The latest disclosure surrounding TCK (064760) stock has captured the attention of the investment community. A recent filing from Baring Asset Management revealed a slight adjustment in their holdings. While the change itself is minor, it prompts a crucial question: Is this a routine portfolio rebalancing, or does it signal a deeper sentiment about TCK’s future trajectory? This comprehensive TCK stock analysis will explore the company’s robust fundamentals, its dominant position in SiC technology, and what this move by a major institutional investor truly means for your investment strategy.

We’ll break down the financial health, technological advantages, and potential risks, providing a clear outlook on what to expect from TCK in the coming months and years.

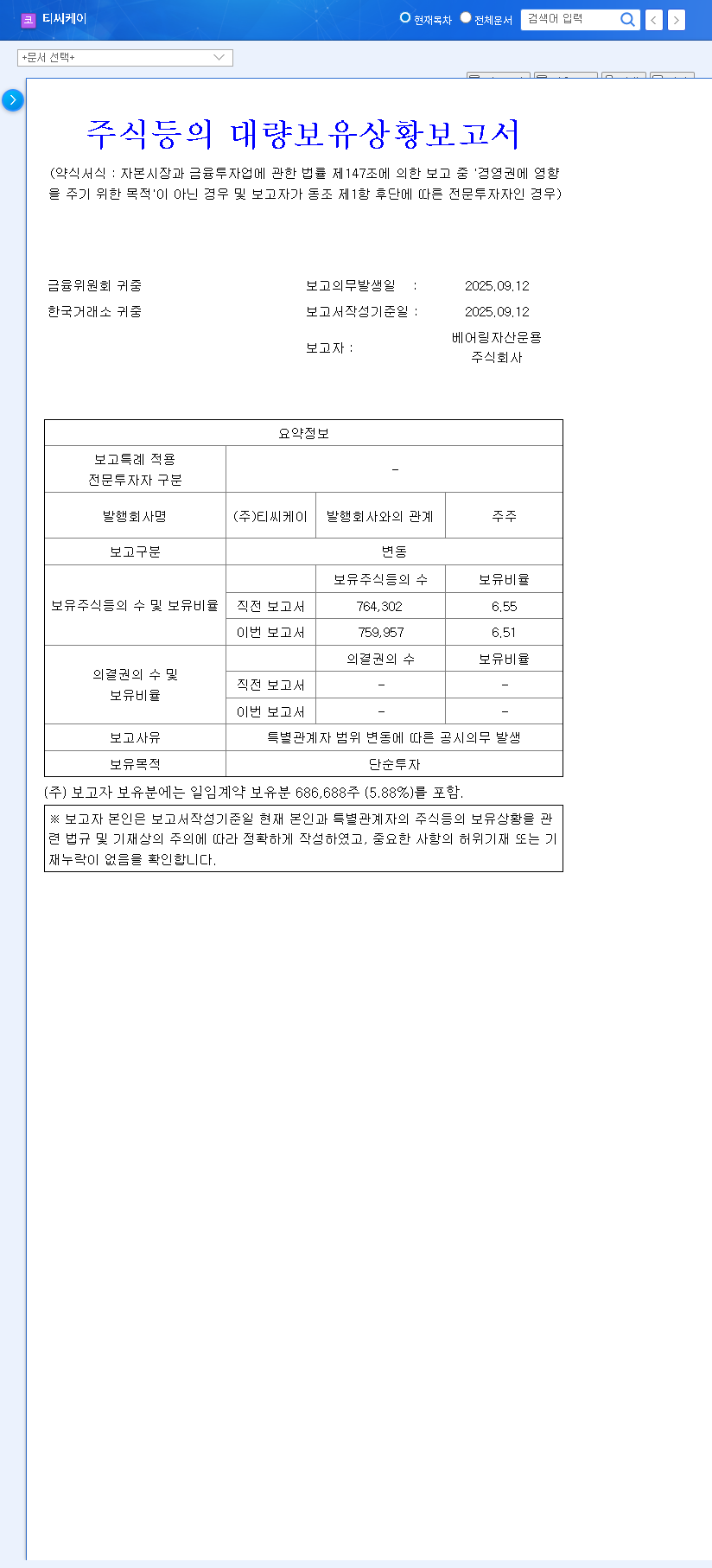

The Catalyst: Baring Asset Management’s Holding Report

On October 2, 2025, a mandatory disclosure was filed regarding large shareholdings in TCK (064760). The report, submitted by Baring Asset Management, outlined a subtle shift in their position. Here are the critical details from the Official Disclosure:

- •Reporting Entity: Baring Asset Management (Republic of Korea)

- •Purpose of Holding: Clarified as ‘Simple Investment’.

- •Stake Change: A fractional decrease from 6.55% to 6.51% (a 0.04 percentage point reduction).

- •Reason for Report: An obligation triggered by changes in the scope of related parties.

The key takeaway is that the change is minimal and the intent remains purely for investment purposes, not for exerting management control. This suggests confidence in the underlying business rather than a strategic exit.

While the 0.04% reduction is statistically insignificant, the continued presence of a major institution like Baring Asset Management underscores a belief in the long-term value proposition of TCK’s technology and market position.

Why TCK? A Deep Dive into the Company’s Fundamentals

To understand why an investor like Baring Asset Management maintains a significant stake, we must look at the core strengths of the company. The TCK fundamentals are exceptionally strong, built on a foundation of financial stability and technological dominance.

Unrivaled SiC Technology and Market Dominance

TCK’s crown jewel is its leadership in Silicon Carbide (SiC) components, particularly Solid SiC rings used in the semiconductor etching process. As chip manufacturers push for smaller, more powerful designs (finer process nodes), the demand for high-performance, durable components like TCK’s SiC products skyrockets. The company was the first to localize this technology in Korea, creating a significant technological moat and high barriers to entry for competitors. This market leadership is a primary driver of its value.

Stellar Financial Health

A look at TCK’s financials reveals a remarkably resilient and well-managed company:

- •Robust Growth: The 2025 semi-annual report showed an 18.6% year-on-year revenue increase, primarily fueled by the Solid SiC segment.

- •High Profitability: An impressive operating profit margin of 28.4% highlights operational efficiency and strong pricing power.

- •Fortress Balance Sheet: TCK operates with virtually no debt, boasting a low debt-to-equity ratio of just 8.1%. This insulates it from interest rate volatility.

- •Forward-Looking Investment: A significant KRW 25.7 billion investment in a new factory demonstrates a clear strategy for capturing future growth. For more details on growth strategies, you can explore our guide on how to analyze semiconductor stocks.

Impact on TCK (064760) Stock and Investor Outlook

In the short term, this minor share adjustment is unlikely to cause any significant ripples in the TCK (064760) stock price. The market generally overlooks such small changes when the stated purpose is ‘simple investment’. The more important story is the long-term outlook. The fact that Baring is largely holding its position can be seen as a vote of confidence in TCK’s enduring competitive advantages.

Potential Risks to Monitor

No investment is without risk. For TCK, investors should keep two main factors on their radar:

- •Raw Material Dependency: A high percentage of graphite raw materials (over 90%) is sourced from its largest shareholder. Any disruption in this supply chain could pose a challenge.

- •Macroeconomic Headwinds: The semiconductor industry is cyclical and sensitive to global economic health. A broad downturn could impact demand, as discussed in many industry reports from sources like Bloomberg.

Conclusion: The Verdict on TCK Stock

Baring Asset Management’s minor portfolio tweak should be viewed as background noise. The real story for TCK (064760) stock lies in its powerful fundamentals and strategic position within the semiconductor value chain. The company’s unrivaled SiC technology, pristine financial health, and clear growth roadmap make it a compelling long-term holding.

Investors should focus on the bigger picture: the increasing complexity of semiconductors will continue to drive demand for TCK’s high-value products. While monitoring supply chain and macroeconomic risks is prudent, the company’s core strengths provide a solid foundation for future growth. This disclosure serves as a timely reminder to re-examine the intrinsic value of TCK and its long-term potential.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are the sole responsibility of the investor.