a company’s trajectory. For Prestige BioPharma Limited, a recent deal has done just that, capturing the market’s attention. The company announced a KRW 1.9 billion agreement to supply pharmaceutical raw materials to Russia, a move that prompts critical questions for investors. Is this a powerful catalyst for long-term growth, or does it introduce unacceptable risk? This comprehensive Prestige BioPharma analysis will dissect the contract, evaluate the company’s fundamentals, and provide a clear outlook for potential investors.

Unpacking the KRW 1.9 Billion Russia Contract

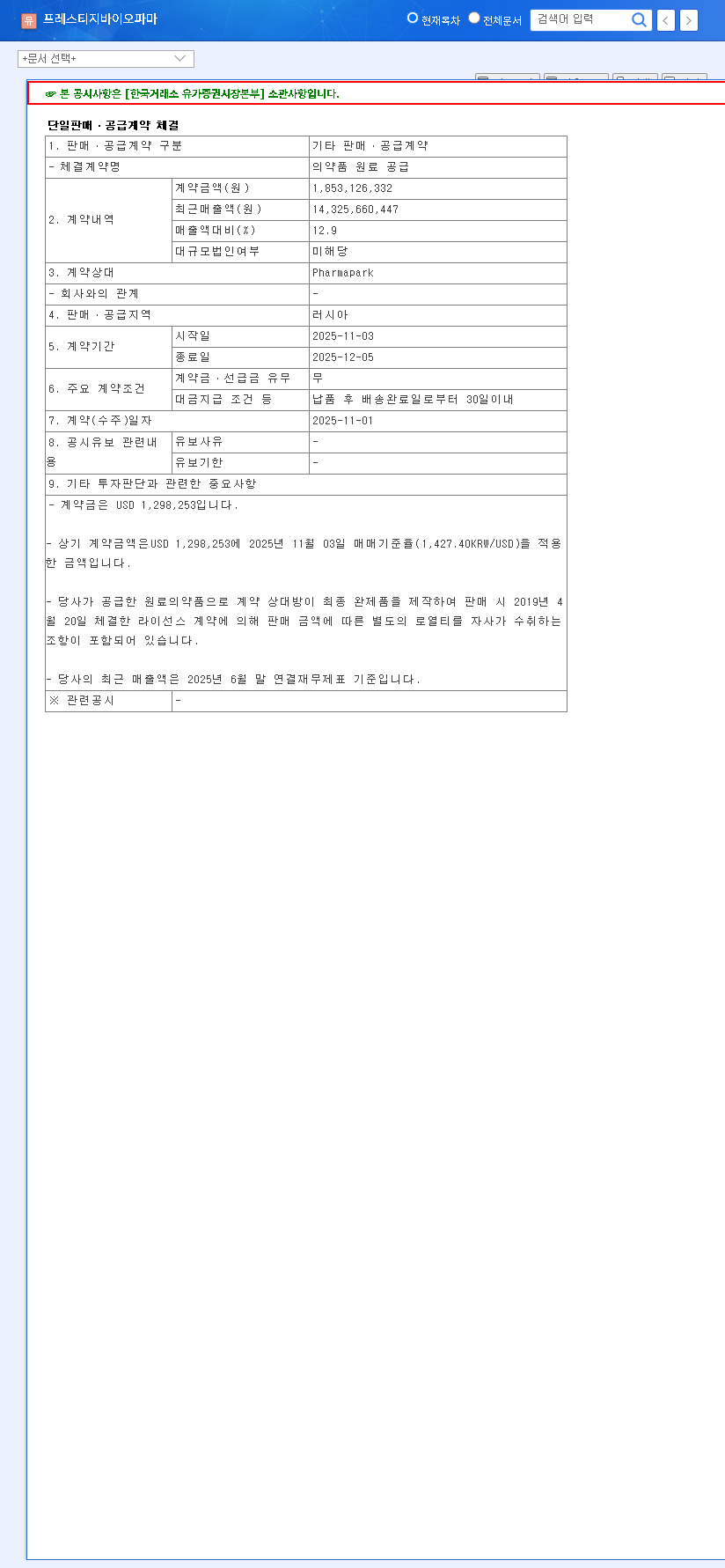

On November 4, 2024, Prestige BioPharma disclosed the signing of a significant supply agreement with the Russian firm Pharmapark. According to the Official Disclosure, the contract is valued at KRW 1.9 billion, representing a substantial 12.9% of the company’s most recent annual revenue. The deal is slated for a rapid execution timeline, spanning just one month from November 3, 2025, to December 5, 2025.

While the immediate revenue boost is notable, the strategic importance of this Prestige BioPharma Russia contract cannot be overstated. It marks the company’s formal entry into a new, large market, potentially acting as a gateway for further expansion into the Commonwealth of Independent States (CIS) region. This move demonstrates an aggressive growth strategy and an ability to secure international partnerships.

This contract is more than just a short-term revenue injection; it’s a strategic beachhead in a new market, signaling Prestige BioPharma’s global ambitions and operational capabilities.

Core Business Fundamentals: A Two-Pillar Strategy

To understand the long-term potential of Prestige BioPharma, we must look beyond a single contract to its foundational business pillars: its proprietary biosimilar pipeline and its stable contract manufacturing operations.

Tuznue (HD201): The Flagship Growth Driver

The company’s core asset is Tuznue (HD201), a biosimilar to Roche’s blockbuster cancer drug, Herceptin (trastuzumab). Biosimilars are highly similar, cost-effective versions of approved biologic drugs, and their adoption is a major trend in global healthcare. For more on this, you can review information on biologics from the World Health Organization. The recent European market approval for Tuznue is a monumental achievement, validating its quality and unlocking a massive revenue stream. This approval provides the commercial foundation that makes market expansions, like the one in Russia, possible and credible.

The CDMO Business: A Stabilizing Force

Complementing its high-growth pipeline is the company’s subsidiary, Prestige Biologics, which operates a robust Contract Development and Manufacturing Organization (CDMO business). This division provides development and manufacturing services to other pharmaceutical companies, generating a stable and predictable revenue stream. This income helps offset the high costs and long timelines associated with R&D, providing a financial cushion and de-risking the company’s overall profile. Understanding the role of CDMOs in the pharma industry is key to appreciating this balanced model.

Financial Health and Risk Analysis

Despite its strategic successes, a thorough biotech stock analysis requires a sober look at the financial risks. Prestige BioPharma is characteristic of a growth-stage biotech firm, with significant challenges to manage.

- •R&D and Cost Burden: The company continues to post operating losses, largely due to heavy investment in research and development for its pipeline and high selling, general, and administrative (SG&A) expenses. This cash burn is a critical metric to monitor.

- •Debt Management: A high debt-to-equity ratio remains a financial risk. However, it is encouraging that this ratio has been on a downward trend since 2024, indicating improved financial discipline and management.

- •Geopolitical & Market Risk: Entering the Russian market introduces unique challenges, including potential economic sanctions, political instability, and significant currency exchange volatility (USD/KRW/RUB). These macroeconomic factors can directly impact the profitability of this and future contracts.

Action Plan for Investors

The Prestige BioPharma Russia contract is a clear positive signal, but prudent investment requires ongoing vigilance. This is not a ‘set it and forget it’ stock. Investors should focus on the following key areas:

Key Monitoring Points:

- •Short-Term Catalysts: Monitor the successful execution and revenue recognition from the current Russian contract. Look for announcements of follow-on orders or expansion into adjacent markets.

- •Long-Term Value Drivers: Track the commercialization progress and sales figures for Tuznue HD201 in Europe. Pay close attention to the growth and profitability of the CDMO business unit in quarterly reports.

- •Financial Health Metrics: Keep a close eye on the company’s cash burn rate, operating margins, and progress in further reducing its debt-to-equity ratio. Financial stability is paramount for long-term success.

In conclusion, Prestige BioPharma presents a compelling, albeit complex, investment case. The company holds significant long-term potential, but this is balanced by tangible financial and geopolitical risks. Cautious, well-informed optimism is the recommended approach.