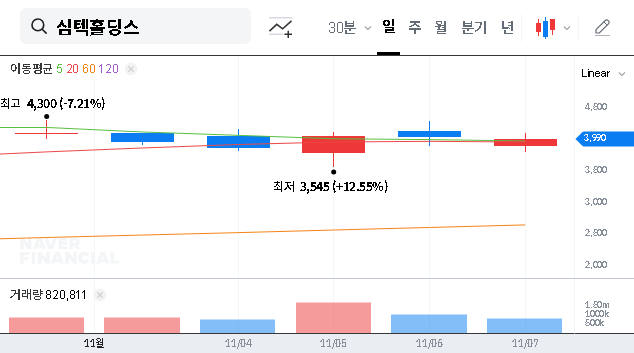

The future of SIMMTECH HOLDINGS stock hangs in the balance as the company prepares for its pivotal Investor Relations (IR) briefing on November 17, 2025. As a specialized manufacturer of semiconductor PCB technology, SIMMTECH HOLDINGS faces a critical juncture. After a period of declining revenue and significant operating losses, this event represents a crucial opportunity to restore investor confidence and chart a new course for growth. Investors are keenly watching, and the details presented could either trigger a significant rally or deepen existing concerns.

This comprehensive SIMMTECH HOLDINGS analysis will delve into the company’s current financial health, the macroeconomic headwinds it faces, and the key factors that will determine its stock performance post-briefing. We will explore both the potential catalysts for a positive turnaround and the risks that could lead to further decline, providing essential insights for any stakeholder.

Current Financial State: A Deep Dive

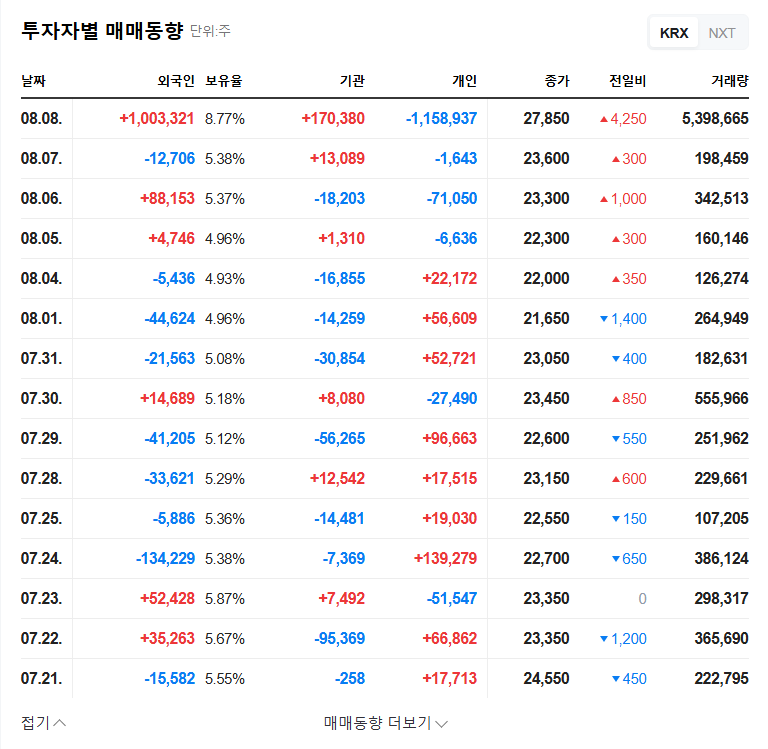

To understand the significance of the upcoming SIMMTECH HOLDINGS IR event, we must first examine the challenging financial landscape the company navigates. According to its preliminary financial results, which will be discussed in detail at the briefing (see the Official Disclosure), several key metrics are raising red flags for investors.

- •Declining Revenue: Consolidated revenue for the first half of 2025 fell to KRW 692.47 billion. This year-over-year decrease is primarily attributed to a significant slump in its core PCB business unit.

- •Persistent Operating Losses: The company reported a consolidated operating loss of KRW -40.54 billion for H1 2025. Although this is a slight improvement from the previous year, mounting costs continue to pressure profitability.

- •High Debt-to-Equity Ratio: Financial leverage is a major concern, with the debt-to-equity ratio climbing to 464.12%. This increase from 427.28% at the end of the prior year highlights a growing reliance on borrowings and bonds.

- •Liquidity Strain: A current ratio of approximately 51% suggests potential difficulties in meeting short-term financial obligations, a critical point for risk-averse investors.

SWOT Analysis: Challenges vs. Opportunities

The outlook for SIMMTECH HOLDINGS stock is a classic case of weighing internal weaknesses against external opportunities. A balanced view is essential for a sound investment strategy.

Strengths and Opportunities

Despite its financial troubles, the company possesses core strengths. Its specialization in semiconductor PCB technology, a diversified customer base, and a commitment to R&D (3.50% of revenue) are significant assets. These strengths are well-positioned to capitalize on a positive industry outlook. The broader PCB market is projected to grow by 7.6% in 2025, according to industry market reports. The expansion of the high-performance System IC market, in particular, offers a substantial growth avenue that aligns perfectly with the company’s strategic focus.

Weaknesses and Threats

The primary weaknesses are internal: the high debt load and negative cash flow. These vulnerabilities are amplified by external macroeconomic threats. Persistently high interest rates in the US and Europe increase financial costs, while KRW/USD exchange rate volatility presents a double-edged sword—potentially boosting export competitiveness but also raising raw material costs and debt repayment burdens. For more context on navigating such markets, investors can explore our guide on investing in the global semiconductor sector.

The market is no longer looking for promises; it is demanding a clear, actionable roadmap. The success of the SIMMTECH HOLDINGS IR will be measured by the credibility and concreteness of its financial restructuring and growth strategy.

The IR Briefing: Potential Scenarios and Stock Impact

The upcoming investor briefing is the primary catalyst that will dictate near-term stock performance. Here’s what investors will be looking for and how the outcomes could influence the stock price.

Positive Catalysts (Bull Case)

- •Clear Turnaround Plan: A detailed strategy with timelines for improving profitability, such as securing new orders from major clients or effective cost-reduction measures.

- •Debt Restructuring Roadmap: A credible plan to improve the balance sheet, possibly through asset sales or strategic capital raising, would significantly de-risk the stock.

- •System IC Dominance: Showcasing tangible progress and a forward-looking strategy to capture a larger share of the high-growth System IC market.

Negative Factors (Bear Case)

- •Vague or Ambiguous Outlook: A failure to provide specific, measurable goals or a forecast of continued underperformance would likely trigger a sell-off.

- •Inadequate Financial Solutions: If the high debt ratio and financial costs are not addressed with a clear solution, concerns about solvency could intensify.

- •Overemphasis on Headwinds: Focusing too much on negative macroeconomic factors without presenting proactive mitigation strategies could signal a lack of control to investors.

Conclusion: An Inflection Point for SIMMTECH HOLDINGS Stock

The November 17, 2025, IR briefing is more than a standard financial update; it is an inflection point for SIMMTECH HOLDINGS. The company’s management has the opportunity to change the narrative from one of financial distress to one of strategic recovery and future growth. Investors should scrutinize the realism and feasibility of the plans presented. A convincing and transparent presentation could unlock significant value and set SIMMTECH HOLDINGS stock on a path to recovery. Conversely, any disappointment could lead to sustained downward pressure. Careful analysis of the IR content will be paramount for making an informed investment decision.