Investors in SIMMTECH Co., Ltd. (222800) are closely watching the company’s latest strategic financial maneuver: the SIMMTECH conversion rights exercise. This development, which introduces over 1.6 million new shares, has sparked a critical debate among stakeholders about the balance between short-term stock dilution and the potential for long-term, sustainable growth. Is this a temporary headwind or a catalyst for future expansion? This comprehensive analysis will unpack the details, weigh the risks against the rewards, and provide a strategic framework for your investment decisions.

Understanding the SIMMTECH Conversion Rights Exercise

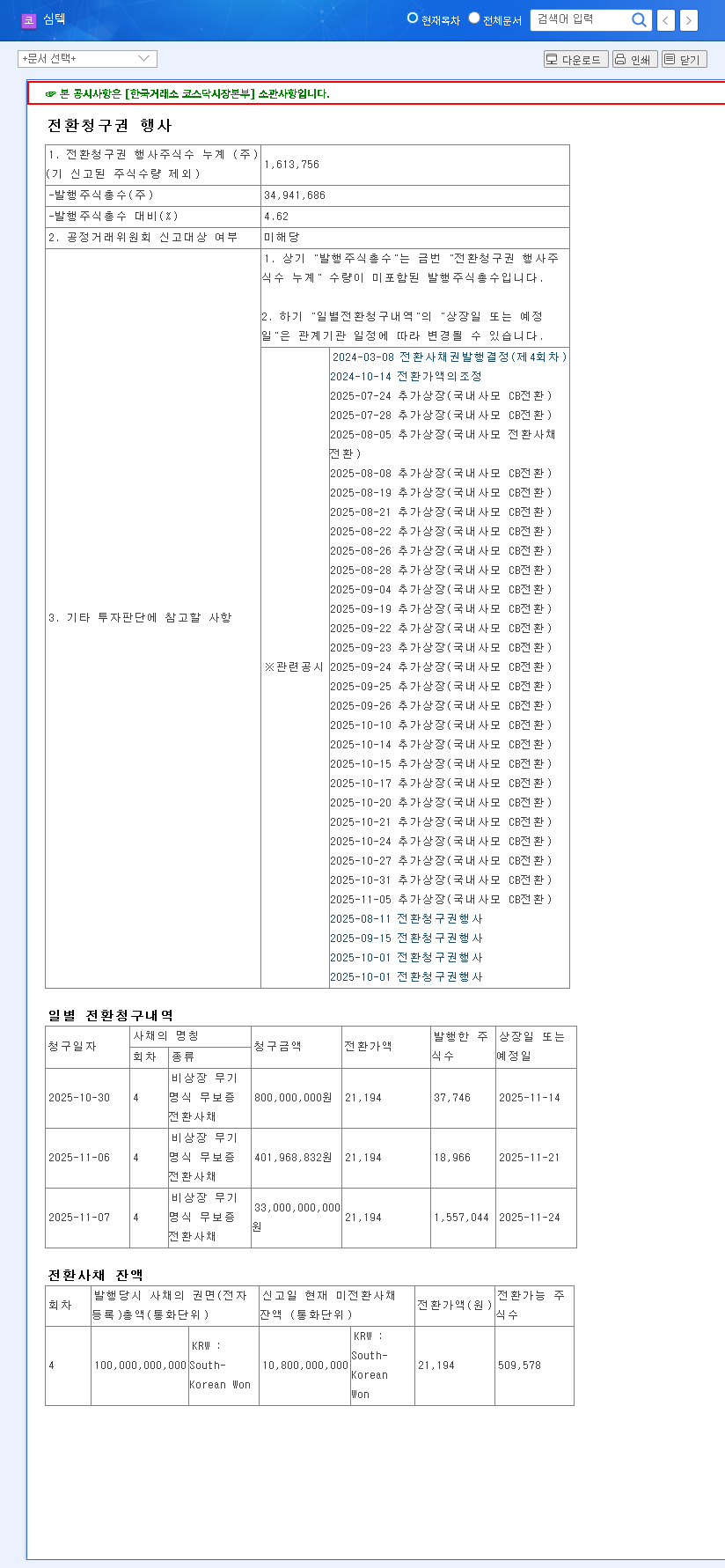

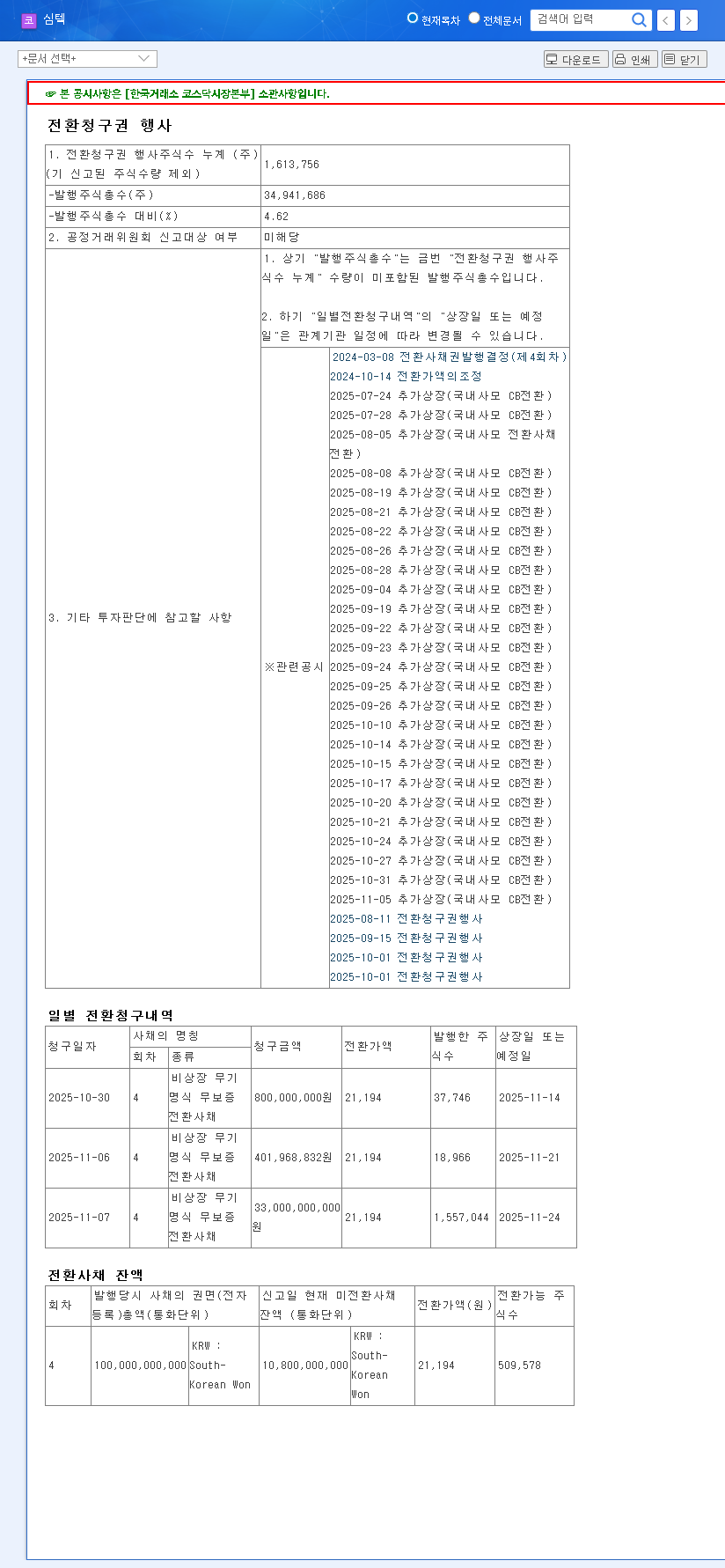

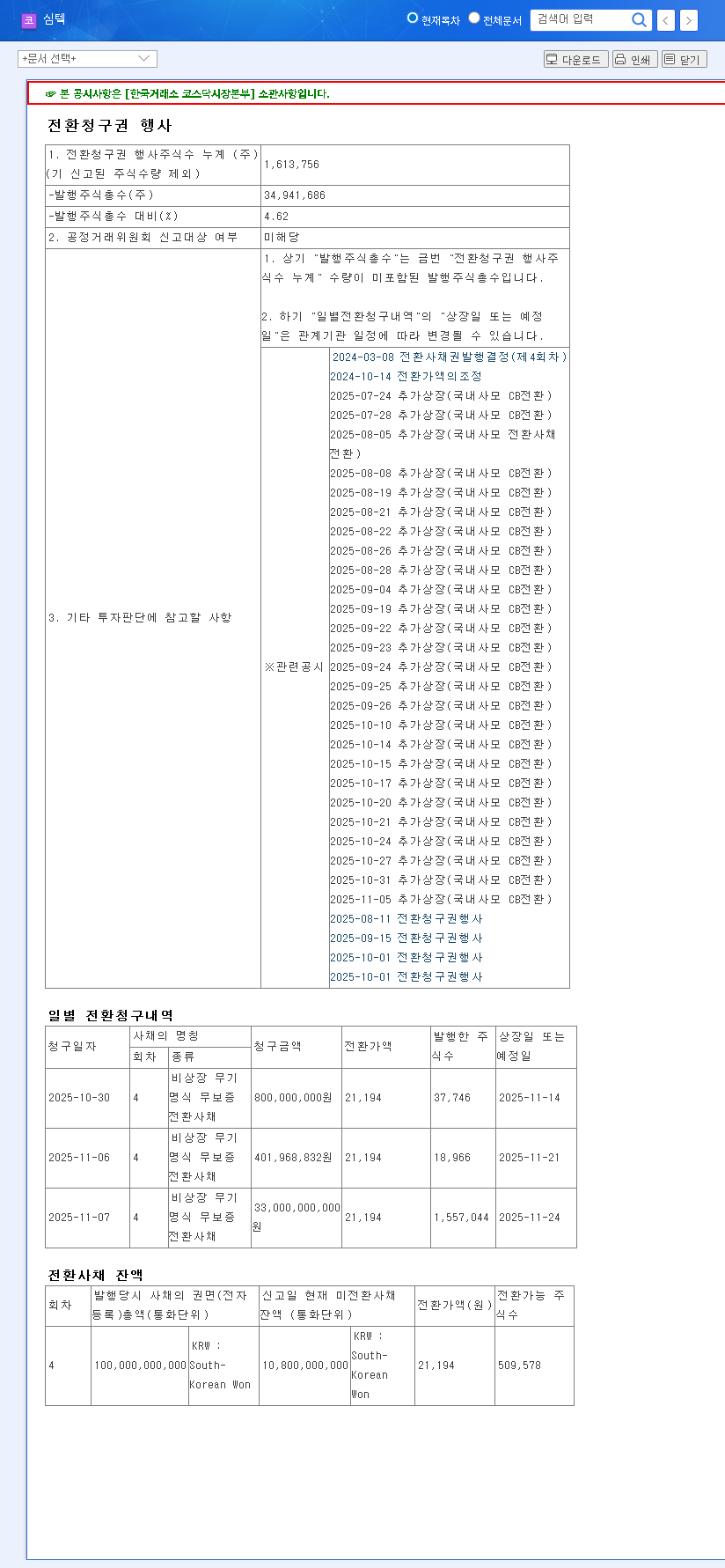

At its core, this event involves the conversion of debt into equity. Holders of SIMMTECH’s Convertible Bonds (CBs) are choosing to swap their bonds for company stock at a predetermined price. According to the Official Disclosure on DART, a total of 1,613,756 new shares (representing 4.62% of market capitalization) are set to be listed. For investors, understanding what convertible bonds are is crucial; they are a hybrid financial instrument that offers bond-like income with the potential for stock-like appreciation.

The new shares are scheduled to enter the market on the following dates:

- •November 24, 2025: 1,557,044 shares

- •November 21, 2025: 18,966 shares

- •November 14, 2025: 37,746 shares

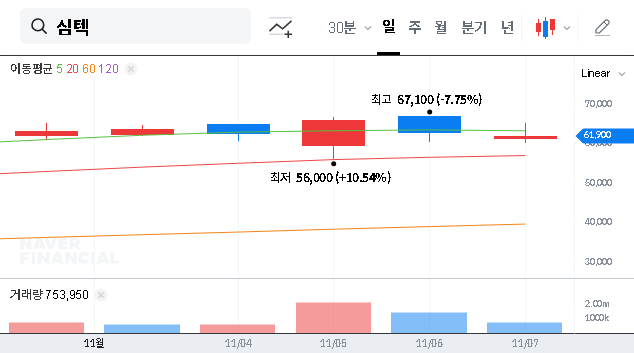

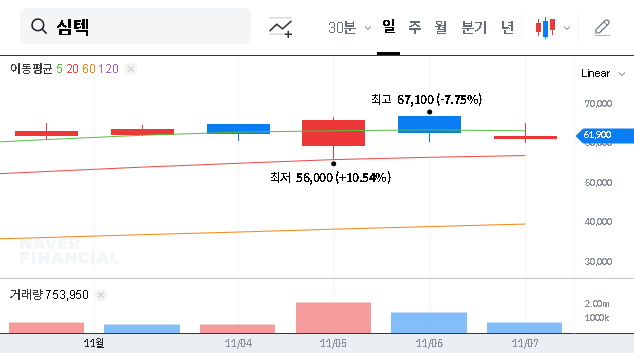

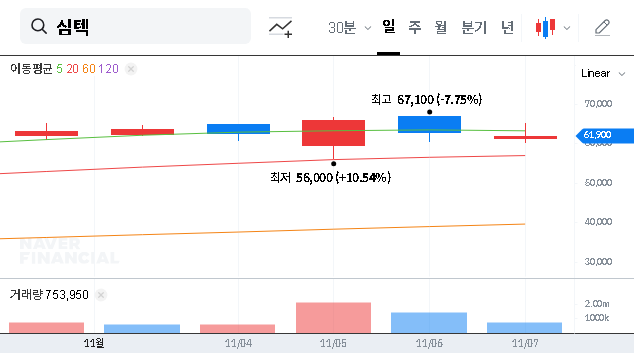

The conversion price is set at KRW 21,194, which is notably higher than the stock’s price of KRW 16,975 at the time of the announcement. This premium suggests that bondholders see long-term value, but the influx of new shares could create a supply overhang in the near term.

SIMMTECH Stock Analysis: Strengths vs. Risks

Positive Fundamentals: A Foundation for Growth

Despite market headwinds, SIMMTECH’s core business remains strong. The company has demonstrated consistent revenue growth, fueled by the booming semiconductor and IT device markets. Securing major global clients like Samsung Electronics and SK Hynix provides a stable demand base and reinforces its position as a technological leader. Furthermore, the strategic expansion into the high-value-added System IC business is a key driver that could significantly enhance future profitability and establish new growth engines for the company.

Financial Headwinds: Key Risk Factors

However, a complete SIMMTECH stock analysis must acknowledge the risks. The company’s consolidated operating and net incomes have recently been in the red, signaling a need for improved cost management. The most significant concern is its financial leverage; a debt-to-equity ratio of 243.51% indicates a heavy reliance on borrowing, which can amplify risk. While converting debt to equity can alleviate this pressure, the underlying financial structure requires careful monitoring by investors.

The core challenge is balancing the short-term stock dilution risk against the long-term strategic benefits of a stronger balance sheet and newly funded growth initiatives.

Investment Strategy in Light of the News

The SIMMTECH conversion rights exercise introduces both uncertainty and opportunity. A prudent investment strategy should be multifaceted, considering the immediate market reaction and the company’s long-term trajectory. It’s important to analyze these events within the broader context of current semiconductor industry trends.

Key Factors to Monitor

Investors should keep a close watch on the following key performance indicators in the upcoming quarters:

- •Profitability Metrics: Look for signs of a turnaround in operating profit and net income. Is the expansion into the System IC business translating into higher margins?

- •Financial Health: Track the debt-to-equity ratio and other leverage indicators post-conversion. A meaningful reduction would be a strong positive signal.

- •Market Reaction: Observe how the market absorbs the new supply of shares. Is the selling pressure short-lived, or does it signal a more prolonged period of consolidation?

- •Macroeconomic Factors: Continue to monitor interest rates, exchange rates, and global semiconductor demand, as these will all impact SIMMTECH’s performance.

In conclusion, while the issuance of new shares presents a clear short-term stock dilution risk, it is also a vital part of SIMMTECH’s long-term strategy to deleverage its balance sheet and fund future growth. For long-term investors, the key is to look beyond the immediate price action and focus on whether the company can successfully execute its strategic pivot toward higher-margin businesses and improved financial stability.